贵州省2020年ACCA国际会计师报考指南

发布时间:2020-01-08

对于近些年才映入大众眼球的ACCA证书,想必大家也是处于一知半解的状态吧,那么ACCA国际注册会计师证到底有什么用?适用的报考的人群又是哪些呢?这些问题一直困扰着大部分准备报考ACCA的同学们,不用担心,51题库考试学习网在这为大家解答疑惑,这些报考指南宝典要收藏哟~

首先大家先看看最新的免试政策,看看你符合哪个条件,到底能免试几个科目:

1.哪些人适合报考ACCA?

在校大学生(金融、会计、管理专业的)

有意向从事财务、金融、管理领域相关职业,教育部认可的高等院校在读学生,建议从大一开始学习ACCA。但需要你完成了大一整个学年的学习才可以报考ACCA。

大专及以上学历者

有意向从事财务、金融、管理领域相关职业,希望提升自身的学历水平和专业技能,扩大自己的人脉圈,ACCA可助你学历跟职业竞争力双丰收。

财务专业人士

正在从事或准备从事财会工作的专业人士,适合财务经理、财务主管、财务分析、财务顾问、投资经理等岗位人员。这一部分的人学习ACCA相比较前两者有优势的地方在于目前从事的工作与ACCA考试基础阶段的知识要点或多或少有重叠部分

高级管理人员

需要提升国际化思维能力,综合运用财务与管理知识做出战略决策的企业中高层管理者,高级管理人员对自身要求将会更高,而ACCA考试正是一个全方面对自己能力的考核的考试。例如公司总裁、财务总监、董秘等。

2.ACCA的效力?

ACCA一般用来和CPA相比。各自又有各自的优势,虽然对于大部分企业(各种集团和四大)而言,二者可以互换(作为会计知识水平的证明)。但前者作为全英文考试,更受外企喜爱;后者在国内有签字权(财务报告或审计报告签字),因而国内内资会计师事务所略看重一些。

3.ACCA考试改革具体的变化有哪些?

ACCA对其专业资格最高阶段的考试进行了创新设计,已于2018年9月以全新的战略专业阶段(Strategic Professional)考试取代之前的专业阶段考试体系,更加注重就业能力与核心技能在现代工作场所中的实际应用。更加注重培养理论和实践都杰出的人才

全新的战略专业阶段包括:

●战略商业领袖 (Strategic Business Leader)——这是一门基于现实商业情境的创新案例考试,考试时长为4小时。

●战略商业报告(Strategic Business Reporting)——这门新型考试将使学员接触到更广泛的财务和商业报告情境,培养他们的重要技能,从而向利益相关方解释和传达商业交易与报告的意义和影响。

●职业道德与专业技能模块(Ethics and Professional Skills

module)——作为首家在2008年向学员开设职业道德模块的专业会计师组织,ACCA对当前的职业道德模块进行了重新构建。新模块已上线。

这一阶段的考试不仅仅是对考试理论层面的考核,还必须要结合实践,所以此类改革更加完备了ACCA考核的标准,让ACCA证书的含金量更上一层楼~

4.ACCA和学校学习之间的关系?

首先,由于ACCA是英文版的国际会计课程,所以在很多课程上会出现ACCA先讲过课内再讲,亦或者相反。总体而言,ACCA的课程比学校课程更加靠近时代,理论层次稍高。同时,ACCA对于四大的大一大二大三的项目、实习项目和企业的实习项目也有一定的帮助。但如果是在大学期间报考ACCA考试的话,一定要协调好ACCA考试和学校课程的关系,比较学校课程的成绩和绩点与自身的毕业证书有关。

总结,这些报考宝典你Get到了吗?最后,还是希望大家能明白,Pass,Fail本身并无好坏,成绩只是结果,关键是我们如何以平静的心态去面对考试,去面对考试结果。不论Pass or Fail,我们都要真确应对!最后,51题库考试学习网预祝大家在三月份的考试全部PASS!

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

5 (a) ‘In the case of an assurance engagement it is in the public interest and, therefore, required by this Code of Ethics,

that members of assurance teams … be independent of assurance clients’.

