ACCA考试常用公式汇总,值得贵州省考生收藏!

发布时间:2020-01-10

距离2020年3月份的ACCA考试还有两个多月左右的时间,想必备考ACCA的同学们正在如火如荼地进行着复习。那么,今天这条“公式宝典”你一定要收好,或许会帮助你成功通过ACCA考试哦!接下来,51题库考试学习网将这份“公式宝典”分享给大家:

因为ACCA考试毕竟是国际性质的考试,因此一些题的计算可能就存在不同的计算方式,计算方式的不同也会导致结果的不同。

一、境内

1、税额=销项税-进项税

2、销项税=销售额×税率

3、视销征税无销额(1)当月类平均;(2)近类货平均,(3)组税价=成本×(1+成利率)

4、征增税及消税:

组税价=成本×(1+成润率)+消税

组税价=成本×(1+成润率)/(1-消率)

5、含税额换

不含税销额=含税销额/1+率(一般)

不含税销额=含税销额/1+征率(小规模)

6、购农销农品,或向小纳人购农品:

准扣的进税=买价×扣率(13%)

7、一般纳人外购货物付的运费

准扣的进税=运费×扣除率

*随运付的装卸、保费不扣

8、小纳人纳额=销项额×征率(6%或4%)

*不扣进额

9、小纳人不含税销额=含额/(1+征率)

10、自来水公司销水(6%)

不含税销额=发票额×(1+征率)

以上是国内物品的计算方式,接下来是国外进口的相关公式

二、进口货

1、组税价=关税完价+关税+消税

2、纳额=组税价×税率

三、出口货物退(免)税

1、"免、抵、退"计算方法(指生产企自营委外贸代出口自产)

(1)纳额=内销销税-(进税-免抵退税不免、抵税)

(2)免抵退税=FOB×外汇RMB牌价×退率-免抵退税抵减额

*FOB:出口货物离岸价。

*免抵退税抵减额=免税购原料价×退税率

免税购原料=国内购免原料+进料加工免税进料

进料加工免税进口料件组税价=到岸价+关、消税

(3)应退税和免抵税

A、如期末留抵税≤免抵退税,则:

应退税=期末留抵税

免抵税=免抵退税-应退税

B、期末留抵税>免抵退税,则:

应退税=免抵退税

免抵税=0

*期末留抵税额据《增值税纳税申报表》中"期末留抵税额"定。

(4)免抵退税不得免和抵税

免抵退税不免和抵税=FOB×外汇RMB牌价×(出口征率-出口退率)-免抵退税不免抵税抵减额

免抵退税不免和抵扣税抵减额=免税进原料价×(出口征率-出口货物退率)

2、先征后退

(1)外贸及外贸制度工贸企购货出口,出口增税免;出口后按收购成本与退税率算退税还外贸,征、退税差计企业成本

应退税额=外贸购不含增税购进金额×退税率

(2)外贸企购小纳人出货口增税退税规定:

A、从小纳人购并持普通发票准退税的抽纱、工艺品等12类出口货物,销售出口货入免,退还出口货进税

退税=[发票列(含税)销额]/(1+征率)×6%或5%

B、从小纳人购代开的增税发票的出口货:

退税=增税发票金额×6%或5%

C、外企托生企加工出口货的退税规定:

原辅料退税=国内原辅料增税发票进项×原辅料退税率

以上这些就是全部ACCA考试常用公式,希望对大家有所帮助!最后51题库考试学习网想告诉大家:“放弃可以找到一万个理由,但坚持只需一个信念!致敬那些在ACCA备考路上永不放弃的人,好结果只留给有毅力的人。”

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

2 Marrgrett, a public limited company, is currently planning to acquire and sell interests in other entities and has asked

for advice on the impact of IFRS3 (Revised) ‘Business Combinations’ and IAS27 (Revised) ‘Consolidated and Separate

Financial Statements’. The company is particularly concerned about the impact on earnings, net assets and goodwill

at the acquisition date and any ongoing earnings impact that the new standards may have.

