ACCA考试前都应该准备些什么呢?

发布时间:2021-03-12

ACCA考试前都应该准备些什么呢?

最佳答案

考试时需要携带注册卡、准考证、黑色签字笔、铅笔、橡皮、尺子、计算器(无声、无翻译功能)等文具;若注册卡丢失,可以携带本人身份证代替注册卡。如果没有收到从英国直接邮寄过来的准考证,请直接从网上下载,也可以使用。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(ii) Recommend further audit procedures that should be carried out. (4 marks)

(ii) Further audit procedures:

Request from Peter Sheffield a written representation detailing:

– the exact nature of his control over Jarvis Co, i.e. if he is a shareholder then state his percentage shareholding, if

he is a member of senior management then state his exact position within the entity,

– a comment on whether in his opinion the balance is recoverable,

– a specific date by which the amount should be expected to be repaid, and

– a confirmation that there are no further balances outstanding from Jarvis Co, or any further transactions between

Jarvis Co and Pulp Co.

Tutorial note: Reference to the Exposure Draft ISA 550 Related Parties (Revised and Redrafted) requirement for both

general and specific management representations will be awarded credit.

Review the terms of any written confirmation of the amount, such as a signed agreement or invoice, checking whether

any interest is due to Pulp Co. The terms should be reviewed for details of any security offered, and the nature of the

consideration to be provided in settlement.

From discussion with Peter Sheffield, develop an understanding of the business purpose of the transaction, particularly

to understand whether the balance is a trade receivable or an investment.

Review the board minutes for evidence of any discussion of the transaction and the recoverability of the balance

outstanding.

Obtain the most recent audited financial statements of Jarvis Co and:

– ascertain whether Peter Sheffield is disclosed as the ultimate controlling party or disclosed as a member of key

management personnel,

– scrutinise the disclosure notes to find any disclosure of the transaction, where it should be described as a related

party liability, and

– perform. a liquidity analysis to establish whether the amount can be repaid from liquid assets.

(ii) the recent financial performance of Merton plc from a shareholder perspective. Clearly identify any

issues that you consider should be brought to the attention of the ordinary shareholders. (15 marks)

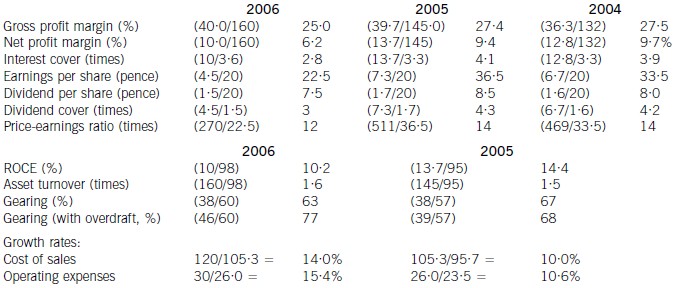

(ii) Discussion of financial performance

It is clear that 2006 has been a difficult year for Merton plc. There are very few areas of interest to shareholders where

anything positive can be found to say.

Profitability

Return on capital employed has declined from 14·4% in 2005, which compared favourably with the sector average of

12%, to 10·2% in 2006. Since asset turnover has improved from 1·5 to 1·6 in the same period, the cause of the decline

is falling profitability. Gross profit margin has fallen each year from 27·5% in 2004 to 25% in 2006, equal to the sector

average, despite an overall increase in turnover during the period of 10% per year. Merton plc has been unable to keep

cost of sales increases (14% in 2006 and 10% in 2005) below the increases in turnover. Net profit margin has declined

over the same period from 9·7% to 6·2%, compared to the sector average of 8%, because of substantial increases in

operating expenses (15·4% in 2006 and 10·6% in 2005). There is a pressing need here for Merton plc to bring cost

of sales and operating costs under control in order to improve profitability.

Gearing and financial risk

Gearing as measured by debt/equity has fallen from 67% (2005) to 63% (2006) because of an increase in

shareholders’ funds through retained profits. Over the same period the overdraft has increased from £1m to £8m and

cash balances have fallen from £16m to £1m. This is a net movement of £22m. If the overdraft is included, gearing

has increased to 77% rather than falling to 63%.

None of these gearing levels compare favourably with the average gearing for the sector of 50%. If we consider the large

increase in the overdraft, financial risk has clearly increased during the period. This is also evidenced by the decline in

interest cover from 4·1 (2005) to 2·8 (2006) as operating profit has fallen and interest paid has increased. In each year

interest cover has been below the sector average of eight and the current level of 2·8 is dangerously low.

Share price

As the return required by equity investors increases with increasing financial risk, continued increases in the overdraft

will exert downward pressure on the company’s share price and further reductions may be expected.

Investor ratios

Earnings per share, dividend per share and dividend cover have all declined from 2005 to 2006. The cut in the dividend

per share from 8·5 pence per share to 7·5 pence per share is especially worrying. Although in its announcement the

company claimed that dividend growth and share price growth was expected, it could have chosen to maintain the

dividend, if it felt that the current poor performance was only temporary. By cutting the dividend it could be signalling

that it expects the poor performance to continue. Shareholders have no guarantee as to the level of future dividends.

This view could be shared by the market, which might explain why the price-earnings ratio has fallen from 14 times to

12 times.