IFAC Code of Ethics for Professional Accountants

Required:

Define the term ‘assurance team’. (3 marks)

5 ETHICS COLUMN

(a) ‘Assurance team’

■ All members of the engagement team (for the assurance engagement);

■ All others within a firm who can directly influence the outcome of the assurance engagement, for example:

– those who recommend the compensation of, or who provide direct supervisory, management or other oversight of

the assurance engagement partner in connection with the performance of the assurance engagement;

– those who provide consultation regarding technical or industry specific issues, transactions or events for the

assurance engagement; and

– those who provide quality control for the assurance.

25 What should the minority interest figure be in the group’s consolidated balance sheet at 31 December 2005?

A $240,000

B $80,000

C $180,000

D $140,000

20% x (400,000 + 800,000)

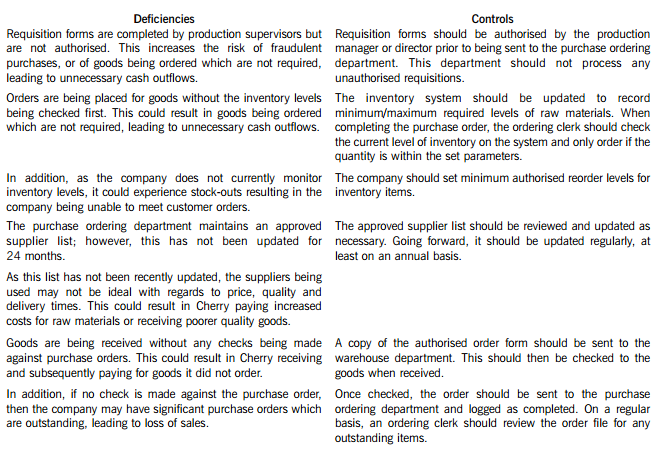

Cherry Blossom Co (Cherry) manufactures custom made furniture and its year end is 30 April. The company purchases its raw materials from a wide range of suppliers. Below is a description of Cherry’s purchasing system.

When production supervisors require raw materials, they complete a requisition form. and this is submitted to the purchase ordering department. Requisition forms do not require authorisation and no reference is made to the current inventory levels of the materials being requested. Staff in the purchase ordering department use the requisitions to raise sequentially numbered purchase orders based on the approved suppliers list, which was last updated 24 months ago. The purchasing director authorises the orders prior to these being sent to the suppliers.

When the goods are received, the warehouse department verifies the quantity to the suppliers despatch note and checks that the quality of the goods received are satisfactory. They complete a sequentially numbered goods received note (GRN) and send a copy of the GRN to the finance department.

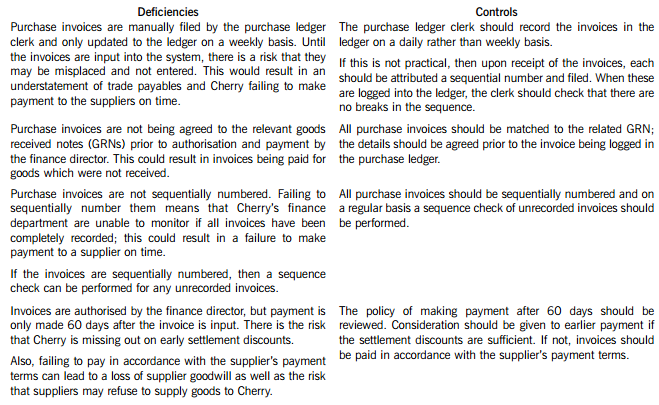

Purchase invoices are sent directly to the purchase ledger clerk, who stores them in a manual file until the end of each week. He then inputs them into the purchase ledger using batch controls and gives each invoice a unique number based on the supplier code. The invoices are reviewed and authorised for payment by the finance director, but the actual payment is only made 60 days after the invoice is input into the system.

Required:

In respect of the purchasing system of Cherry Blossom Co:

(i) Identify and explain FIVE deficiencies; and

(ii) Recommend a control to address each of these deficiencies.

