ACCA考试如何搭配科目?从简到难or从难到简考?

发布时间:2020-02-28

ACCA考试科目较多,如何合理搭配科目就成为了许多小伙伴们关心的问题。为了顺利通过考试,一些考生在新年到来之后就在网上查询ACCA考试如何搭配科目。鉴于此,51题库考试学习网在下面为大家带来2020年ACCA考试科目搭配的相关信息,以供参考。

ACCA考试必须按照四大课程的顺序进行,因此小伙伴们主要关注的是课程内的科目搭配顺序。事实上。ACCA官方建议学员只需按照科目顺序从F1考到P7是非常合理的。同时,因为一年只能考8门,所以平均下来每次报2科目就非常简单合理了。不过,由于2020年第一考试季的ACCA考试已经取消(中国地区),因此准备好的小伙伴们也可以在剩下的考试季适当增加一科。

以上就是关于ACCA考试科目搭配的相关情况。51题库考试学习网提醒:ACCA考试科目较多,小伙伴们在备考时间不充足的情况下,可以适当减少每年报考的总科目数,提高过关率。最后,51题库考试学习网预祝准备参加2020年ACCA考试的小伙伴都能顺利通过。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(c) the deferred tax implications (with suitable calculations) for the company which arise from the recognition

of a remuneration expense for the directors’ share options. (7 marks)

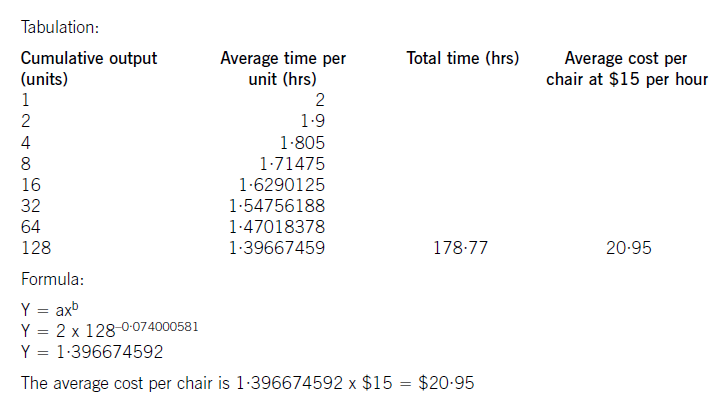

Big Cheese Chairs (BCC) manufactures and sells executive leather chairs. They are considering a new design of massaging chair to launch into the competitive market in which they operate.

They have carried out an investigation in the market and using a target costing system have targeted a competitive selling price of $120 for the chair. BCC wants a margin on selling price of 20% (ignoring any overheads).

The frame. and massage mechanism will be bought in for $51 per chair and BCC will upholster it in leather and assemble it ready for despatch.

Leather costs $10 per metre and two metres are needed for a complete chair although 20% of all leather is wasted in the upholstery process.

The upholstery and assembly process will be subject to a learning effect as the workers get used to the new design.

BCC estimates that the first chair will take two hours to prepare but this will be subject to a learning rate (LR) of 95%.

The learning improvement will stop once 128 chairs have been made and the time for the 128th chair will be the time for all subsequent chairs. The cost of labour is $15 per hour.

The learning formula is shown on the formula sheet and at the 95% learning rate the value of b is -0·074000581.

Required:

(a) Calculate the average cost for the first 128 chairs made and identify any cost gap that may be present at

that stage. (8 marks)

(b) Assuming that a cost gap for the chair exists suggest four ways in which it could be closed. (6 marks)

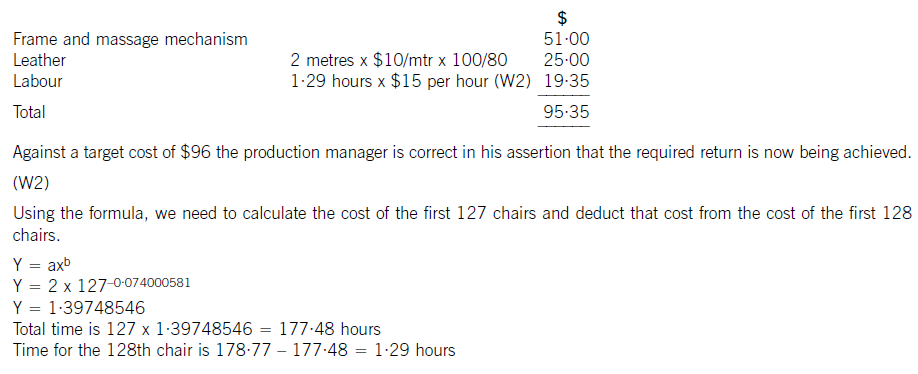

The production manager denies any claims that a cost gap exists and has stated that the cost of the 128th chair will be low enough to yield the required margin.

