速看!你符合acca报名资格吗?

发布时间:2020-01-31

最近有很多小伙伴都在问51题库考试学习网报考ACCA需要什么条件?今天51题库考试学习网就为各位小伙伴说说吧!

一、ACCA报名条件:

以下是报名参加ACCA考试资格要求,具备以下条件之一即可注册成为ACCA学员:

ACCA报名条件

1、具有教育部承认的大专以上学历。

2、教育部认可的高等院校在校生,但是需要完成大一全年的所有课程考试才行。

3、未符合前两项报名资格的,可以先申请参加FIA资格考试,通过FFA、FMA和FAB三门课程后,可以申请转入ACCA并且豁免F1-F3三门课程的考试,直接进入ACCA技能课程阶段的考试。

因为这两种资格考试的三门课程内容一致,ACCA认可FIA的这三门成绩,而且申请FIA资格考试的学员,可以不满足以上1、2项条件,并且没有相关的年龄限制。

为了提升学员注册处理的效率和质量,ACCA从2012年8月1日起推出在线注册申请流程,ACCA学员可以通过http://www.accaglobal.com/完成在线注册报名,申请成为ACCA学员。只需10分钟便可完成整个在线注册申请流程并在线交纳注册费用,ACCA将在15个工作日内处理您的注册申请。

二、ACCA注册操作程序

注册前请先阅读此注意事项,然后参考详细申请步骤完成整个注册程序。

1、请准备好您的以下证件待上传,所有上传文件为彩色扫描件或者照片格式。

身份证或者护照

学历/学位证书。

持国外学历及MPAcc学员还需提交所有课程成绩单。

高校在校生注册需提交学校出具的在校证明函(需证明其顺利完成前几学年)及所学所有学年的课程考试合格的成绩单。

其他有利申请免试的证书(如CICPA、CMA)(非必须,持有者须提供)

译文:非英文证件均需提交英文翻译件译文须由高校或者公司加盖红章,公证处/翻译公司提供的正规翻译件均可(请不要使用钢印图章)。

2、请记住您的注册号和密码,以便查询注册进度。

3、请确定您提供给ACCA的EMAIL地址真实有效。ACCA将通过EMAIL与学员确认注册及发布重要信息。

(Tip:请确保您填写的邮箱地址是自己的,不是与他人共享的。最好更换或创建一个全新的邮箱。)

详细申请步骤:

1、登录http://www.accaglobal.com

2、点击Apply now开始进行网上注册

在注册过程中遇到的问题您可以与ACCA全球客服中心(ACCA Connect)联系,客服中心将为您提供24小时,12个月,365天的全方位快捷服务。

以上就是51题库考试学习网为大家带来的相关内容,希望能给各位小伙伴带来帮助。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(b) Explain the meaning of Stephanie’s comment: ‘I would like to get risk awareness embedded in the culture

at the Southland factory.’ (5 marks)

Embedded risk

Risk awareness is the knowledge of the nature, hazards and probabilities of risk in given situations. Whilst management will

typically be more aware than others in the organisation of many risks, it is important to embed awareness at all levels so as

to reduce the costs of risk to an organisation and its members (which might be measured in financial or non-financial terms).

In practical terms, embedding means introducing a taken-for-grantedness of risk awareness into the culture of an organisation

and its internal systems. Culture, defined in Handy’s terms as ‘the way we do things round here’ underpins all risk

management activity as it defines attitudes, actions and beliefs.

The embedding of risk awareness into culture and systems involves introducing risk controls into the process of work and the

environment in which it takes place. Risk awareness and risk mitigation become as much a part of a process as the process

itself so that people assume such measures to be non-negotiable components of their work experience. In such organisational

cultures, risk management is unquestioned, taken for granted, built into the corporate mission and culture and may be used

as part of the reward system.

Tutorial note: other meaningful definitions of culture in an organisational context are equally acceptable.

There is considerable evidence that small firms are reluctant to carry out strategic planning in their businesses.

(b) What are the advantages and disadvantages for Gould and King Associates in creating and implementing a

strategic plan? (8 marks)

(b) Clearly, there is a link between the ability to write a business plan and the willingness, or otherwise, of small firms to carry

out strategic planning. Whilst writing a business plan may be a necessity in order to acquire financial support, there is much

more question over the benefits to the existing small business, such as Gould and King, of carrying out strategic planning.

One of the areas of greatest debate is whether carrying out strategic planning leads to improved performance. Equally

contentious is whether the formal rational planning model is worthwhile or whether strategy is much more of an emergent

process, with the firm responding to changes in its competitive environment.

One source argues that small firms may be reluctant to create a strategic plan because of the time involved; small firms may

find day-to-day survival and crisis management prevents them having the luxury of planning where they mean to be over the

next few years. Secondly, strategic plans may also be viewed as too restricting, stopping the firm responding flexibly and

quickly to opportunities and threats. Thirdly, many small firms may feel that they lack the necessary skills to carry out strategic

planning. Strategic planning is seen as a ‘big’ firm process and inappropriate for small firms. Again, there is evidence to

suggest that owner-managers are much less aware of strategic management tools such as SWOT, PESTEL and mission

statements than their managers. Finally, owner-managers may be reluctant to involve others in the planning process, which

would necessitate giving them access to key information about the business. Here there is an issue of the lack of trust and

openness preventing the owner-manager developing and sharing a strategic plan. Many owner-managers may be quite happy

to limit the size of the business to one which they can personally control.

