ACCA考试常用公式汇总,值得西藏考生收藏!

发布时间:2020-01-10

距离2020年3月份的ACCA考试还有两个多月左右的时间,想必备考ACCA的同学们正在如火如荼地进行着复习。那么,今天这条“公式宝典”你一定要收好,或许会帮助你成功通过ACCA考试哦!接下来,51题库考试学习网将这份“公式宝典”分享给大家:

因为ACCA考试毕竟是国际性质的考试,因此一些题的计算可能就存在不同的计算方式,计算方式的不同也会导致结果的不同。

一、境内

1、税额=销项税-进项税

2、销项税=销售额×税率

3、视销征税无销额(1)当月类平均;(2)近类货平均,(3)组税价=成本×(1+成利率)

4、征增税及消税:

组税价=成本×(1+成润率)+消税

组税价=成本×(1+成润率)/(1-消率)

5、含税额换

不含税销额=含税销额/1+率(一般)

不含税销额=含税销额/1+征率(小规模)

6、购农销农品,或向小纳人购农品:

准扣的进税=买价×扣率(13%)

7、一般纳人外购货物付的运费

准扣的进税=运费×扣除率

*随运付的装卸、保费不扣

8、小纳人纳额=销项额×征率(6%或4%)

*不扣进额

9、小纳人不含税销额=含额/(1+征率)

10、自来水公司销水(6%)

不含税销额=发票额×(1+征率)

以上是国内物品的计算方式,接下来是国外进口的相关公式

二、进口货

1、组税价=关税完价+关税+消税

2、纳额=组税价×税率

三、出口货物退(免)税

1、"免、抵、退"计算方法(指生产企自营委外贸代出口自产)

(1)纳额=内销销税-(进税-免抵退税不免、抵税)

(2)免抵退税=FOB×外汇RMB牌价×退率-免抵退税抵减额

*FOB:出口货物离岸价。

*免抵退税抵减额=免税购原料价×退税率

免税购原料=国内购免原料+进料加工免税进料

进料加工免税进口料件组税价=到岸价+关、消税

(3)应退税和免抵税

A、如期末留抵税≤免抵退税,则:

应退税=期末留抵税

免抵税=免抵退税-应退税

B、期末留抵税>免抵退税,则:

应退税=免抵退税

免抵税=0

*期末留抵税额据《增值税纳税申报表》中"期末留抵税额"定。

(4)免抵退税不得免和抵税

免抵退税不免和抵税=FOB×外汇RMB牌价×(出口征率-出口退率)-免抵退税不免抵税抵减额

免抵退税不免和抵扣税抵减额=免税进原料价×(出口征率-出口货物退率)

2、先征后退

(1)外贸及外贸制度工贸企购货出口,出口增税免;出口后按收购成本与退税率算退税还外贸,征、退税差计企业成本

应退税额=外贸购不含增税购进金额×退税率

(2)外贸企购小纳人出货口增税退税规定:

A、从小纳人购并持普通发票准退税的抽纱、工艺品等12类出口货物,销售出口货入免,退还出口货进税

退税=[发票列(含税)销额]/(1+征率)×6%或5%

B、从小纳人购代开的增税发票的出口货:

退税=增税发票金额×6%或5%

C、外企托生企加工出口货的退税规定:

原辅料退税=国内原辅料增税发票进项×原辅料退税率

以上这些就是全部ACCA考试常用公式,希望对大家有所帮助!最后51题库考试学习网想告诉大家:“放弃可以找到一万个理由,但坚持只需一个信念!致敬那些在ACCA备考路上永不放弃的人,好结果只留给有毅力的人。”

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(ii) Calculate the probability of the net profit being less than £75 million. (2 marks)

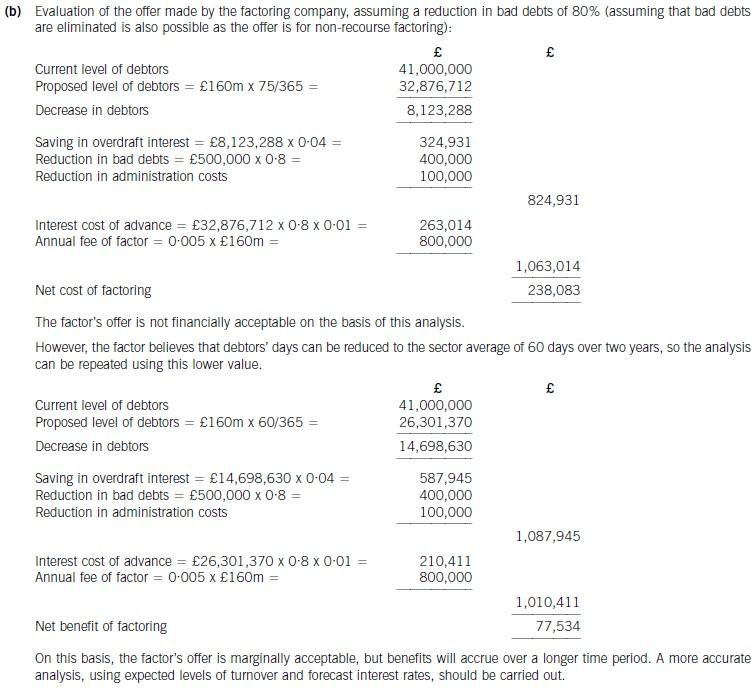

(b) Determine whether the factoring company’s offer can be recommended on financial grounds. Assume a

