了解!2020年最新ACCA考试大纲出来啦!

发布时间:2020-04-24

想知道2020年最新的考试大纲和资料到哪里找吗?我们一起来了解一下吧!

获得ACCA官方最新考纲的方式如下:

在ACCA官网点击student导航按钮,在下拉菜单中点击ACCA qualification,进入后,选择不同科目,有不同的资料可以下载,包括考纲,考官文章,考官报告等。

为了避免大家浪费时间与精力,这里推荐官方出版的几个有价值的资料。

一.ACCA历年真题

ACCA历年真题可以说是制胜法宝了,如果你认真对待真题,你会发现很多题目都是有固定套路的,熟悉之后就可以立即拿到相应分数。一定要重视真题,反复训练。

二.ACCA考官文章

这里敲黑板,Technical Articles很重要。Technical Articles是ACCA考试小组出品,对于大纲中的重点,难点,新增点,学生的薄弱点,教材中阐述不够深入的点以及实务中非常重要的点,专门编写的,其重要程度可想而知。

三.ACCA考试大纲

ACCA考试大纲把每门课的知识点详细的列了出来。但是小编并不建议一直看考试大纲,因为看这个容易在details中迷失方向,抓不到重点。我们只要在学习前看看作为参考就可以了。

四.ACCA考官报告

这是ACCA考官对一次考试的评价,一是对考生的表现作出评判,二是反思考试出题的情况,有的考官会很明确的说某个知识点考生答得不好,以后还要加强考察,这就要注意了,加强准备为好。有的时候考官还会说明以后考试的侧重或者考法的变化,这也值得关注。总之,这是值得大家关注的考官资料,看上一次考试的 Examiner\\'s Report 就基本够了。

五.教材

1.我们需要BPP教材和练习册,BPP教材是全球ACCA使用最多的版本,通俗易懂,比较适合新老学员自学。推荐在F1-4选择BPP练习册,在F5-9两者兼可进行选。当然,对FTC版教材感兴趣的小伙伴也可以看看,但它比BPP教材难度稍大;

2.准备一本《会计双语英汉词典》对同学们是有益无害的,ACCA全英文考试需要同学们掌握很多的财会专业词汇,这样可以较好的理解文章语义。

好了,以上就是51题库考试学习网分享的内容,希望对想拿ACCA证书的同学有帮助。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

3 Organisations need to recruit new employees. An important step in the process is the selection interview.

Required:

(a) Explain the purpose of the selection interview. (4 marks)

3 The interview is extensively used for the selection of new employees and in many cases is the only method of selection. However,interviews have been criticised for failing to identify appropriate candidates suitable for the organisation. It is essential therefore that professional accountants recognise both the problems and opportunities that the formal selection interview presents.

(a) The purpose of the selection interview is to find the best possible person for the position who will fit into the organisation. Those conducting the interview must also ensure that the candidate clearly understands the job on offer, career prospects and that all candidates feel that fair treatment has been provided through the selection process.In addition, the interview also gives the opportunity to convey a good impression of the organisation, whether the candidate has been successful or not.

(ii) the recent financial performance of Merton plc from a shareholder perspective. Clearly identify any

issues that you consider should be brought to the attention of the ordinary shareholders. (15 marks)

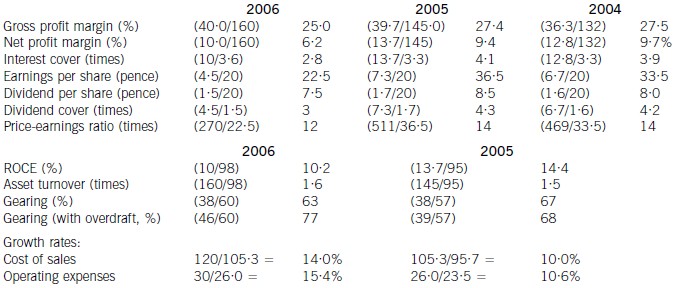

(ii) Discussion of financial performance

It is clear that 2006 has been a difficult year for Merton plc. There are very few areas of interest to shareholders where

anything positive can be found to say.

Profitability

Return on capital employed has declined from 14·4% in 2005, which compared favourably with the sector average of

12%, to 10·2% in 2006. Since asset turnover has improved from 1·5 to 1·6 in the same period, the cause of the decline

is falling profitability. Gross profit margin has fallen each year from 27·5% in 2004 to 25% in 2006, equal to the sector

average, despite an overall increase in turnover during the period of 10% per year. Merton plc has been unable to keep

cost of sales increases (14% in 2006 and 10% in 2005) below the increases in turnover. Net profit margin has declined

over the same period from 9·7% to 6·2%, compared to the sector average of 8%, because of substantial increases in

operating expenses (15·4% in 2006 and 10·6% in 2005). There is a pressing need here for Merton plc to bring cost

of sales and operating costs under control in order to improve profitability.

