如何选择适合自己的acca课程上课方式?

发布时间:2021-10-17

备考acca的小伙伴们多多少少都了解过acca的课程,课程学习的种类较多,可以说零零总总,眼花缭乱,其实仔细观察,课程内容大都差不多。那么如何选择适合自己的课程呢?下面就给大家分享一下。

一、应该如何选择课程?

一般来说课程分为网课,直播课,面授课三种。

1、网课。如果自身就是相关专业的,同时基础比较好的话,可以选择网课的形式,一方面价格相对来说会低一些,而且上课地点灵活,网络通畅的情况下,随时随地都可以进行学习,另一方面,由于自身有一定的基础,可以跟随网课系统学习,把握考点难点。但是网课也有一定的弊端,因为是网上学习没有人监督,自觉性不强的同学在学习过程中就很容易分心。

2、直播课。直播课兼具网课的优点,在授课过程中如果存在疑虑,可以直接与老师进行互动,一般来说直播课时间是比较固定的,灵活性会低一些,直播过程中学员的人数较多,授课老师可能无法兼顾每一位同学的问题。

3、面授课。面授课的优势在于一般情况下学员人数不会太多,老师通常可以照顾到每一位学员的感受,根据学员的课堂反应及时调整授课计划,在一定程度上能够对学员的听课情况进行监督,互动性更强,是上课效果比较好的一个选择。缺点是时间比较固定,价格可能会略高一些。

二、如何选择acca培训机构?

1、机构规模。机构规模是应对风险、防范风险的重要指标。可以通过了解备选培训机构的规模是否有扩张、在同一个城市有没有开设新的培训点,以及各培训网点的场地、人员情况。

2、教学和研发水平。对于培训机构来说,教学和研发水平是最主要的竞争力,在进行选择、考量的同时,教学水平是首要关注的地方,可以了解不同机构之间课程内容和授课形式的区别,选择最适合自己的课程。

3、服务质量。不仅仅要关注教学,服务也是至关重要的衡量指标。有没有承诺不到位的,有没有随便更改时间却不通知学员的,信息有没有记事本和学员沟通,封锁学员和外界接触渠道的等等,这些都是需要进行考量的。同时签订合同的时候也要特别注意细节,以免落入陷阱。

以上就是关于如何选择acca课程的全部内容啦!希望对大家有所帮助,想了解更多acca考试相关资讯,可以关注51题库考试学习网,51题库考试学习网将竭诚为您服务。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(d) Additionally Router purchased 60% of the ordinary shares of a radio station, Playtime, a public limited company,

on 31 May 2007. The remaining 40% of the ordinary shares are owned by a competitor company who owns a

substantial number of warrants issued by Playtime which are currently exercisable. If these warrants are

exercised, they will result in Router only owning 35% of the voting shares of Playtime. (4 marks)

Required:

Discuss how the above items should be dealt with in the group financial statements of Router for the year ended

31 May 2007.

(d) IAS27 paragraph 14, ‘Consolidated and Separate Financial Statements’, states that warrants that have the potential to give

the holder voting power or reduce another party’s voting power over the financial and operating policies of the issuer should

be considered when existence of control is assessed. The warrants held by the competitor company, if exercised, would grant

that company control over Playtime. One party only can control Playtime and, therefore, the competitor company should

consolidate Playtime. In coming to this decision all the facts and circumstances that affect potential voting rights (except the

intention of management and the financial ability to exercise or convert) should be considered. It seems, however, that there

is a prima facie case for not consolidating Playtime but accounting for it under IAS28 or IAS39.

(b) Explain how the process of developing scenarios might help John better understand the macro-environmental

factors influencing Airtite’s future strategy. (8 marks)

(b) Carrying out a systematic PESTEL analysis is a key step in developing alternative scenarios about the future. Johnson and

Scholes define scenarios as ‘detailed and plausible views of how the business environment of an organisation might develop

in the future based on groupings of key environmental influences and drivers of change about which there is a high level of

uncertainty’. In developing scenarios it is necessary to isolate the key drivers of change, which have the potential to have a

significant impact on the company and are associated with high levels of uncertainty. Development of scenarios enables

managers to share assumptions about the future and the key variables shaping that future. This provides an opportunity for

real organisational learning. They are then in a position to monitor these key variables and amend strategies accordingly. It

is important to note that different stakeholder groups will have different expectations about the future and each may provide

a key input to the process of developing scenarios. By their very nature scenarios should not attempt to allocate probabilities

to the key factors and in so doing creating ‘spurious accuracy’ about those factors. A positive scenario is shown below and

should provide a shared insight into the external factors most likely to have a significant impact on Airtite‘s future strategy.

For most companies operating in global environments the ability to respond flexibly and quickly to macro-environmental

change would seem to be a key capability.

The scenario as illustrated below, clearly could have a major impact on the success or otherwise of Airtite’s strategy for the

future. The key drivers for change would seem to be the link between technology and global emissions, fuel prices and the

stability of the global political environment. Through creating a process which considers the drivers which will have most

impact on Airtite and which are subject to the greatest uncertainty, Airtite will have a greater chance of its strategy adaptingto changing circumstances.