The company is considering purchasing additional shares in an associate, Josey, a public limited company. The

holding will increase from 30% stake to 70% stake by offering the shareholders of Josey, cash and shares in

Marrgrett. Marrgrett anticipates that it will pay $5 million in transaction costs to lawyers and bankers. Josey had

previously been the subject of a management buyout. In order that the current management shareholders may remain

in the business, Marrgrett is going to offer them share options in Josey subject to them remaining in employment for

two years after the acquisition. Additionally, Marrgrett will offer the same shareholders, shares in the holding company

which are contingent upon a certain level of profitability being achieved by Josey. Each shareholder will receive shares

of the holding company up to a value of $50,000, if Josey achieves a pre-determined rate of return on capital

employed for the next two years.

Josey has several marketing-related intangible assets that are used primarily in marketing or promotion of its products.

These include trade names, internet domain names and non-competition agreements. These are not currently

recognised in Josey’s financial statements.

Marrgrett does not wish to measure the non-controlling interest in subsidiaries on the basis of the proportionate

interest in the identifiable net assets, but wishes to use the ‘full goodwill’ method on the transaction. Marrgrett is

unsure as to whether this method is mandatory, or what the effects are of recognising ‘full goodwill’. Additionally the

company is unsure as to whether the nature of the consideration would affect the calculation of goodwill.

To finance the acquisition of Josey, Marrgrett intends to dispose of a partial interest in two subsidiaries. Marrgrett will

retain control of the first subsidiary but will sell the controlling interest in the second subsidiary which will become

an associate. Because of its plans to change the overall structure of the business, Marrgrett wishes to recognise a

re-organisation provision at the date of the business combination.

Required:

Discuss the principles and the nature of the accounting treatment of the above plans under International Financial

Reporting Standards setting out any impact that IFRS3 (Revised) ‘Business Combinations’ and IAS27 (Revised)

‘Consolidated and Separate Financial Statements’ might have on the earnings and net assets of the group.

Note: this requirement includes 2 professional marks for the quality of the discussion.

(25 marks)

2 IFRS3 (Revised) is a further development of the acquisition model and represents a significant change in accounting for business

combinations. The consideration is the amount paid for the business acquired and is measured at fair value. Consideration will

include cash, assets, contingent consideration, equity instruments, options and warrants. It also includes the fair value of all equity

interests that the acquirer may have held previously in the acquired business. The principles to be applied are that:

(a) a business combination occurs only in respect of the transaction that gives one entity control of another

(b) the identifiable net assets of the acquiree are re-measured to their fair value on the date of the acquisition

(c) NCI are measured on the date of acquisition under one of the two options permitted by IFRS3 (Revised).

An equity interest previously held in the acquiree which qualified as an associate under IAS28 is similarly treated as if it were

disposed of and reacquired at fair value on the acquisition date. Accordingly, it is re-measured to its acquisition date fair value, and

any resulting gain or loss compared to its carrying amount under IAS28 is recognised in profit or loss. Thus the 30% holding in

the associate which was previously held will be included in the consideration. If the carrying amount of the interest in the associate

is not held at fair value at the acquisition date, the interest should be measured to fair value and the resulting gain or loss should

be recognised in profit or loss. The business combination has effectively been achieved in stages.

The fees payable in transaction costs are not deemed to be part of the consideration paid to the seller of the shares. They are not

assets of the purchased business that are recognised on acquisition. Therefore, they should be expensed as incurred and the

services received. Transaction costs relating to the issue of debt or equity, if they are directly attributable, will not be expensed but

deducted from debt or equity on initial recognition.

It is common for part of the consideration to be contingent upon future events. Marrgrett wishes some of the existing

shareholders/employees to remain in the business and has, therefore, offered share options as an incentive to these persons. The

issue is whether these options form. part of the purchase consideration or are compensation for post-acquisition services. The

conditions attached to the award will determine the accounting treatment. In this case there are employment conditions and,

therefore, the options should be treated as compensation and valued under IFRS2 ‘Share based payment’. Thus a charge will

appear in post-acquisition earnings for employee services as the options were awarded to reward future services of employees

rather than to acquire the business.

