湖北省考生:2020年ACCA国际会计师考试时间是如何安排的?

发布时间:2020-01-10

众所周知,想要获得ACCA证书代价是十分巨大的,不仅仅要花费昂贵的报名费用,而且因为考试科目多的原因还需要大把大把的时间和精力去学习和理解知识点。尤其是对在职人员来说,更是一大挑战者,因此许多考生都因此望尘莫及,目前,ACCA国际会计师注册考试的报名时间和考试时间都依次发布了,51题库考试学习网替大家收集到了今年全部的考试报名时间信息和考试时间信息,希望对大家在了解到考试时间之后,能够合理地科学地备考考试。

首先是2020年ACCA考试报名时间:(建议收藏哦~)

了解完报名时间后,大家可以根据自己的学习能力和时间因素等情况依次可以开始备考了哟(学习能力强的考生可以优先从真题开始做起)

接下来,在认真复习、科学备考的同时,千万不要忘记了考试时间,所以这份是2020年ACCA考试时间表建议大家保存在相册里:

险夷原不滞胸中,何异浮云过太空!以上消息希望对正在准备备战3月份的ACCAer们有所帮助,51题库考试学习网预祝大家考试成功!

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(b) What styles of managing change would you recommend John use to bring about the desired change?

(8 marks)

(b) Choosing the right combination of styles to manage the desired change will be an interesting challenge to John as the principal

change agent. Education and communication will be vital in getting the police officers to buy in to the need for change. It is

only by changing their perception of the nature and size of the city centre problem that any change in activity will be possible.

Communication will also be important to keep the other stakeholders informed and on board – in this case the mayor is likely

to be a key player.

Having convinced the police officers of the need for and achievability of the change John has then to motivate them to become

involved. This is achieved through collaboration and participation. John will determine the extent to which officers or task

groups are involved in various parts in the change process. Here the emphasis is on getting a shared ownership of the problem

and getting better solutions to parts of the problem. As with education and communication this may be a time-consuming

process.

Intervention by John may be needed at various points in the change process; he may delegate certain activities to others but

retain the coordination and control of the project. On occasions it may be necessary for John to take direct control over the

process in order to clarify and speed-up the whole process but such direction may cause a lack of acceptance and a poorly

conceived strategy. Finally, in times of crisis resort may have to be made to coercion/edict. This is likely to be the leastsuccessful means of managing change and should only be used when exceptional circumstances are present.

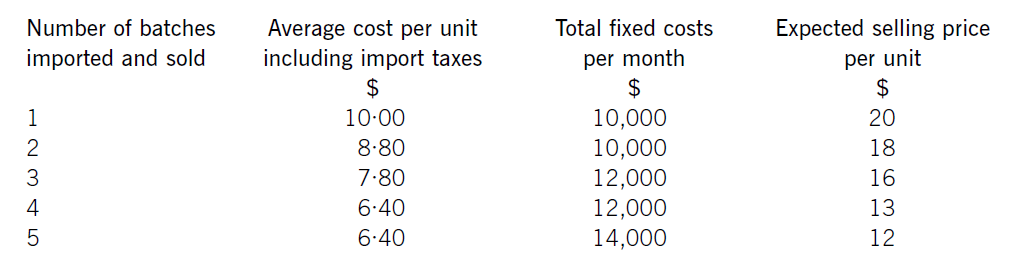

Jewel Co is setting up an online business importing and selling jewellery headphones. The cost of each set of headphones varies depending on the number purchased, although they can only be purchased in batches of 1,000 units. It also has to pay import taxes which vary according to the quantity purchased.

Jewel Co has already carried out some market research and identified that sales quantities are expected to vary depending on the price charged. Consequently, the following data has been established for the first month:

Required:

(a) Calculate how many batches Jewel Co should import and sell. (6 marks)

(b) Explain why Jewel Co could not use the algebraic method to establish the optimum price for its product.