working year of 365 days and base your analysis on financial information for 2006. (8 marks)

6 Proposed ISA 600 (Revised and Redrafted) The Audit of Group Financial Statements is likely to substantially increase

the formal requirements in the area of group audits.

Required:

(a) Outline the significant issues that are being addressed in the IAASB’s project on group audits. (5 marks)

6 REQUIREMENTS IN GROUP AUDITS

Tutorial note: The answer which follows is indicative of the range of points which might be made. Other relevant material will be

given suitable credit.

(a) Significant issues

Tutorial note: The objective of the IAASB’s project on the audit of group financial statements (‘group audits’) was to deal

with special considerations in group audits and, in particular, the involvement of other auditors. The re-exposure of ISA 600

(Revised and Redrafted) in March 2006 (following initial publication of a proposed revised ISA in December 2003 and an

exposure draft in March 2005) reflects the significance of the issues that the IAASB has sought to address.

Sole vs divided responsibility

The IAASB has concluded that the group auditor has sole responsibility for the group audit opinion. Thus the exposure drafts

eliminate the distinction between sole and divided responsibility. Therefore no reference to another auditor (e.g. of significant

components) should be made in the group auditor’s report. The practice of referring to another auditor may, arguably, be more

transparent to users of group financial statements. However, it may also mislead users to believe that the group auditor does

not have sole responsibility.

Definition of group auditor

The group auditor is the auditor who signs the auditor’s report on the group financial statements. The project has sought to

clarify whether, for example, an auditor from another office of the group engagement partner’s firm is a member of the group

engagement team or an ‘other auditor’.

‘Related’ vs ‘unrelated’ auditors

IAASB recognises that the nature, timing and extent of procedures performed by the group auditor, including the review of

the other auditor’s audit documentation, are affected by the group auditor’s relationship with the other audit. (For example,

if the other auditor operates under the quality control policies and procedures of the group auditor.) However, IAASB

acknowledges that a consistent distinction between ‘related’ and ‘unrelated’ auditors cannot be made due to the varying

structures of audit firms and their networks. Consequently, the only distinction that is made is between the ‘group’ and ‘other’

auditors.

Acceptance/continuance as group auditor

A group auditor should only accept or continue an engagement if sufficient appropriate evidence is expected to be obtained

on which to base the group audit opinion. Acceptance and continuance as group auditors therefore requires an assessment

of the risk of misstatement in components. IAASB has therefore proposed guidance on the benchmarks that might be used

in identifying significant components.

Access to information

IAASB has concluded that a group audit engagement should be refused (or resigned from) if the group engagement partner

concludes that it will not be possible to obtain sufficient appropriate audit evidence, the result of which would be a disclaimer.

However, if the group engagement partner is prohibited from refusing or resigning an engagement, the group audit opinion

must be disclaimed.

Aggregation of components

Sufficient appropriate audit evidence must be obtained in respect of components that are not individually significant (but

significant in aggregate). This requires that components be selected for audit procedures (e.g. on specified account balances).

Analytical procedures are required to be performed on components that are not selected. IAASB has therefore identified factors

to be considered in selecting components that are not individually significant.

Responsibilities of other auditors

Historically, other auditors, knowing the context in which their work will be used by the group auditor, have been required to

cooperate with the group auditor. However, the project did not address guidance for other auditors. Therefore, in providing

guidance on the group audit, the IAASB requires the group auditor to obtain an understanding of the requirements for other

auditors to cooperate with the group auditor and provide access to relevant documentation.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-01-10

- 2020-04-21

- 2020-01-10

- 2019-07-20

- 2020-04-08

- 2020-01-09

- 2020-01-30

- 2020-01-09

- 2020-03-12

- 2020-01-10

- 2020-04-10

- 2020-01-10

- 2020-05-15

- 2020-02-18

- 2021-06-24

- 2020-01-10

- 2019-07-20

- 2020-01-10

- 2020-01-09

- 2020-01-10

- 2020-01-09

- 2020-01-10

- 2020-01-09

- 2020-01-10

- 2020-01-10

- 2020-04-24

- 2020-03-12

- 2020-01-09

- 2020-04-10

- 2020-01-10