The additional shares to a fixed value of $50,000 are contingent upon the future returns on capital employed. Marrgrett only wants

to make additional payments if the business is successful. All consideration should be fair valued at the date of acquisition,

including the above contingent consideration. The contingent consideration payable in shares where the number of shares varies

to give the recipient a fixed value ($50,000) meets the definition of a financial liability under IAS32 ‘Financial Instruments:

Presentation’. As a result the liability will have to be fair valued and any subsequent remeasurement will be recognised in the

income statement. There is no requirement under IFRS3 (Revised) for the payments to be probable.

Intangible assets should be recognised on acquisition under IFRS3 (Revised). These include trade names, domain names, and

non-competition agreements. Thus these assets will be recognised and goodwill effectively reduced. The additional clarity in

IFRS3 (Revised) could mean that more intangible assets will be recognised on acquisition. As a result of this, the post-combination

income statement may have more charges for amortisation of the intangibles than was previously the case.

The revised standard gives entities the option, on a transaction by transaction basis, to measure non-controlling interests (NCI) at

the fair value of the proportion of identifiable net assets or at full fair value. The first option results in measurement of goodwill on

consolidation which would normally be little different from the previous standard. The second approach records goodwill on the

NCI as well as on the acquired controlling interest. Goodwill is the residual but may differ from that under the previous standard

because of the nature of the valuation of the consideration as previously held interests are fair valued and also because goodwill

can be measured in the above two ways (full goodwill and partial goodwill). The standard gives entities a choice for each separate

business combination of recognising full or partial goodwill. Recognising full goodwill will increase reported net assets and may

result in any future impairment of goodwill being of greater value. Measuring NCI at fair value may have some difficulties but

goodwill impairment testing may be easier under full goodwill as there is no need to gross-up goodwill for partly-owned

subsidiaries. The type of consideration does not affect goodwill regardless of how the payment is structured. Consideration is

recognised in total at its fair value at the date of acquisition. The form. of the consideration will not affect goodwill but the structure

of the payments can affect post-acquisition profits. Contingent payments which are deemed to be debt instruments will be

remeasured at each reporting date with the change going to the income statement.

Marrgrett has a maximum period of 12 months to finalise the acquisition accounting but will not be able to recognise the

re-organisation provision at the date of the business combination. The ability of the acquirer to recognise a liability for reducing or

changing the activities of the acquiree is restricted. A restructuring provision can only be recognised in a business combination

when the acquiree has at the acquisition date, an existing liability which complies with IAS37 ‘Provisions, contingent liabilities and

contingent assets’. These conditions are unlikely to exist at the acquisition date. A restructuring plan that is conditional on the

completion of a business combination is not recognised in accounting for the acquisition but the expense will be met against

post-acquisition earnings.

IAS27 (Revised) uses the economic entity model whereas previous practice used the parent company approach. The economic

entity model treats all providers of equity capital as shareholders of the entity even where they are not shareholders in the parent.

A partial disposal of an interest in a subsidiary in which control is still retained is seen as a treasury transaction and accounted for

in equity. It does not result in a gain or loss but an increase or decrease in equity. However, where a partial disposal in a subsidiary

results in a loss of control but the retention of an interest in the form. of an associate, then a gain or loss is recognised in the whole

interest. A gain or loss is recognised on the portion that has been sold, and a holding gain or loss is recognised on the interest

retained being the difference between the book value and fair value of the interest. Both gains/losses are recognised in the income

statement.

(b) Explain what effect the acquisition of Di Rollo Co will have on the planning of your audit of the consolidated

financial statements of Murray Co for the year ending 31 March 2008. (10 marks)

(b) Effect of acquisition on planning the audit of Murray’s consolidated financial statements for the year ending 31 March

2008

Group structure

The new group structure must be ascertained to identify all entities that should be consolidated into the Murray group’s

financial statements for the year ending 31 March 2008.

