要参加ACCA考试,需要准备哪些学习资料?

发布时间:2020-03-26

ACCA资格被认为是"国际财会界的通行证",许多国家立法许可ACCA会员从事审计、投资顾问和破产执行工作。ACCA在国内称为"国际注册会计师"。随着ACCA报考者的日益增多,很多同学纷纷前来询问,报考ACCA所需要准备的学习资料有哪些?接下来,由51题库考试学习网为大家介绍一下吧!

一、ACCA历年真题

ACCA历年真题可以说是制胜法宝了,如果你认真对待真题,你会发现很多题目都是有固定套路的,熟悉之后就可以立即拿到相应分数。一定要重视真题,反复训练。

二、ACCA考官文章

这里敲黑板,Technical Articles很重要。Technical Articles是ACCA考试小组出品,对于大纲中的重点,难点,新增点,学生的薄弱点,教材中阐述不够深入的点以及实务中非常重要的点,专门编写的,其重要程度可想而知。

三、ACCA考试大纲

ACCA考试大纲把每门课的知识点详细的列了出来。但是小编并不建议一直看考试大纲,因为看这个容易在details中迷失方向,抓不到重点。我们只要在学习前看看作为参考就可以了。

四、ACCA考官报告

这是ACCA考官对一次考试的评价,一是对考生的表现作出评判,二是反思考试出题的情况,有的考官会很明确的说某个知识点考生答得不好,以后还要加强考察,这就要注意了,加强准备为好。有的时候考官还会说明以后考试的侧重或者考法的变化,这也值得关注。总之,这是值得大家关注的考官资料,看上一次考试的 Examiner’s Report 就基本够了。

五、教材

1.我们需要BPP教材和练习册,BPP教材是全球ACCA使用最多的版本,通俗易懂,比较适合新老学员自学。推荐在F1-4选择BPP练习册,在F5-9两者兼可进行选。当然,对FTC版教材感兴趣的小伙伴也可以看看,但它比BPP教材难度稍大;

2.准备一本《会计双语英汉词典》对同学们是有益无害的,ACCA全英文考试需要同学们掌握很多的财会专业词汇,这样可以较好的理解文章语义。

以上,就是51题库考试学习网给大家分享的ACCA考试可供参考的学习资料,希望对小伙伴们有帮助。如果想了解更多其他信息,欢迎来51题库考试学习网留言咨询。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

In relation to the courts’ powers to interpret legislation, explain and differentiate between:

(a) the literal approach, including the golden rule; and (5 marks)

(b) the purposive approach, including the mischief rule. (5 marks)

Tutorial note:

In order to apply any piece of legislation, judges have to determine its meaning. In other words they are required to interpret the

statute before them in order to give it meaning. The diffi culty, however, is that the words in statutes do not speak for themselves and

interpretation is an active process, and at least potentially a subjective one depending on the situation of the person who is doing

the interpreting.

Judges have considerable power in deciding the actual meaning of statutes, especially when they are able to deploy a number of

competing, not to say contradictory, mechanisms for deciding the meaning of the statute before them. There are, essentially, two

contrasting views as to how judges should go about determining the meaning of a statute – the restrictive, literal approach and the

more permissive, purposive approach.

(a) The literal approach

The literal approach is dominant in the English legal system, although it is not without critics, and devices do exist for

circumventing it when it is seen as too restrictive. This view of judicial interpretation holds that the judge should look primarily

to the words of the legislation in order to construe its meaning and, except in the very limited circumstances considered below,

should not look outside of, or behind, the legislation in an attempt to fi nd its meaning.

Within the context of the literal approach there are two distinct rules:

(i) The literal rule

Under this rule, the judge is required to consider what the legislation actually says rather than considering what it might

mean. In order to achieve this end, the judge should give words in legislation their literal meaning, that is, their plain,

ordinary, everyday meaning, even if the effect of this is to produce what might be considered an otherwise unjust or

undesirable outcome (Fisher v Bell (1961)) in which the court chose to follow the contract law literal interpretation of

the meaning of offer in the Act in question and declined to consider the usual non-legal literal interpretation of the word

(offer).