(c) Calculate the cost of the 128th chair made and state whether the target cost is being achieved on the 128th chair. (6 marks)

(W1)

The cost of the labour can be calculated using learning curve principles. The formula can be used or a tabular approach would

also give the average cost of 128 chairs. Both methods are acceptable and shown here.

(b) To reduce the cost gap various methods are possible (only four are needed for full marks)

– Re-design the chair to remove unnecessary features and hence cost

– Negotiate with the frame. supplier for a better cost. This may be easier as the volume of sales improve as suppliers often

are willing to give discounts for bulk buying. Alternatively a different frame. supplier could be found that offers a better

price. Care would be needed here to maintain the required quality

– Leather can be bought from different suppliers or at a better price also. Reducing the level of waste would save on cost.

Even a small reduction in waste rates would remove much of the cost gap that exists

– Improve the rate of learning by better training and supervision

– Employ cheaper labour by reducing the skill level expected. Care would also be needed here not to sacrifice quality or

push up waste rates.

(c) The cost of the 128th chair will be:

(iii) State the value added tax (VAT) and stamp duty (SD) issues arising as a result of inserting Bold plc as

a holding company and identify any planning actions that can be taken to defer or minimise these tax

costs. (4 marks)

You should assume that the corporation tax rates for the financial year 2005 and the income tax rates

and allowances for the tax year 2005/06 apply throughout this question.

(iii) Bold plc will be making a taxable supply of services, likely to exceed the VAT threshold. It should therefore consider

registering for VAT – either immediately on a voluntary basis, or when its cumulative taxable supplies in the previous

twelve months exceed £60,000.

As an alternative, the new group can apply for a group VAT registration. This will simplify its VAT administration as intragroup

transactions are broadly disregarded for VAT purposes, and only one VAT return is required for the group as a

whole.

Stamp duty normally applies at 0·5% on the consideration payable in respect of transactions in shares. However, an

exemption is available in the case of a takeover, reconstruction or amalgamation where there is no real change in

ownership, i.e. the new shareholdings mirror the old shareholdings, and the transaction is for commercial purposes. The

insertion of a new holding company over an existing company, as proposed here, would qualify for this exemption.

There is no VAT on transactions in shares.

(ii) Explain the organisational factors that determine the need for internal audit in public listed companies.

(5 marks)

(ii) Factors affecting the need for internal audit and controls

(Based partly on Turnbull guidance)

The nature of operations within the organisation arising from its sector, strategic positioning and main activities.

The scale and size of operations including factors such as the number of employees. It is generally assumed that larger

and more complex organisations have a greater need for internal controls and audit than smaller ones owing to the

number of activities occurring that give rise to potential problems.

Cost/benefit considerations. Management must weigh the benefits of instituting internal control and audit systems

against the costs of doing so. This is likely to be an issue for medium-sized companies or companies experiencing

growth.

Internal or external changes affecting activities, structures or risks. Changes arising from new products or internal

activities can change the need for internal audit and so can external changes such as PESTEL factors.

Problems with existing systems, products and/or procedures including any increase in unexplained events. Repeated or

persistent problems can signify the need for internal control and audit.

The need to comply with external requirements from relevant stock market regulations or laws. This appears to be a

relevant factor at Gluck & Goodman.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-05-20

- 2020-04-18

- 2020-01-09

- 2020-02-29

- 2021-09-12

- 2020-02-28

- 2020-01-09

- 2020-02-14

- 2020-03-12

- 2020-03-11

- 2019-07-21

- 2020-01-10

- 2020-01-09

- 2020-01-09

- 2020-03-13

- 2020-03-05

- 2019-05-28

- 2020-03-08

- 2020-04-29

- 2020-03-08

- 2020-01-10

- 2019-01-09

- 2020-01-09

- 2020-01-11

- 2021-09-12

- 2020-04-21

- 2020-02-29

- 2020-01-10

- 2020-01-08

- 2020-04-27