Materiality assessment

Preliminary materiality for the group will be much higher, in monetary terms, than in the prior year. For example, if a % of

total assets is a determinant of the preliminary materiality, it may be increased by 10% (as the fair value of assets acquired,

including goodwill, is $2,373,000 compared with $21·5m in Murray’s consolidated financial statements for the year ended

31 March 2007).

The materiality of each subsidiary should be re-assessed, in terms of the enlarged group as at the planning stage. For

example, any subsidiary that was just material for the year ended 31 March 2007 may no longer be material to the group.

This assessment will identify, for example:

– those entities requiring an audit visit; and

– those entities for which substantive analytical procedures may suffice.

As Di Rollo’s assets are material to the group Ross should plan to inspect the South American operations. The visit may

include a meeting with Di Rollo’s previous auditors to discuss any problems that might affect the balances at acquisition and

a review of the prior year audit working papers, with their permission.

Di Rollo was acquired two months into the financial year therefore its post-acquisition results should be expected to be

material to the consolidated income statement.

Goodwill acquired

The assets and liabilities of Di Rollo at 31 March 2008 will be combined on a line-by-line basis into the consolidated financial

statements of Murray and goodwill arising on acquisition recognised.

Audit work on the fair value of the Di Rollo brand name at acquisition, $600,000, may include a review of a brand valuation

specialist’s working papers and an assessment of the reasonableness of assumptions made.

Significant items of plant are likely to have been independently valued prior to the acquisition. It may be appropriate to plan

to place reliance on the work of expert valuers. The fair value adjustment on plant and equipment is very high (441% of

carrying amount at the date of acquisition). This may suggest that Di Rollo’s depreciation policies are over-prudent (e.g. if

accelerated depreciation allowed for tax purposes is accounted for under local GAAP).

As the amount of goodwill is very material (approximately 50% of the cash consideration) it may be overstated if Murray has

failed to recognise any assets acquired in the purchase of Di Rollo in accordance with IFRS 3 Business Combinations. For

example, Murray may have acquired intangible assets such as customer lists or franchises that should be recognised

separately from goodwill and amortised (rather than tested for impairment).

Subsequent impairment

The audit plan should draw attention to the need to consider whether the Di Rollo brand name and goodwill arising have

suffered impairment as a result of the allegations against Di Rollo’s former chief executive.

Liabilities

Proceedings in the legal claim made by Di Rollo’s former chief executive will need to be reviewed. If the case is not resolved

at 31 March 2008, a contingent liability may require disclosure in the consolidated financial statements, depending on the

materiality of amounts involved. Legal opinion on the likelihood of Di Rollo successfully defending the claim may be sought.

Provision should be made for any actual liabilities, such as legal fees.

Group (related party) transactions and balances

A list of all the companies in the group (including any associates) should be included in group audit instructions to ensure

that intra-group transactions and balances (and any unrealised profits and losses on transactions with associates) are

identified for elimination on consolidation. Any transfer pricing policies (e.g. for clothes manufactured by Di Rollo for Murray

and sales of Di Rollo’s accessories to Murray’s retail stores) must be ascertained and any provisions for unrealised profit

eliminated on consolidation.

It should be confirmed at the planning stage that inter-company transactions are identified as such in the accounting systems

of all companies and that inter-company balances are regularly reconciled. (Problems are likely to arise if new inter-company

balances are not identified/reconciled. In particular, exchange differences are to be expected.)

Other auditors

If Ross plans to use the work of other auditors in South America (rather than send its own staff to undertake the audit of Di

Rollo), group instructions will need to be sent containing:

– proforma statements;

– a list of group and associated companies;

– a statement of group accounting policies (see below);

– the timetable for the preparation of the group accounts (see below);

– a request for copies of management letters;

– an audit work summary questionnaire or checklist;

– contact details (of senior members of Ross’s audit team).