(ii) The golden rule

This rule is applied in circumstances where the application of the literal rule is likely to result in what appears to the court

to be an obviously absurd result. It should be emphasised, however, that the court is not at liberty to ignore, or replace,

legislative provisions simply on the basis that it considers them absurd; it must fi nd genuine diffi culties before it declines

to use the literal rule in favour of the golden one. As examples, there may be two apparently contradictory meanings to a

particular word used in the statute, or the provision may simply be ambiguous in its effect. In such situations, the golden

rule operates to ensure that preference is given to the meaning that does not result in the provision being an absurdity.

Thus in Adler v George (1964) the defendant was found guilty, under the Offi cial Secrets Act 1920, with obstruction

‘in the vicinity’ of a prohibited area, although she had actually carried out the obstruction ‘inside’ the area.

(b) The purposive approach

The purposive approach rejects the limitation of the judges’ search for meaning to a literal construction of the words of

legislation itself. It suggests that the interpretative role of the judge should include, where necessary, the power to look beyond

the words of statute in pursuit of the reason for its enactment, and that meaning should be construed in the light of that purpose

and so as to give it effect. This purposive approach is typical of civil law systems. In these jurisdictions, legislation tends to set

out general principles and leaves the fi ne details to be fi lled in later by the judges who are expected to make decisions in the

furtherance of those general principles.

European Community (EC) legislation tends to be drafted in the continental manner. Its detailed effect, therefore, can only be

determined on the basis of a purposive approach to its interpretation. This requirement, however, runs counter to the literal

approach that is the dominant approach in the English system. The need to interpret such legislation, however, has forced

a change in that approach in relation to Community legislation and even with respect to domestic legislation designed to

implement Community legislation. Thus, in Pickstone v Freemans plc (1988), the House of Lords held that it was permissible,

and indeed necessary, for the court to read words into inadequate domestic legislation in order to give effect to Community

law in relation to provisions relating to equal pay for work of equal value. (For a similar approach, see also the House of Lords’

decision in Litster v Forth Dry Dock (1989) and the decision in Three Rivers DC v Bank of England (No 2) (1996).) However,

it has to recognise that the purposive rule is not particularly modern and has its precursor in a long established rule of statutory

interpretation, namely the mischief rule.

The mischief rule

This rule permits the court to go behind the actual wording of a statute in order to consider the problem that the statute is

supposed to remedy.

In its traditional expression it is limited by being restricted to using previous common law rules in order to decide the operation

of contemporary legislation. Thus in Heydon’s case (1584) it was stated that in making use of the mischief rule the court

should consider what the mischief in the law was which the common law did not adequately deal with and which statute law

had intervened to remedy. Use of the mischief rule may be seen in Corkery v Carpenter (1950), in which a man was found

guilty of being drunk in charge of a carriage although he was in fact only in charge of a bicycle.

4 You are a senior manager in Becker & Co, a firm of Chartered Certified Accountants offering audit and assurance

services mainly to large, privately owned companies. The firm has suffered from increased competition, due to two

new firms of accountants setting up in the same town. Several audit clients have moved to the new firms, leading to

loss of revenue, and an over staffed audit department. Bob McEnroe, one of the partners of Becker & Co, has asked

you to consider how the firm could react to this situation. Several possibilities have been raised for your consideration:

1. Murray Co, a manufacturer of electronic equipment, is one of Becker & Co’s audit clients. You are aware that the

company has recently designed a new product, which market research indicates is likely to be very successful.

The development of the product has been a huge drain on cash resources. The managing director of Murray Co

has written to the audit engagement partner to see if Becker & Co would be interested in making an investment

in the new product. It has been suggested that Becker & Co could provide finance for the completion of the

development and the marketing of the product. The finance would be in the form. of convertible debentures.

Alternatively, a joint venture company in which control is shared between Murray Co and Becker & Co could be

established to manufacture, market and distribute the new product.