On the positive side there is evidence to show that a commitment to strategic planning results in speedier decision making,

a better ability to introduce change and innovation and being good at managing change. This in turn results in better

performance including higher rates of growth and profits, clear indicators of competitive advantage. If Gould and King arelooking to grow the business as suggested, this means some strategic planning will necessarily be involved

(ii) the recent financial performance of Merton plc from a shareholder perspective. Clearly identify any

issues that you consider should be brought to the attention of the ordinary shareholders. (15 marks)

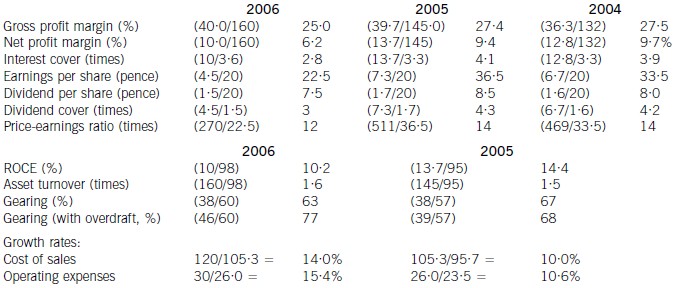

(ii) Discussion of financial performance

It is clear that 2006 has been a difficult year for Merton plc. There are very few areas of interest to shareholders where

anything positive can be found to say.

Profitability

Return on capital employed has declined from 14·4% in 2005, which compared favourably with the sector average of

12%, to 10·2% in 2006. Since asset turnover has improved from 1·5 to 1·6 in the same period, the cause of the decline

is falling profitability. Gross profit margin has fallen each year from 27·5% in 2004 to 25% in 2006, equal to the sector

average, despite an overall increase in turnover during the period of 10% per year. Merton plc has been unable to keep

cost of sales increases (14% in 2006 and 10% in 2005) below the increases in turnover. Net profit margin has declined

over the same period from 9·7% to 6·2%, compared to the sector average of 8%, because of substantial increases in

operating expenses (15·4% in 2006 and 10·6% in 2005). There is a pressing need here for Merton plc to bring cost

of sales and operating costs under control in order to improve profitability.

Gearing and financial risk

Gearing as measured by debt/equity has fallen from 67% (2005) to 63% (2006) because of an increase in

shareholders’ funds through retained profits. Over the same period the overdraft has increased from £1m to £8m and

cash balances have fallen from £16m to £1m. This is a net movement of £22m. If the overdraft is included, gearing

has increased to 77% rather than falling to 63%.

None of these gearing levels compare favourably with the average gearing for the sector of 50%. If we consider the large

increase in the overdraft, financial risk has clearly increased during the period. This is also evidenced by the decline in

interest cover from 4·1 (2005) to 2·8 (2006) as operating profit has fallen and interest paid has increased. In each year

interest cover has been below the sector average of eight and the current level of 2·8 is dangerously low.

Share price

As the return required by equity investors increases with increasing financial risk, continued increases in the overdraft

will exert downward pressure on the company’s share price and further reductions may be expected.

Investor ratios

Earnings per share, dividend per share and dividend cover have all declined from 2005 to 2006. The cut in the dividend

per share from 8·5 pence per share to 7·5 pence per share is especially worrying. Although in its announcement the

company claimed that dividend growth and share price growth was expected, it could have chosen to maintain the

dividend, if it felt that the current poor performance was only temporary. By cutting the dividend it could be signalling

that it expects the poor performance to continue. Shareholders have no guarantee as to the level of future dividends.

This view could be shared by the market, which might explain why the price-earnings ratio has fallen from 14 times to

12 times.

Financing strategy

Merton plc has experienced an increase in fixed assets over the last period of £10m and an increase in stocks and

debtors of £21m. These increases have been financed by a decline in cash (£15m), an increase in the overdraft (£7m)

and an increase in trade credit (£6m). The company is following an aggressive strategy of financing long-term

investment from short-term sources. This is very risky, since if the overdraft needed to be repaid, the company would

have great difficulty in raising the funds required.

A further financing issue relates to redemption of the existing debentures. The 10% debentures are due to be redeemed

in two years’ time and Merton plc will need to find £13m in order to do this. It does not appear that this sum can be

raised internally. While it is possible that refinancing with debt paying a lower rate of interest may be possible, the low

level of interest cover may cause concern to potential providers of debt finance, resulting in a higher rate of interest. The

Finance Director of Merton plc needs to consider the redemption problem now, as thought is currently being given to

raising a substantial amount of new equity finance. This financing choice may not be available again in the near future,

forcing the company to look to debt finance as a way of effecting redemption.

Overtrading

The evidence produced by the financial analysis above is that Merton plc is showing some symptoms of overtrading

(undercapitalisation). The board are suggesting a rights issue as a way of financing an expansion of business, but it is

possible that a rights issue will be needed to deal with the overtrading problem. This is a further financing issue requiring

consideration in addition to the redemption of debentures mentioned earlier.

Conclusion

Ordinary shareholders need to be aware of the following issues.

1. Profitability has fallen over the last year due to poor cost control

2. A substantial increase in the overdraft over the last year has caused gearing to increase

3. It is possible that the share price will continue to fall

4. The dividend cut may warn of continuing poor performance in the future

5. A total of £13m of debentures need redeeming in two year’s time

6. A large amount of new finance is needed for working capital and debenture redemption

Appendix: Analysis of key ratios and financial information

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-05-02

- 2020-03-28

- 2020-05-09

- 2020-01-07

- 2020-01-10

- 2020-01-11

- 2020-01-09

- 2020-04-20

- 2020-05-05

- 2020-03-22

- 2019-07-19

- 2020-03-27

- 2020-05-20

- 2020-03-13

- 2020-01-09

- 2020-01-09

- 2020-01-10

- 2020-03-26

- 2020-02-02

- 2020-01-09

- 2020-02-28

- 2020-01-09

- 2019-07-19

- 2020-02-13

- 2020-03-15

- 2020-01-09

- 2020-05-14

- 2020-01-09

- 2020-03-22

- 2020-03-18