Accounting policies

Di Rollo may have material accounting policies which do not comply with the rest of the Murray group. As auditor to Di Rollo,

Ross will be able to recalculate the effect of any non-compliance with a group accounting policy (that Murray’s management

would be adjusting on consolidation).

Timetable

The timetable for the preparation of Murray’s consolidated financial statements should be agreed with management as soon

as possible. Key dates should be planned for:

– agreement of inter-company balances and transactions;

– submission of proforma statements;

– completion of the consolidation package;

– tax review of group accounts;

– completion of audit fieldwork by other auditors;

– subsequent events review;

– final clearance on accounts of subsidiaries;

– Ross’s final clearance of consolidated financial statements.

Tutorial note: The order of dates is illustrative rather than prescriptive.

The group have now decided to convert their business idea into reality.

(b) What elements should a marketing plan contain to achieve a successful launch of their restaurant?

(8 marks)

(b) The launch of any new business is a critical event and a marketing plan a vital ingredient in achieving launch success. Most

companies will associate a marketing plan with the ever-popular 4 Ps. However, the marketing mix can only be decided once

some fundamental marketing decisions have been taken. Firstly, the group need to clearly identify which segments of the

market they are seeking to attract. Segments are made up of groups of customers with similar needs and expectations. If they

are identifying the student market as an important segment they should recognise that there are very different segments within

this group. They are most likely to want to target those students willing and able to pay for a high quality meal and experience.

They are not in the market for low priced/fast food. This requires them to recognise how they are trying to position their

restaurant – high quality and moderate prices looks to be a combination, which will deliver an attractive service and added

value to the customer. The relationship between the customers’ perception of added value and the price charged is, in terms

of Bowman’s strategy clock, likely to be that of a focused differentiator.

For the Casa del Mediterraneo getting the product or service right will involve a complex co-ordination of many different

activities – from buying the right food through to delivering the orders efficiently. As a service, there may be many more things

that potentially can go wrong and it really does come down to the people delivering the service. This involves one of the

additional ‘P’s, involved in delivering services, namely processes, which together with the physical evidence in the shape of

the restaurant, will have a major say in the success or otherwise of the launch. Clearly, the place and the physical evidence

are one and the same thing and the right location will also affect the success of both the launch and the whole venture.

Pricing in a competitive market will be important and many upmarket restaurants price on the basis of what the market will

bear. There needs to be a clear relationship between the price and the value offered. Finally, promotion is perhaps the key

element in the effective launch of the new restaurant. There will need to be a correct choice of media to reach the targetaudience including the use of web-based advertising to get the restaurant known.

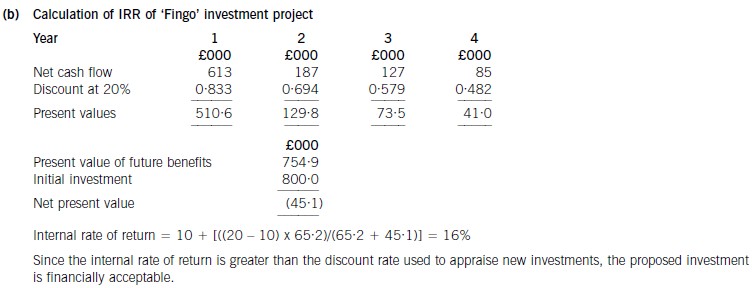

(b) Calculate the internal rate of return of the proposed investment and comment on your findings. (5 marks)

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-05-09

- 2020-01-14

- 2020-04-30

- 2020-01-09

- 2020-05-21

- 2020-04-24

- 2020-01-09

- 2020-04-20

- 2020-04-09

- 2020-01-10

- 2020-01-10

- 2020-04-11

- 2020-05-21

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-01-13

- 2020-01-11

- 2020-01-09

- 2021-06-18

- 2020-05-09

- 2020-01-09

- 2021-08-08

- 2020-01-10

- 2020-01-10

- 2020-01-09

- 2020-05-14