2. Becker & Co is considering expanding the provision of non-audit services. Ingrid Sharapova, a senior manager in

Becker & Co, has suggested that the firm could offer a recruitment advisory service to clients, specialising in the

recruitment of finance professionals. Becker & Co would charge a fee for this service based on the salary of the

employee recruited. Ingrid Sharapova worked as a recruitment consultant for a year before deciding to train as

an accountant.

3. Several audit clients are experiencing staff shortages, and it has been suggested that temporary staff assignments

could be offered. It is envisaged that a number of audit managers or seniors could be seconded to clients for

periods not exceeding six months, after which time they would return to Becker & Co.

Required:

Identify and explain the ethical and practice management implications in respect of:

(a) A business arrangement with Murray Co. (7 marks)

4 Becker & Co

(a) Joint business arrangement

The business opportunity in respect of Murray Co could be lucrative if the market research is to be believed.

However, IFAC’s Code of Ethics for Professional Accountants states that a mutual business arrangement is likely to give rise

to self-interest and intimidation threats to independence and objectivity. The audit firm must be and be seen to be independent

of the audit client, which clearly cannot be the case if the audit firm and the client are seen to be working together for a

mutual financial gain.

In the scenario, two options are available. Firstly, Becker & Co could provide the audit client with finance to complete the

development and take the product to market. There is a general prohibition on audit firms providing finance to their audit

clients. This would create a clear financial self-interest threat as the audit firm would be receiving a return on investment from

their client. The Code states that if a firm makes a loan (or guarantees a loan) to a client, the self-interest threat created would

be so significant that no safeguard could reduce the threat to an acceptable level.

The provision of finance using convertible debentures raises a further ethical problem, because if the debentures are ultimately

converted to equity, the audit firm would then hold equity shares in their audit client. This is a severe financial self-interest,

which safeguards are unlikely to be able to reduce to an acceptable level.

The finance should not be advanced to Murray Co while the company remains an audit client of Becker & Co.

The second option is for a joint venture company to be established. This would be perceived as a significant mutual business

interest as Becker & Co and Murray Co would be investing together, sharing control and sharing a return on investment in

the form. of dividends. IFAC’s Code of Ethics states that unless the relationship between the two parties is clearly insignificant,

the financial interest is immaterial, and the audit firm is unable to exercise significant influence, then no safeguards could

reduce the threat to an acceptable level. In this case Becker & Co may not enter into the joint venture arrangement while

Murray Co is still an audit client.

The audit practice may consider that investing in the new electronic product is a commercial strategy that it wishes to pursue,

either through loan finance or using a joint venture arrangement. In this case the firm should resign as auditor with immediate

effect in order to eliminate any ethical problem with the business arrangement. The partners should carefully consider if the

potential return on investment will more than compensate for the lost audit fee from Murray Co.

The partners should also reflect on whether they want to diversify to such an extent – this investment is unlikely to be in an

area where any of the audit partners have much knowledge or expertise. A thorough commercial evaluation and business risk

analysis must be performed on the new product to ensure that it is a sound business decision for the firm to invest.

The audit partners should also consider how much time they would need to spend on this business development, if they

decided to resign as auditors and to go ahead with the investment. Such a new and important project could mean that they

take their focus off the key business i.e. the audit practice. They should consider if it would be better to spend their time trying

to compete effectively with the two new firms of accountants, trying to retain key clients, and to attract new accounting and

audit clients rather than diversify into something completely different.

1 Alvaro Pelorus is 47 years old and married to Maria. The couple have two children, Vito and Sophie, aged 22 and

19 years respectively. Alvaro and Maria have lived in the country of Koruba since 1982. On 1 July 2005 the family

moved to the UK to be near Alvaro’s father, Ray, who was very ill. Alvaro and Maria are UK resident, but not ordinarily

resident in the tax years 2005/06 and 2006/07. They are both domiciled in the country of Koruba.

