ACCA考试应考技巧

发布时间:2019-01-04

特许公认会计师公会(The

Association of Chartered Certified Accountants)简称ACCA,成立于1904年,是目前世界上领先的专业会计师团体,也是国际大家最多、大家规模发展最快的专业会计师组织。今天我们要看的就是ACCA考试答题技巧,希望对大家有所帮助。

1.ACCA的答卷在考试完成后全部寄回英国,由专家评改。尽管每题都有考官提供的标准答案,但判卷的专家不会拘泥于标准答案,如果学员能结合实际工作,其分析过程合理、充分,也会得分。

2.ACCA题目数量不大,但答题量大,占用时间长,ACCA考试时间为每门3个小时(笔试3小时15分钟答题时间),一般学员难以在这个时间段内答完全部题目,像会计报表的平衡,通常需1到1.5个小时完成。考生宜根据自己的情况,把控好时间,个别考生要注意取舍。

3.ACCA考试与中国大部分考试相比,差异很大。ACCA教材和考试都充分体现“注重理解,注重对知识的运用”这一原则,不仅测试学员对经济计算规则的掌握程度,而且更重视学员对经济数据内涵的理解和分析。所以考试范围主要涉及ACCA认为是重点的部分,历年题型也基本类似,很少对非常细节性的问题出填空,选择的题目,也很少出偏题。题型以主观题为主,只有第一部分课程考试才会有少量客观题。主观题又基本分成计算(40%)和分析(60%)两大部分,或者合二为一。

备考之路漫长艰辛,需要大家持之以恒,每天要进行复习,切忌三天打鱼两天晒网,51题库考试学习网会一直在您的身边,支持您,陪伴您。祝愿大家早日功成名就!!!

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(b) Comment (with relevant calculations) on the performance of the business of Quicklink Ltd and Celer

Transport during the year ended 31 May 2005 and, insofar as the information permits, its projected

performance for the year ending 31 May 2006. Your answer should specifically consider:

(i) Revenue generation per vehicle

(ii) Vehicle utilisation and delivery mix

(iii) Service quality. (14 marks)

difference will reduce in the year ending 31 May 2006 due to the projected growth in sales volumes of the Celer Transport

business. The average mail/parcels delivery of mail/parcels per vehicle of the Quicklink Ltd part of the business is budgeted

at 12,764 which is still 30·91% higher than that of the Celer Transport business.

As far as specialist activities are concerned, Quicklink Ltd is budgeted to generate average revenues per vehicle amounting to

£374,850 whilst Celer Transport is budgeted to earn an average of £122,727 from each of the vehicles engaged in delivery

of processed food. It is noticeable that all contracts with major food producers were renewed on 1 June 2005 and it would

appear that there were no increases in the annual value of the contracts with major food producers. This might have been

the result of a strategic decision by the management of the combined entity in order to secure the future of this part of the

business which had been built up previously by the management of Celer Transport.

Each vehicle owned by Quicklink Ltd and Celer Transport is in use for 340 days during each year, which based on a

365 day year would give an in use % of 93%. This appears acceptable given the need for routine maintenance and repairs

due to wear and tear.

During the year ended 31 May 2005 the number of on-time deliveries of mail and parcel and industrial machinery deliveries

were 99·5% and 100% respectively. This compares with ratios of 82% and 97% in respect of mail and parcel and processed

food deliveries made by Celer Transport. In this critical area it is worth noting that Quicklink Ltd achieved their higher on-time

delivery target of 99% in respect of each activity whereas Celer Transport were unable to do so. Moreover, it is worth noting

that Celer Transport missed their target time for delivery of food products on 975 occasions throughout the year 31 May 2005

and this might well cause a high level of customer dissatisfaction and even result in lost business.

It is interesting to note that whilst the businesses operate in the same industry they have a rather different delivery mix in

terms of same day/next day demands by clients. Same day deliveries only comprise 20% of the business of Quicklink Ltd

whereas they comprise 75% of the business of Celer Transport. This may explain why the delivery performance of Celer

Transport with regard to mail and parcel deliveries was not as good as that of Quicklink Ltd.

The fact that 120 items of mail and 25 parcels were lost by the Celer Transport business is most disturbing and could prove

damaging as the safe delivery of such items is the very substance of the business and would almost certainly have resulted

in a loss of customer goodwill. This is an issue which must be addressed as a matter of urgency.

The introduction of the call management system by Quicklink Ltd on 1 June 2004 is now proving its worth with 99% of calls

answered within the target time of 20 seconds. This compares favourably with the Celer Transport business in which only

90% of a much smaller volume of calls were answered within a longer target time of 30 seconds. Future performance in this

area will improve if the call management system is applied to the Celer Transport business. In particular, it is likely that the

number of abandoned calls will be reduced and enhance the ‘image’ of the Celer Transport business.

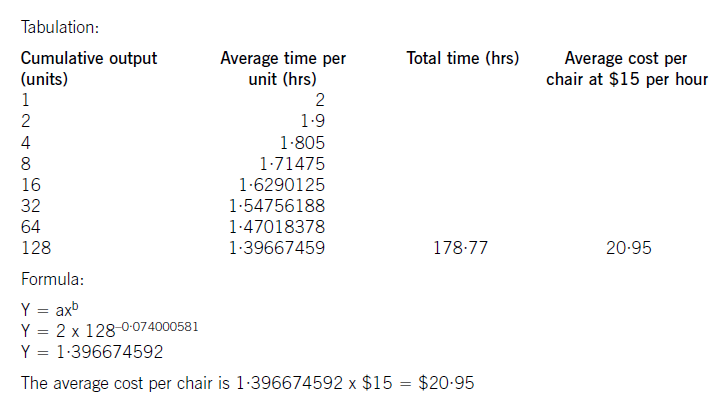

Big Cheese Chairs (BCC) manufactures and sells executive leather chairs. They are considering a new design of massaging chair to launch into the competitive market in which they operate.