Financing strategy

Merton plc has experienced an increase in fixed assets over the last period of £10m and an increase in stocks and

debtors of £21m. These increases have been financed by a decline in cash (£15m), an increase in the overdraft (£7m)

and an increase in trade credit (£6m). The company is following an aggressive strategy of financing long-term

investment from short-term sources. This is very risky, since if the overdraft needed to be repaid, the company would

have great difficulty in raising the funds required.

A further financing issue relates to redemption of the existing debentures. The 10% debentures are due to be redeemed

in two years’ time and Merton plc will need to find £13m in order to do this. It does not appear that this sum can be

raised internally. While it is possible that refinancing with debt paying a lower rate of interest may be possible, the low

level of interest cover may cause concern to potential providers of debt finance, resulting in a higher rate of interest. The

Finance Director of Merton plc needs to consider the redemption problem now, as thought is currently being given to

raising a substantial amount of new equity finance. This financing choice may not be available again in the near future,

forcing the company to look to debt finance as a way of effecting redemption.

Overtrading

The evidence produced by the financial analysis above is that Merton plc is showing some symptoms of overtrading

(undercapitalisation). The board are suggesting a rights issue as a way of financing an expansion of business, but it is

possible that a rights issue will be needed to deal with the overtrading problem. This is a further financing issue requiring

consideration in addition to the redemption of debentures mentioned earlier.

Conclusion

Ordinary shareholders need to be aware of the following issues.

1. Profitability has fallen over the last year due to poor cost control

2. A substantial increase in the overdraft over the last year has caused gearing to increase

3. It is possible that the share price will continue to fall

4. The dividend cut may warn of continuing poor performance in the future

5. A total of £13m of debentures need redeeming in two year’s time

6. A large amount of new finance is needed for working capital and debenture redemption

Appendix: Analysis of key ratios and financial information

(ii) On 1 July 2006 Petrie introduced a 10-year warranty on all sales of its entire range of stainless steel

cookware. Sales of stainless steel cookware for the year ended 31 March 2007 totalled $18·2 million. The

notes to the financial statements disclose the following:

‘Since 1 July 2006, the company’s stainless steel cookware is guaranteed to be free from defects in

materials and workmanship under normal household use within a 10-year guarantee period. No provision

has been recognised as the amount of the obligation cannot be measured with sufficient reliability.’

(4 marks)

Your auditor’s report on the financial statements for the year ended 31 March 2006 was unmodified.

Required:

Identify and comment on the implications of these two matters for your auditor’s report on the financial

statements of Petrie Co for the year ended 31 March 2007.

NOTE: The mark allocation is shown against each of the matters above.

(ii) 10-year guarantee

$18·2 million stainless steel cookware sales amount to 43·1% of revenue and are therefore material. However, the

guarantee was only introduced three months into the year, say in respect of $13·6 million (3/4 × 18·2 million) i.e.

approximately 32% of revenue.

The draft note disclosure could indicate that Petrie’s management believes that Petrie has a legal obligation in respect

of the guarantee, that is not remote and likely to be material (otherwise no disclosure would have been required).

A best estimate of the obligation amounting to 5% profit before tax (or more) is likely to be considered material, i.e.

$90,000 (or more). Therefore, if it is probable that 0·66% of sales made under guarantee will be returned for refund,

this would require a warranty provision that would be material.

Tutorial note: The return of 2/3% of sales over a 10-year period may well be probable.

Clearly there is a present obligation as a result of a past obligating event for sales made during the nine months to

31 March 2007. Although the likelihood of outflow under the guarantee is likely to be insignificant (even remote) it is

probable that some outflow will be needed to settle the class of such obligations.

The note in the financial statements is disclosing this matter as a contingent liability. This term encompasses liabilities

that do not meet the recognition criteria (e.g. of reliable measurement in accordance with IAS 37 Provisions, Contingent

Liabilities and Contingent Assets).

However, it is extremely rare that no reliable estimate can be made (IAS 37) – the use of estimates being essential to

the preparation of financial statements. Petrie’s management must make a best estimate of the cost of refunds/repairs

under guarantee taking into account, for example:

■ the proportion of sales during the nine months to 31 March 2007 that have been returned under guarantee at the

balance sheet date (and in the post balance sheet event period);

■ the average age of cookware showing a defect;

■ the expected cost of a replacement item (as a refund of replacement is more likely than a repair, say).

If management do not make a provision for the best estimate of the obligation the audit opinion should be qualified

‘except for’ non-compliance with IAS 37 (no provision made). The disclosure made in the note to the financial

statements, however detailed, is not a substitute for making the provision.

Tutorial note: No marks will be awarded for suggesting that an emphasis of matter of paragraph would be appropriate

(drawing attention to the matter more fully explained in the note).

Management’s claim that the obligation cannot be measured with sufficient reliability does not give rise to a limitation

on scope on the audit. The auditor has sufficient evidence of the non-compliance with IAS 37 and disagrees with it.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2021-04-16

- 2021-01-04

- 2021-03-10

- 2021-07-01

- 2021-03-10

- 2021-04-15

- 2021-03-10

- 2021-03-12

- 2021-03-12

- 2021-03-11

- 2021-03-11

- 2021-04-14

- 2021-04-23

- 2021-04-14

- 2021-05-06

- 2021-06-05

- 2021-04-16

- 2021-05-27

- 2021-03-10

- 2021-03-12

- 2021-06-04

- 2021-05-30

- 2021-04-14

- 2021-03-12

- 2021-03-12

- 2021-03-12

- 2021-05-13

- 2021-04-22

- 2021-05-15

- 2021-03-12