ACCA考试报名时间已公布,报名前全国考生要这么备考!

发布时间:2020-01-10

早在2019年年末的时候就公布了ACCA考试报名时间,备考的你知道吗?同时,很多小伙伴来咨询51题库考试学习网,想问问ACCA考试那么多科目应该怎么样有效地、科学地复习呢?不用担心,51题库考试学习网帮大家整理了一些考试小技巧,帮助大家事半功倍地通过考试,早日脱坑:

可能有些初次备考ACCA考试的萌新不了解报名时间,51题库考试学习网再次提醒大家2020年ACCA考试的报名时间:

2020年3月ACCA考试报名时间报名周期

提前报名截止 2019年11月11日

常规报名截止 2020年1月27日

后期报名截止 2020年2月3日

2020年6月ACCA考试报名时间报名周期

提前报名截止 2020年2月10日

常规报名截止 2020年4月27日

后期报名截止 2020年5月4日

2020年9月ACCA考试报名时间报名周期

提前报名截止 2020年5月11日

常规报名截止: 2020年7月27日

后期报名截止 2020年8月3日

2020年12月ACCA考试报名时间报名周期

提前报名截止 2020年8月10日

常规报名截止 2020年10月26日

后期报名截止 2020年11月2日

AB(F1)

AB(F1)这门课,首先要从题型出发来分析:目前AB(F1)的题型主要是46个单选题+6个多任务题;因此,从题型上来看就可以分析得知大部分内容其实不需要考生去原封不动地去死记硬背知识点,更多的是要求考生理解性记忆,比如它会教大家用一些模型去分析企业所处的内部以及外部环境,所以考生所学的的是它如何分析这个模型的这种方法,活学活用才能以不变应万变。同时,它还会教一些关于职业道德,企业社会责任的简单介绍。

说到AB(F1),就不得不说SBL课程,其实它们两者是有重复的地方的,就比如SBL课程会把这些AB(F1)课程中的知识点做深入并细化地讲解,就好比分析内外部环境之后企业将如何面对环境的变化、企业在专业层面上的战略,以及在公司治理,财务从业人员的职业道德等做了更深入且全面的介绍。总而言之,AB(F1)是基础,而SBL课程就是延伸。

但考生需要注意的事情就是:因为国家对ACCA考试规则做了限制,你是没有办法同时报考AB(F1)与SBL两个科目的,因为中间还隔着F4-F9 6门技能课程。所以你能做的就是打好基础。对于备考SBL,AB(F1)的知识点是大量的基础知识,所以要注意在考过AB(F1)之后依然需要巩固和记忆相关的知识点,不要把所学的知识点给遗忘了,如果到时候重新来复习的话,就太浪费时间了。

文字类考试对考生的记忆力的要求是极高的,不光要求考生要记忆从中的知识点并且是要熟练记忆。因此51题库考试学习网建议在选择考试科目时要避免选择同时备考多科需要高强度记忆的考试科目,例如F4《Corporate and Business law》以及F8《Audit and Assurance》,如果这些同时备考的话,会增加记忆难度,间接地导致学习效果的下降,最后导致考试成绩的不理想,所以不建议在同一考季中备考多个文字类考试。但是,51题库考试学习网推荐在相邻两个考季中参加考试(比如2020年6月份准备F4,那么2020年6月份就准备F8),因为文字类考试的内容或多或少是有重叠的部分的,区别仅仅在于侧重点不同,识记内容有重叠部分;就比如F8学得很扎实的小伙伴对于后面的学习SBL或者选修高级审计与鉴证《Advanced Audit and Assurance(AAA)》是赢在了起跑线上的,优势是十分巨大的。这就是为什么有一些考神能一次性通过ACCA考试的原因:合理地、科学地、有目的性地、高效地去学习,巧用复习方法能让你的学习效果事半功倍。

F2《Management Accounting》、F5业绩管理《Performance Management》和F9选修高级业绩管理《Advanced Performance Management》