They have carried out an investigation in the market and using a target costing system have targeted a competitive selling price of $120 for the chair. BCC wants a margin on selling price of 20% (ignoring any overheads).

The frame. and massage mechanism will be bought in for $51 per chair and BCC will upholster it in leather and assemble it ready for despatch.

Leather costs $10 per metre and two metres are needed for a complete chair although 20% of all leather is wasted in the upholstery process.

The upholstery and assembly process will be subject to a learning effect as the workers get used to the new design.

BCC estimates that the first chair will take two hours to prepare but this will be subject to a learning rate (LR) of 95%.

The learning improvement will stop once 128 chairs have been made and the time for the 128th chair will be the time for all subsequent chairs. The cost of labour is $15 per hour.

The learning formula is shown on the formula sheet and at the 95% learning rate the value of b is -0·074000581.

Required:

(a) Calculate the average cost for the first 128 chairs made and identify any cost gap that may be present at

that stage. (8 marks)

(b) Assuming that a cost gap for the chair exists suggest four ways in which it could be closed. (6 marks)

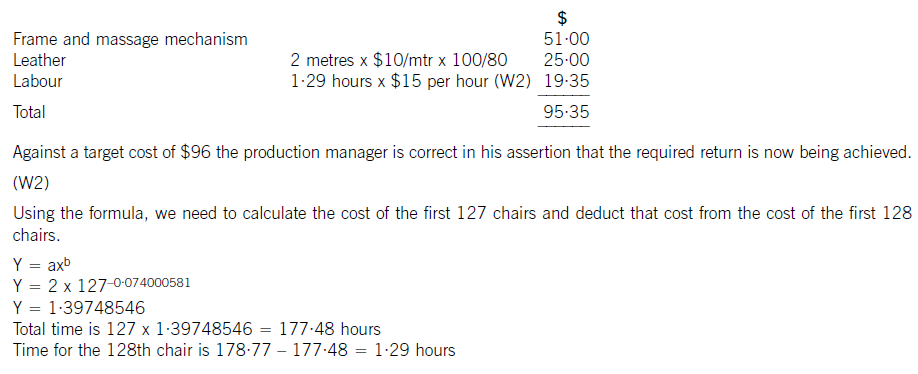

The production manager denies any claims that a cost gap exists and has stated that the cost of the 128th chair will be low enough to yield the required margin.

(c) Calculate the cost of the 128th chair made and state whether the target cost is being achieved on the 128th chair. (6 marks)

(W1)

The cost of the labour can be calculated using learning curve principles. The formula can be used or a tabular approach would

also give the average cost of 128 chairs. Both methods are acceptable and shown here.

(b) To reduce the cost gap various methods are possible (only four are needed for full marks)

– Re-design the chair to remove unnecessary features and hence cost

– Negotiate with the frame. supplier for a better cost. This may be easier as the volume of sales improve as suppliers often

are willing to give discounts for bulk buying. Alternatively a different frame. supplier could be found that offers a better

price. Care would be needed here to maintain the required quality

– Leather can be bought from different suppliers or at a better price also. Reducing the level of waste would save on cost.

Even a small reduction in waste rates would remove much of the cost gap that exists

– Improve the rate of learning by better training and supervision

– Employ cheaper labour by reducing the skill level expected. Care would also be needed here not to sacrifice quality or

push up waste rates.

(c) The cost of the 128th chair will be:

(d) Describe the three stages of a formal grievance interview that Oliver might seek with the appropriate partner

at Hoopers and Henderson following the formal procedure. (9 marks)

Part (d):

Oliver should arrange a formal grievance interview with the appropriate partner. Both Oliver and the partner need to be aware that

the grievance interview follows three steps in a particular and logical order. The meeting between Oliver and the partner responsible

for human resources must be in a formal atmosphere.

The first stage is exploration. The manager or supervisor – in this case the partner responsible for human resources – must gather

as much information as possible. No solution must be offered at this stage. The need is to establish what is actually the problem;

the background to the problem (in this case the icy relationship between Oliver and David Morgan) and the facts and causes of

the problem – in this case the resentment felt by David Morgan over Oliver’s appointment.

The second stage is the consideration stage. This is undertaken by the appropriate manager or partner here, who must firstly check

the facts, analyse the causes of the complaint and evaluate possible solutions. The meeting may be adjourned if at this stage the

partner requires more time to fulfil this step.

The final stage is the reply. This will be carried out by the partner after he or she has reached and reviewed a conclusion. It is

important that the outcome is recorded in writing; the meeting and therefore the interview and procedure is only successful when

an agreement is reached.

If no agreement is reached then the procedure should be taken to a higher level of management.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-03-21

- 2020-01-10

- 2020-01-10

- 2020-02-01

- 2020-01-09

- 2020-01-10

- 2020-05-14

- 2020-01-10

- 2020-02-06

- 2020-01-09

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-02-02

- 2020-01-10

- 2020-01-10

- 2021-06-25

- 2020-04-08

- 2020-03-14

- 2020-05-05

- 2020-04-16

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2019-07-20

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-01-10