2020年ACCA考试F6、P6科目特点及备考建议

发布时间:2020-02-29

ACCA考试科目较多,考生往往需要几年才能通过所有考试。而合理的考试科目搭配,可以让考试通过时间更快。鉴于此,51题库考试学习网在下面为大家带来2020年ACCA考试F2-F5-F9-P5科目备考的相关信息,以供参考。

如果小伙伴们准备学习P6,那么可以把F6放在F阶段最后一门,然后紧接着学习P6。由于F6P6的考试时间是同一天,所以你没法一次跨进两条河流,也没法两次跨进同一条河流。因此,小伙伴可以选择将这两科安排在同一个年度内,税率不变也不用重新记;当然了,科目类别要选择一致的,如果在F6选择了UK,那么 P6也就选择UK,但是由于在中国选择P6这门课程学习的人不多,所以学习资料与课程也很少,考生一定要根据自身要求谨慎选择。提前做好准备。

从内容上看,F6《税务》是P6《高级税务》的直接基础。F6课程涵盖:英国税法体制,个人所得税,公司所得税,应税所得,增值税,继承税,国民保险以及纳税人的义务。在学习F6时,考生能够学到:如何解释和计算与个人、公司相关的税收法律体系。同时,也是在为P6做准备。

ACCA考试必须按照四大课程的顺序进行,因此小伙伴们在报考时主要面对的是课程内的科目搭配顺序。而不同科目之间又往往存在递进关系,所以ACCA官方建议学员只需按照科目顺序从F1考到P7是非常合理的。同时,因为一年只能考8门,所以平均下来每次报2科目就非常简单合理了。不过,由于2020年第一考试季的ACCA考试已经取消(中国地区),因此准备好的小伙伴们也可以在剩下的考试季适当增加一科。

以上就是关于ACCA考试科目搭配的相关情况。51题库考试学习网提醒:ACCA考试科目较多,并且考试费用较高,小伙伴们在报考后应尽快安排学习计划,争取早日脱坑。最后,51题库考试学习网预祝准备参加2020年ACCA考试的小伙伴都能顺利通过。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(c) Calculate and explain the amount of income tax relief that Gerard will obtain in respect of the pension

contributions he proposes to make in the tax year 2007/08 and contrast this with how his position could be

improved by delaying some of the contributions that he could have made in 2007/08 until 2008/09. You

should include relevant supporting calculations and quantify the additional tax savings arising as a result of

your advice.

You should ignore the proposed changes to the bonus scheme for this part of this question and assume that

Gerard’s income will not change in 2008/09. (12 marks)

(b) Explain the matters you should consider before accepting an engagement to conduct a due diligence review

of MCM. (10 marks)

(b) Matters to be considered (before accepting the engagement)

Tutorial note: Although candidates may approach this part from a rote-learned list of ‘matters to consider’ it is important

that answer points be tailored, in so far as the information given in the scenario permits, to the specifics of Plaza and MCM.

It is critical that answer points should not contradict the scenario (e.g. assuming that it is Plaza’s auditor who has been

asked to undertake the assignment).

■ Information about Duncan Seymour – What is the relationship of the chief finance officer to Plaza (e.g. is he on the

management board)? By what authority is he approaching Andando to undertake this assignment?

■ The purpose of the assignment must be clarified. Duncan’s approach to Andando is ‘to advise on a bid’. However,

Andando cannot make executive decisions for a client but only provide the facts of material interest. Plaza’s

management must decide whether or not to bid and, if so, how much to bid.

■ The scope of the due diligence review. It seems likely that Plaza will be interested in acquiring all of MCM’s business

as its areas of operation coincide with Plaza’s. However it must be confirmed that Plaza is not merely interested in

acquiring only the National or International business of MCM.

■ Andando’s competence and experience – Andando should not accept the engagement unless the firm has experience in

undertaking due diligence assignments. Even then, the firm must have sufficient knowledge of the territories in which

the businesses operate to evaluate whether all facts of material interest to Plaza have been identified.

Tutorial note: Candidates should be querying their competence and experience in the fields of retailing and training

as though they were dealing with highly regulated or specialist industries such as banking or insurance.

■ Whether Andando has sufficient resources (e.g. representative/associated offices), if any, in Europe and Asia to

investigate MCM’s International business.

■ Any factors which might impair Andando’s objectivity in reporting to Plaza the facts uncovered by the due diligence

review. For example, if Duncan is closely connected with a partner in Andando or if Andando is the auditor of Frontiers.

Tutorial note: Candidates will not be awarded marks for going into ‘autopilot’ on independence issues. For example,

this is a one-off assignment so size of fee is not relevant. Andando holding shares in MCM is not possible (since whollyowned).

■ Plaza’s rationale for wishing to acquire MCM. Presumably it is significant that MCM operates in the same territories as

Plaza. Plaza may be wanting to provide extensive training programs in management, communications and marketing

to its workforce.

■ The relationship, if any, between Plaza and MCM in any of the territories. Plaza may be a major client of MCM. That

is, Plaza is currently out-sourcing training to MCM. Acquiring MCM would bring training in-house.

Tutorial note: Ascertaining what a purchaser hopes to gain from an acquisition before the assignment is accepted is

important. The facts to be uncovered for a merger from which synergy is expected will be different from those relevant

to acquiring an investment opportunity.

■ Time available – Andando must have sufficient time to find all facts that would be of material interest to Plaza before

disclosing their findings.

■ The acceptability of any limitations – whether there will be restrictions on Andando’s access to information held by MCM

(e.g. if there will not be access to board minutes) and personnel.