同理,对于F2《Management Accounting》、F5业绩管理《Performance Management》和F9选修高级业绩管理《Advanced Performance Management》。F2课程内容是F5和选修高级业绩管理的基础,三科课程内容都涉及管理会计与财务会计的区别,涵盖:管理会计,管理信息,成本会计,预算和标准成本,业绩衡量,短期决策方法。同样,差别也仅仅是在于侧重点以及研究深度和广度的不同而已。因此,51题库考试学习网建议学习能力强一点的考生将F2和F5考虑同时学习,而学习能力偏弱的考试就先学F2再学F5;在选择报考科目的时间上,建议将F2、F5以及选修高级业绩管理这三科在相邻考季中备考,因为F2中的variance,在F5中体现更加灵活、更加具体。先学F2,再看F5,F2比较简单,很多常识的知识,为F5打好基础,也加深对F2的理解。在这些学科中,ACCAer们将会学到:如何处理基本的成本信息,并能向管理层提供能用作预算和决策的信息。而与此同时,F9科目又是F5升级版,课程研究的更加具体化和形象化,但是RATIO部分是一样的,所以51题库考试学习网建议可以将F5和F9放在同一考季去考试。

F6和P6高级税务《Advanced Taxation》

如果你有选修学习P6高级税务《Advanced Taxation》的打算,可以建议把F6放在F阶段最后一门,在考完F6考试之后,就赶紧学习P6。因为,F6《Taxation》是P6《Advanced Taxation》的直接基础。这门课程涵盖:英国税收体制,个人所得税,企业所得税,资本利得税,增值税,遗产税这五大税种应交税额的计算以及基于个人收入缴纳的国民保险和养老金投资的计算。F6考试中以税负计算为主,而P6更偏向在熟悉税法规定后,帮客户做合理纳税筹划。为什么不将F6和P6在同一考季报考呢?也是由于国家的相关规定,禁止在同一考季报考的,因此在考完F6考试之后,就赶紧学习P6。可以安排在同一年度相邻考季考这两门是最好的,因为两个科目中的相关知识点,例如:税率不变也不用重新记;科目类别要选择一致的,例如F6选择了UK ,P6也就选择UK,但是这样选择存在一个弊端就是,由于在中国P6这门课程学习的人不多,学习资料与课程也很少,如果将F6和P6放在两个相邻,备考时间相对较紧凑,对于资料不好找的科目可能复习到的知识点可能存在不太全面的问题。因此,同学们应根据自身需求谨慎选择。

P2和F7

P2在2018年9月改革为新科目SBR(Strategic Business Reporting)。课程涵盖是十分广泛的,例如:财务会计,财务报表,公司合并报表,分析并解读财务报表。P2的核心就是:让你如何运用合理地会计准则和概念框架编制财务报表同时又能够分析并解读财务报表。不难发现的是:P2有一大部分是重复F7的内容,但是由于ACCA考试规则规定了必须F阶段考试全部通过完毕之后才能报考P阶段,所以51题库考试学习网建议考生在考完F阶段考试之后,可以在下一次考试先考P2,将F7的知识点灵活运用。

如果想要学习4选2的P4的话,可以再F9考完之后学习P4,P4《Advanced Financial Management》是F9《Financial Management》的延伸考查,与SBR也有一定的联系。

课程涵盖:高级投资评估,公司并购、重组,高级风险管理,跨国公司面临的经济环境,您将会学到作为一名高级财务人员进行与财务管理相关决策必备的知识、技巧和进行职业判断的能力。

F8《Audit Assurance》是P7《Advanced Audit Assurance》的直接基础,与F3,F7,SBL等课程都有一定的关系。

F8课程中涵盖:内部审计和外部审计以及设计建立及实施内控程序,重点学习审计师如何了解企业情况,对审计风险进行评估,制定审计计划,在国际审计准则下如何进行设计,建立并实施审计程序,以及各种审计报告和审计意见。