Gearing and financial risk

Gearing as measured by debt/equity has fallen from 67% (2005) to 63% (2006) because of an increase in

shareholders’ funds through retained profits. Over the same period the overdraft has increased from £1m to £8m and

cash balances have fallen from £16m to £1m. This is a net movement of £22m. If the overdraft is included, gearing

has increased to 77% rather than falling to 63%.

None of these gearing levels compare favourably with the average gearing for the sector of 50%. If we consider the large

increase in the overdraft, financial risk has clearly increased during the period. This is also evidenced by the decline in

interest cover from 4·1 (2005) to 2·8 (2006) as operating profit has fallen and interest paid has increased. In each year

interest cover has been below the sector average of eight and the current level of 2·8 is dangerously low.

Share price

As the return required by equity investors increases with increasing financial risk, continued increases in the overdraft

will exert downward pressure on the company’s share price and further reductions may be expected.

Investor ratios

Earnings per share, dividend per share and dividend cover have all declined from 2005 to 2006. The cut in the dividend

per share from 8·5 pence per share to 7·5 pence per share is especially worrying. Although in its announcement the

company claimed that dividend growth and share price growth was expected, it could have chosen to maintain the

dividend, if it felt that the current poor performance was only temporary. By cutting the dividend it could be signalling

that it expects the poor performance to continue. Shareholders have no guarantee as to the level of future dividends.

This view could be shared by the market, which might explain why the price-earnings ratio has fallen from 14 times to

12 times.

Financing strategy

Merton plc has experienced an increase in fixed assets over the last period of £10m and an increase in stocks and

debtors of £21m. These increases have been financed by a decline in cash (£15m), an increase in the overdraft (£7m)

and an increase in trade credit (£6m). The company is following an aggressive strategy of financing long-term

investment from short-term sources. This is very risky, since if the overdraft needed to be repaid, the company would

have great difficulty in raising the funds required.

A further financing issue relates to redemption of the existing debentures. The 10% debentures are due to be redeemed

in two years’ time and Merton plc will need to find £13m in order to do this. It does not appear that this sum can be

raised internally. While it is possible that refinancing with debt paying a lower rate of interest may be possible, the low

level of interest cover may cause concern to potential providers of debt finance, resulting in a higher rate of interest. The

Finance Director of Merton plc needs to consider the redemption problem now, as thought is currently being given to

raising a substantial amount of new equity finance. This financing choice may not be available again in the near future,

forcing the company to look to debt finance as a way of effecting redemption.

Overtrading

The evidence produced by the financial analysis above is that Merton plc is showing some symptoms of overtrading

(undercapitalisation). The board are suggesting a rights issue as a way of financing an expansion of business, but it is

possible that a rights issue will be needed to deal with the overtrading problem. This is a further financing issue requiring

consideration in addition to the redemption of debentures mentioned earlier.

Conclusion

Ordinary shareholders need to be aware of the following issues.

1. Profitability has fallen over the last year due to poor cost control

2. A substantial increase in the overdraft over the last year has caused gearing to increase

3. It is possible that the share price will continue to fall

4. The dividend cut may warn of continuing poor performance in the future

5. A total of £13m of debentures need redeeming in two year’s time

6. A large amount of new finance is needed for working capital and debenture redemption

Appendix: Analysis of key ratios and financial information

(ii) Explain whether or not Carver Ltd will become a close investment-holding company as a result of

acquiring either the office building or the share portfolio and state the relevance of becoming such a

company. (2 marks)

(ii) Close investment holding company status

Carver Ltd will not become a close investment-holding company if it purchases the office building as, although it will no

longer be a trading company, it intends to rent out the building to a number of tenants none of whom is connected to

the company.

Carver Ltd will become a close investment holding company if it purchases a portfolio of quoted shares as it will no

longer be a trading company. As a result it will pay corporation tax at the full rate of 30% regardless of the level of its

profits.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-04-18

- 2020-01-10

- 2020-01-10

- 2020-05-09

- 2019-12-31

- 2020-04-23

- 2020-01-10

- 2020-01-10

- 2020-02-20

- 2020-01-09

- 2020-03-08

- 2020-01-10

- 2020-01-09

- 2020-04-22

- 2020-05-21

- 2020-04-20

- 2019-07-20

- 2020-01-10

- 2019-07-20

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-04-15

- 2020-08-16

- 2020-01-09

- 2019-07-20

- 2020-01-10

- 2020-04-18

- 2019-03-23