(ii) the recent financial performance of Merton plc from a shareholder perspective. Clearly identify any

issues that you consider should be brought to the attention of the ordinary shareholders. (15 marks)

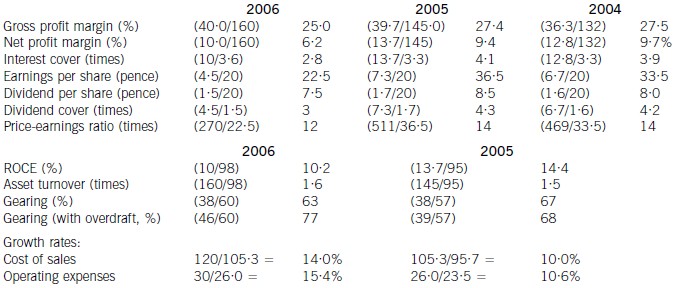

(ii) Discussion of financial performance

It is clear that 2006 has been a difficult year for Merton plc. There are very few areas of interest to shareholders where

anything positive can be found to say.

Profitability

Return on capital employed has declined from 14·4% in 2005, which compared favourably with the sector average of

12%, to 10·2% in 2006. Since asset turnover has improved from 1·5 to 1·6 in the same period, the cause of the decline

is falling profitability. Gross profit margin has fallen each year from 27·5% in 2004 to 25% in 2006, equal to the sector

average, despite an overall increase in turnover during the period of 10% per year. Merton plc has been unable to keep

cost of sales increases (14% in 2006 and 10% in 2005) below the increases in turnover. Net profit margin has declined

over the same period from 9·7% to 6·2%, compared to the sector average of 8%, because of substantial increases in

operating expenses (15·4% in 2006 and 10·6% in 2005). There is a pressing need here for Merton plc to bring cost

of sales and operating costs under control in order to improve profitability.

Gearing and financial risk

Gearing as measured by debt/equity has fallen from 67% (2005) to 63% (2006) because of an increase in

shareholders’ funds through retained profits. Over the same period the overdraft has increased from £1m to £8m and

cash balances have fallen from £16m to £1m. This is a net movement of £22m. If the overdraft is included, gearing

has increased to 77% rather than falling to 63%.

None of these gearing levels compare favourably with the average gearing for the sector of 50%. If we consider the large

increase in the overdraft, financial risk has clearly increased during the period. This is also evidenced by the decline in

interest cover from 4·1 (2005) to 2·8 (2006) as operating profit has fallen and interest paid has increased. In each year

interest cover has been below the sector average of eight and the current level of 2·8 is dangerously low.

Share price

As the return required by equity investors increases with increasing financial risk, continued increases in the overdraft

will exert downward pressure on the company’s share price and further reductions may be expected.

Investor ratios

Earnings per share, dividend per share and dividend cover have all declined from 2005 to 2006. The cut in the dividend

per share from 8·5 pence per share to 7·5 pence per share is especially worrying. Although in its announcement the

company claimed that dividend growth and share price growth was expected, it could have chosen to maintain the

dividend, if it felt that the current poor performance was only temporary. By cutting the dividend it could be signalling

that it expects the poor performance to continue. Shareholders have no guarantee as to the level of future dividends.

This view could be shared by the market, which might explain why the price-earnings ratio has fallen from 14 times to

12 times.

Financing strategy

Merton plc has experienced an increase in fixed assets over the last period of £10m and an increase in stocks and

debtors of £21m. These increases have been financed by a decline in cash (£15m), an increase in the overdraft (£7m)

and an increase in trade credit (£6m). The company is following an aggressive strategy of financing long-term

investment from short-term sources. This is very risky, since if the overdraft needed to be repaid, the company would

have great difficulty in raising the funds required.

A further financing issue relates to redemption of the existing debentures. The 10% debentures are due to be redeemed

in two years’ time and Merton plc will need to find £13m in order to do this. It does not appear that this sum can be

raised internally. While it is possible that refinancing with debt paying a lower rate of interest may be possible, the low

level of interest cover may cause concern to potential providers of debt finance, resulting in a higher rate of interest. The

Finance Director of Merton plc needs to consider the redemption problem now, as thought is currently being given to

raising a substantial amount of new equity finance. This financing choice may not be available again in the near future,

forcing the company to look to debt finance as a way of effecting redemption.

Overtrading

The evidence produced by the financial analysis above is that Merton plc is showing some symptoms of overtrading

(undercapitalisation). The board are suggesting a rights issue as a way of financing an expansion of business, but it is

possible that a rights issue will be needed to deal with the overtrading problem. This is a further financing issue requiring

consideration in addition to the redemption of debentures mentioned earlier.

Conclusion

Ordinary shareholders need to be aware of the following issues.

1. Profitability has fallen over the last year due to poor cost control

2. A substantial increase in the overdraft over the last year has caused gearing to increase

3. It is possible that the share price will continue to fall

4. The dividend cut may warn of continuing poor performance in the future

5. A total of £13m of debentures need redeeming in two year’s time

6. A large amount of new finance is needed for working capital and debenture redemption

Appendix: Analysis of key ratios and financial information

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-01-10

- 2020-01-30

- 2020-08-14

- 2020-04-22

- 2020-02-28

- 2020-01-10

- 2020-01-10

- 2020-01-09

- 2020-01-09

- 2020-01-10

- 2020-02-02

- 2020-03-29

- 2020-04-23

- 2019-04-13

- 2020-01-09

- 2020-05-20

- 2020-01-09

- 2020-05-10

- 2020-01-09

- 2020-02-12

- 2020-03-08

- 2019-11-28

- 2020-01-10

- 2020-01-10

- 2020-04-20

- 2020-02-20

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-01-10