On 1 February 2007 Ray Pelorus died. He was UK domiciled, having lived in the UK for the whole of his life. For the

purposes of inheritance tax, his death estate consisted of UK assets, valued at £870,000 after deduction of all

available reliefs, and a house in the country of Pacifica valued at £94,000. The executors of Ray’s estate have paid

Pacifican inheritance tax of £1,800 and legal fees of £7,700 in respect of the sale of the Pacifican house. Ray left

the whole of his estate to Alvaro.

Ray had made two gifts during his lifetime:

(i) 1 May 2003: He gave Alvaro 95 acres of farm land situated in the UK. The market value of the land was

£245,000, although its agricultural value was only £120,000. Ray had acquired the land on

1 January 1996 and granted an agricultural tenancy on that date. Alvaro continues to own the

land as at today’s date and it is still subject to the agricultural tenancy.

(ii) 1 August 2005: He gave Alvaro 6,000 shares valued at £183,000 in Pinger Ltd, a UK resident trading

company. Gift relief was claimed in respect of this gift. Ray had acquired 14,000 shares in

Pinger Ltd on 1 April 1997 for £54,600.

You may assume that Alvaro is a higher rate taxpayer for the tax years 2005/06 and 2006/07. In 2006/07 he made

the following disposals of assets:

(i) On 1 July 2006 he sold the 6,000 shares in Pinger Ltd for £228,000.

(ii) On 1 September 2006 he sold 2,350 shares in Lapis Inc, a company resident in Koruba, for £8,270. Alvaro

had purchased 5,500 shares in the company on 1 September 2002 for £25,950.

(iii) On 1 December 2006 he transferred shares with a market value of £74,000 in Quad plc, a UK quoted company,

to a UK resident discretionary trust for the benefit of Vito and Sophie. Alvaro had purchased these shares on

1 January 2006 for £59,500.

Alvaro has not made any other transfers of value for the purposes of UK inheritance tax. He owns the family house

in the UK as well as shares in UK and Koruban companies and commercial rental property in the country of Koruba.

Maria has not made any transfers of value for the purposes of UK inheritance tax. Her only significant asset is the

family home in the country of Koruba.

Alvaro and his family expect to return to their home in the country of Koruba in October 2007 once Ray’s affairs have

been settled. There is no double taxation agreement between the UK and Koruba.

Required:

(a) Calculate the inheritance tax (IHT) payable as a result of the death of Ray Pelorus. Explain the availability

or otherwise of agricultural property relief and business property relief on the two lifetime gifts made by Ray.

(8 marks)

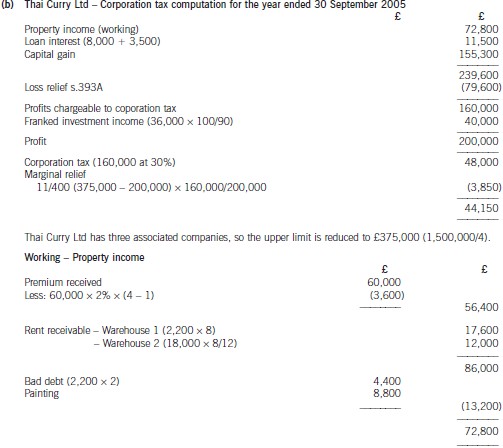

(b) Assuming that Thai Curry Ltd claims relief for its trading loss against total profits under s.393A ICTA 1988,calculate the company’s corporation tax liability for the year ended 30 September 2005. (10 marks)

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-01-10

- 2020-02-01

- 2020-01-10

- 2020-05-03

- 2020-05-07

- 2020-01-10

- 2020-01-10

- 2021-06-19

- 2020-01-10

- 2019-07-20

- 2020-03-13

- 2020-01-10

- 2019-07-20

- 2020-01-29

- 2020-01-09

- 2020-04-08

- 2020-01-10

- 2020-04-22

- 2020-04-16

- 2020-01-09

- 2021-09-13

- 2021-04-23

- 2019-01-04

- 2020-01-10

- 2020-04-10

- 2020-02-04

- 2020-05-16

- 2020-01-10

- 2020-03-07

- 2020-03-30