P7是F8的延伸,与p2也有一定的联系。从三个科目之间存在的共同点可以看出:F7和P2主要学习如何编制财务报表,F8和P7学习如何审计财务报表。

P7课程涵盖:监管环境与制度,职业道德,实务管理,历史财务信息的审计与报告,其它与审计相关的认证业务。

在这里要提醒各位小伙伴们,ACCA在P阶段从P4到P7是选修科目,学员们只要选择学习两门并通过考试就可以了。但这4门选修科目却基本通向不同的工作领域。

P4《Advanced Financial Management》更偏向金融方面,想去投行券商的小伙伴们可以考虑选择P4

P5《Advanced Performance Management》偏向财务管理方向,如果对分析公司财务状况以及咨询岗位感兴趣的小伙伴可以选择P5

P6《Advanced Taxation》及P7《Advanced Audit Assurance》可以让各位学员们对税法以及审计准则的知识熟练掌握,对于想在事务所工作的小伙伴们是不错的选择。

鲤鱼不跃,岂可成龙?大鹏驻足,焉能腾空?十年磨刀霍霍,只为今朝一搏。最后51题库考试学习网祝大家都能顺利通过ACCA,取得好成绩!

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(c) Explain the benefits of performance-related pay in rewarding directors and critically evaluate the implications

of the package offered to Choo Wang. (8 marks)

(c) Choo Wang’s remuneration package

Benefits of PRP

In general terms, performance-related pay serves to align directors’ and shareholders’ interests in that the performancerelated

element can be made to reflect those things held to be important to shareholders (such as financial targets). This, in

turn, serves to motivate directors, especially if they are directly responsible for a cost or revenue/profit budget or centre. The

possibility of additional income serves to motivate directors towards higher performance and this, in turn, can assist in

recruitment and retention. Finally, performance-related pay can increase the board’s control over strategic planning and

implementation by aligning rewards against strategic objectives.

Critical evaluation of Choo Wang’s package

Choo Wang’s package appears to have a number of advantages and shortcomings. It was strategically correct to include some

element of pay linked specifically to Southland success. This will increase Choo’s motivation to make it successful and indeed,

he has said as much – he appears to be highly motivated and aware that additional income rests upon its success. Against

these advantages, it appears that the performance-related component does not take account of, or discount in any way for,

the risk of the Southland investment. The bonus does not become payable on a sliding scale but only on a single payout basis

when the factory reaches an ‘ambitious’ level of output. Accordingly, Choo has more incentive to be accepting of risk with

decisions on the Southland investment than risk averse. This may be what was planned, but such a bias should be pointed

out. Clearly, the company should accept some risk but recklessness should be discouraged. In conclusion, Choo’s PRP

package could have been better designed, especially if the Southland investment is seen as strategically risky.

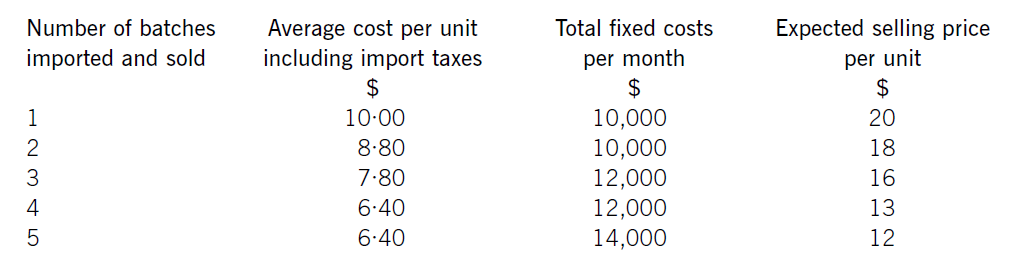

Jewel Co is setting up an online business importing and selling jewellery headphones. The cost of each set of headphones varies depending on the number purchased, although they can only be purchased in batches of 1,000 units. It also has to pay import taxes which vary according to the quantity purchased.