(4 marks)

(b)Thealgebraicmodelrequiresseveralassumptionstobetrue.First,theremustbeaconsistentrelationshipbetweenprice(P)anddemand(Q),sothatademandequationcanbeestablished,usuallyintheform.P=a–bQ.Here,althoughthereisaclearrelationshipbetweenthetwo,itisnotaperfectlylinearrelationshipandsomorecomplicatedtechniquesarerequiredtocalculatethedemandequation.ItalsocannotbeassumedthatalinearrelationshipwillholdforallvaluesofPandQotherthanthefivegiven.Similarly,theremustbeaclearrelationshipbetweendemandandmarginalcost,usuallysatisfiedbyconstantvariablecostperunitandconstantfixedcosts.Thechangingvariablecostsperunitagaincomplicatetheissue,butitisthechangesinfixedcostswhichmakethealgebraicmethodlessusefulinJewel’scase.Thealgebraicmodelisonlysuitableforcompaniesoperatinginamonopolyanditisnotclearherewhetherthisisthecase,butitseemsunlikely,soany‘optimum’pricemightbecomeirrelevantifJewel’scompetitorschargesignificantlylowerprices.Othermoregeneralfactorsnotconsideredbythealgebraicmodelarepoliticalfactorswhichmightaffectimports,socialfactorswhichmayaffectcustomertastesandeconomicfactorswhichmayaffectexchangeratesorcustomerspendingpower.Thereliabilityoftheestimatesthemselves–forsalesprices,variablecostsandfixedcosts–couldalsobecalledintoquestion.

(d) Wader has decided to close one of its overseas branches. A board meeting was held on 30 April 2007 when a

detailed formal plan was presented to the board. The plan was formalised and accepted at that meeting. Letters

were sent out to customers, suppliers and workers on 15 May 2007 and meetings were held prior to the year

end to determine the issues involved in the closure. The plan is to be implemented in June 2007. The company

wish to provide $8 million for the restructuring but are unsure as to whether this is permissible. Additionally there

was an issue raised at one of the meetings. The operations of the branch are to be moved to another country

from June 2007 but the operating lease on the present buildings of the branch is non-cancellable and runs for

another two years, until 31 May 2009. The annual rent of the buildings is $150,000 payable in arrears on

31 May and the lessor has offered to take a single payment of $270,000 on 31 May 2008 to settle the

outstanding amount owing and terminate the lease on that date. Wader has additionally obtained permission to

sublet the building at a rental of $100,000 per year, payable in advance on 1 June. The company needs advice

on how to treat the above under IAS37 ‘Provisions, Contingent Liabilities and Contingent Assets’. (7 marks)

Required:

Discuss the accounting treatments of the above items in the financial statements for the year ended 31 May

2007.

Note: a discount rate of 5% should be used where necessary. Candidates should show suitable calculations where

necessary.

(d) A provision under IAS37 ‘Provisions, Contingent Liabilities and Contingent assets’ can only be made in relation to the entity’s

restructuring plans where there is both a detailed formal plan in place and the plans have been announced to those affected.

The plan should identify areas of the business affected, the impact on employees and the likely cost of the restructuring and

the timescale for implementation. There should be a short timescale between communicating the plan and starting to

implement it. A provision should not be recognised until a plan is formalised.

A decision to restructure before the balance sheet date is not sufficient in itself for a provision to be recognised. A formal plan

should be announced prior to the balance sheet date. A constructive obligation should have arisen. It arises where there has

been a detailed formal plan and this has raised a valid expectation in the minds of those affected. The provision should only

include direct expenditure arising from the restructuring. Such amounts do not include costs associated with ongoing business

operations. Costs of retraining staff or relocating continuing staff or marketing or investment in new systems and distribution

networks, are excluded. It seems as though in this case a constructive obligation has arisen as there have been detailed formal

plans approved and communicated thus raising valid expectations. The provision can be allowed subject to the exclusion of

the costs outlined above.

Although executory contracts are outside IAS37, it is permissible to recognise a provision that is onerous. Onerous contracts

can result from restructuring plans or on a stand alone basis. A provision should be made for the best estimate of the excess

unavoidable costs under the onerous contract. This estimate should assess any likely level of future income from new sources.

Thus in this case, the rental income from sub-letting the building should be taken into account. The provision should be

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-04-04

- 2020-03-19

- 2020-01-09

- 2020-04-08

- 2020-04-18

- 2020-01-09

- 2021-06-25

- 2020-01-08

- 2020-01-10

- 2020-03-05

- 2020-03-25

- 2021-08-29

- 2020-02-28

- 2020-01-10

- 2020-01-09

- 2020-01-10

- 2020-01-08

- 2020-01-09

- 2020-03-12

- 2020-01-10

- 2020-01-08

- 2020-03-04

- 2020-01-08

- 2020-01-09

- 2020-01-08

- 2020-02-28

- 2020-04-19

- 2020-03-05

- 2020-03-11

- 2020-03-05