Note: The total marks will be split equally between each part.

Cherry Blossom Co’s (Cherry) purchasing system deficiencies and controls

(b) Historically, all owned premises have been measured at cost depreciated over 10 to 50 years. The management

board has decided to revalue these premises for the year ended 30 September 2005. At the balance sheet date

two properties had been revalued by a total of $1·7 million. Another 15 properties have since been revalued by

$5·4 million and there remain a further three properties which are expected to be revalued during 2006. A

revaluation surplus of $7·1 million has been credited to equity. (7 marks)

Required:

For each of the above issues:

(i) comment on the matters that you should consider; and

(ii) state the audit evidence that you should expect to find,

in undertaking your review of the audit working papers and financial statements of Albreda Co for the year ended

30 September 2005.

NOTE: The mark allocation is shown against each of the three issues.

(b) Revaluation of owned premises

(i) Matters

■ The revaluations are clearly material as $1·7 million, $5·4 million and $7·1 million represent 5·5% , 17·6% and

23·1% of total assets, respectively.

■ The change in accounting policy, from a cost model to a revaluation model, should be accounted for in accordance

with IAS 16 ‘Property, Plant and Equipment’ (i.e. as a revaluation).

Tutorial note: IAS 8 ‘Accounting Policies, Changes in Accounting Estimates and Errors’ does not apply to the initial

application of a policy to revalue assets in accordance with IAS 16.

■ The basis on which the valuations have been carried out, for example, market-based fair value (IAS 16).

■ Independence, qualifications and expertise of valuer(s).

■ IAS 16 does not permit the selective revaluation of assets thus the whole class of premises should have been

revalued.

■ The valuations of properties after the year end are adjusting events (i.e. providing additional evidence of conditions

existing at the year end) per IAS 10 ‘Events After the Balance Sheet Date’.

Tutorial note: It is ‘now’ still less than three months after the year end so these valuations can reasonably be

expected to reflect year-end values.

■ If $5·4 million is a net amount of surpluses and deficits it should be grossed up so that the credit to equity reflects

the sum of the surpluses with any deficits being expensed through profit and loss (IAS 36 ‘Impairment of Assets’).

■ The revaluation exercise is incomplete. If the revaluations on the remaining three properties are expected to be

material and cannot be reasonably estimated for inclusion in the financial statements for the year ended

30 September 2005 perhaps the change in policy should be deferred for a year.

■ Depreciation for the year should have been calculated on cost as usual to establish carrying amount before

revaluation.

■ Any premises held under finance leases should be similarly revalued.

(ii) Audit evidence

■ A schedule of depreciated cost of owned premises extracted from the non-current asset register.

■ Calculation of difference between valuation and depreciated cost by property. Separate summation of surpluses

and deficits.

■ Copy of valuation certificate for each property.

■ Physical inspection of properties with largest surpluses (including the two valued before the year end) to confirm

condition.

■ Extracts from local property guides/magazines indicating a range of values of similarly styled/sized properties.

■ Separate presentation of the revaluation surpluses (gross) in:

– the statement of changes in equity; and

– reconciliation of carrying amount at the beginning and end of the period.

■ IAS 16 disclosures in the notes to the financial statements including:

– the effective date of revaluation;

– whether an independent valuer was involved;

– the methods and significant assumptions applied in estimating fair values; and

– the carrying amount that would have been recognised under the cost model.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2019-07-21

- 2020-03-05

- 2020-03-04

- 2020-08-01

- 2019-12-27

- 2020-01-10

- 2020-03-12

- 2020-03-19

- 2020-03-22

- 2020-05-20

- 2020-04-15

- 2020-01-31

- 2020-04-18

- 2020-01-09

- 2020-01-10

- 2020-01-10

- 2020-04-21

- 2020-01-10

- 2020-04-07

- 2020-03-11

- 2020-01-10

- 2020-05-21

- 2020-01-10

- 2020-01-09

- 2020-04-03

- 2020-02-19

- 2020-01-09

- 2021-09-12

- 2020-03-08

- 2020-04-18