Jewel Co has already carried out some market research and identified that sales quantities are expected to vary depending on the price charged. Consequently, the following data has been established for the first month:

Required:

(a) Calculate how many batches Jewel Co should import and sell. (6 marks)

(b) Explain why Jewel Co could not use the algebraic method to establish the optimum price for its product.

(4 marks)

(b)Thealgebraicmodelrequiresseveralassumptionstobetrue.First,theremustbeaconsistentrelationshipbetweenprice(P)anddemand(Q),sothatademandequationcanbeestablished,usuallyintheform.P=a–bQ.Here,althoughthereisaclearrelationshipbetweenthetwo,itisnotaperfectlylinearrelationshipandsomorecomplicatedtechniquesarerequiredtocalculatethedemandequation.ItalsocannotbeassumedthatalinearrelationshipwillholdforallvaluesofPandQotherthanthefivegiven.Similarly,theremustbeaclearrelationshipbetweendemandandmarginalcost,usuallysatisfiedbyconstantvariablecostperunitandconstantfixedcosts.Thechangingvariablecostsperunitagaincomplicatetheissue,butitisthechangesinfixedcostswhichmakethealgebraicmethodlessusefulinJewel’scase.Thealgebraicmodelisonlysuitableforcompaniesoperatinginamonopolyanditisnotclearherewhetherthisisthecase,butitseemsunlikely,soany‘optimum’pricemightbecomeirrelevantifJewel’scompetitorschargesignificantlylowerprices.Othermoregeneralfactorsnotconsideredbythealgebraicmodelarepoliticalfactorswhichmightaffectimports,socialfactorswhichmayaffectcustomertastesandeconomicfactorswhichmayaffectexchangeratesorcustomerspendingpower.Thereliabilityoftheestimatesthemselves–forsalesprices,variablecostsandfixedcosts–couldalsobecalledintoquestion.

(ii) Explain why the disclosure of voluntary information in annual reports can enhance the company’s

accountability to equity investors. (4 marks)

(ii) Accountability to equity investors

Voluntary disclosures are an effective way of redressing the information asymmetry that exists between management and

investors. In adding to mandatory content, voluntary disclosures give a fuller picture of the state of the company.

More information helps investors decide whether the company matches their risk, strategic and ethical criteria, and

expectations.

Makes the annual report more forward looking (predictive) whereas the majority of the numerical content is backward

facing on what has been.

Helps transparency in communicating more fully thereby better meeting the agency accountability to investors,

particularly shareholders.

There is a considerable amount of qualitative information that cannot be conveyed using statutory numbers (such as

strategy, ethical content, social reporting, etc).

Voluntary disclosure gives a more rounded and more complete view of the company, its activities, strategies, purposes

and values.

Voluntary disclosure enables the company to address specific shareholder concerns as they arise (such as responding

to negative publicity).

[Tutorial note: other valid points will attract marks]

(ii) State when the inheritance tax (IHT) calculated in (i) would be payable and by whom. (2 marks)

(ii) Inheritance tax administration

The tax on Debbie’s estate (personalty and realty) would be paid by the personal representatives, usually an executor.

Inheritance tax is due six months from the end of the month in which death occurred (31 December 2005) or the date

on which probate is obtained (if earlier). However, an instalment option is available for certain assets, which includes

land and buildings i.e. the residence whereby the tax can be paid in 10 equal annual instalments.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-01-09

- 2020-01-09

- 2020-03-25

- 2021-08-29

- 2020-01-10

- 2020-01-10

- 2020-01-09

- 2019-03-27

- 2019-03-16

- 2020-01-10

- 2019-06-27

- 2020-04-15

- 2020-01-10

- 2020-01-10

- 2020-02-12

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-08-05

- 2020-01-10

- 2020-04-14

- 2020-01-09

- 2020-01-10

- 2020-01-01

- 2020-01-09

- 2020-01-10

- 2020-03-07

- 2020-05-05

- 2020-01-10

- 2020-01-10