■ The degree of secrecy required – this may go beyond the normal duties of confidentiality not to disclose information to

outsiders (e.g. if unannounced staff redundancies could arise).

■ Why Plaza’s current auditors have not been asked to conduct the due diligence review – especially as they are

responsible for (and therefore capable of undertaking) the group audit covering the relevant countries.

■ Andando should be allowed to communicate with Plaza’s current auditor:

– to inform. them of the nature of the work they have been asked to undertake; and

– to enquire if there is any reason why they should not accept this assignment.

■ In taking on Plaza as a new client Andando may have a later opportunity to offer external audit and other services to

Plaza (e.g. internal audit).

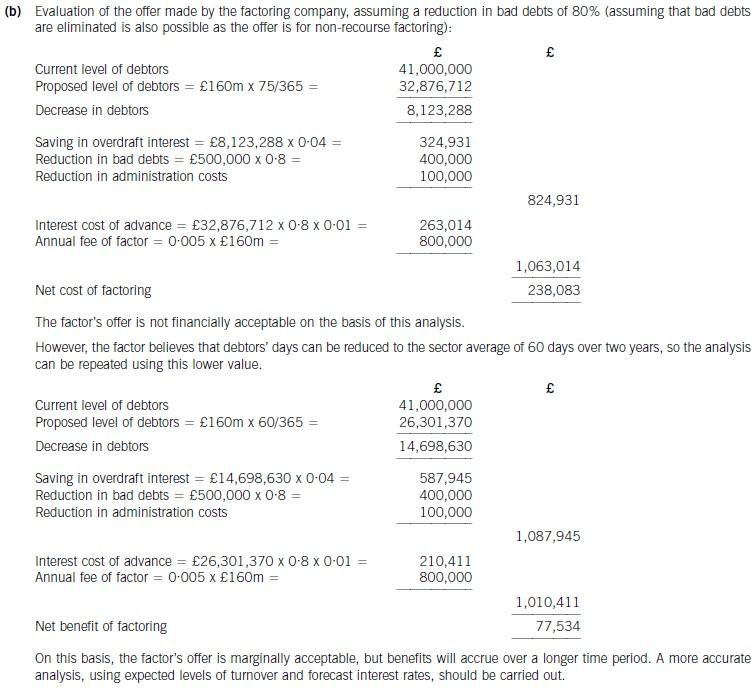

(b) Determine whether the factoring company’s offer can be recommended on financial grounds. Assume a

working year of 365 days and base your analysis on financial information for 2006. (8 marks)

(c) During the year Albreda paid $0·1 million (2004 – $0·3 million) in fines and penalties relating to breaches of

health and safety regulations. These amounts have not been separately disclosed but included in cost of sales.

(5 marks)

Required:

For each of the above issues:

(i) comment on the matters that you should consider; and

(ii) state the audit evidence that you should expect to find,

in undertaking your review of the audit working papers and financial statements of Albreda Co for the year ended

30 September 2005.

NOTE: The mark allocation is shown against each of the three issues.

(c) Fines and penalties

(i) Matters

■ $0·1 million represents 5·6% of profit before tax and is therefore material. However, profit has fallen, and

compared with prior year profit it is less than 5%. So ‘borderline’ material in quantitative terms.

■ Prior year amount was three times as much and represented 13·6% of profit before tax.

■ Even though the payments may be regarded as material ‘by nature’ separate disclosure may not be necessary if,

for example, there are no external shareholders.

■ Treatment (inclusion in cost of sales) should be consistent with prior year (‘The Framework’/IAS 1 ‘Presentation of

Financial Statements’).

■ The reason for the fall in expense. For example, whether due to an improvement in meeting health and safety

regulations and/or incomplete recording of liabilities (understatement).

■ The reason(s) for the breaches. For example, Albreda may have had difficulty implementing new guidelines in

response to stricter regulations.

■ Whether expenditure has been adjusted for in the income tax computation (as disallowed for tax purposes).

■ Management’s attitude to health and safety issues (e.g. if it regards breaches as an acceptable operational practice

or cheaper than compliance).

■ Any references to health and safety issues in other information in documents containing audited financial

statements that might conflict with Albreda incurring these costs.

■ Any cost savings resulting from breaches of health and safety regulations would result in Albreda possessing

proceeds of its own crime which may be a money laundering offence.

(ii) Audit evidence

■ A schedule of amounts paid totalling $0·1 million with larger amounts being agreed to the cash book/bank

statements.

■ Review/comparison of current year schedule against prior year for any apparent omissions.

■ Review of after-date cash book payments and correspondence with relevant health and safety regulators (e.g. local

authorities) for liabilities incurred before 30 September 2005.

■ Notes in the prior year financial statements confirming consistency, or otherwise, of the lack of separate disclosure.

■ A ‘signed off’ review of ‘other information’ (i.e. directors’ report, chairman’s statement, etc).

■ Written management representation that there are no fines/penalties other than those which have been reflected in

the financial statements.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-03-05

- 2020-01-10

- 2020-05-20

- 2020-03-11

- 2020-04-04

- 2020-01-29

- 2020-01-31

- 2020-01-10

- 2020-04-04

- 2021-05-22

- 2020-01-10

- 2020-01-03

- 2019-07-21

- 2020-03-11

- 2020-05-01

- 2020-01-10

- 2019-12-29

- 2020-01-08

- 2020-04-30

- 2020-04-03

- 2020-04-28

- 2020-03-21

- 2020-01-09

- 2020-01-03

- 2020-01-10

- 2020-08-01

- 2020-03-20

- 2020-01-09

- 2020-03-01

- 2020-01-10