如果江西省考生符合这些条件,那么ACCA证书就是为你量身订做的

发布时间:2020-01-09

听闻ACCA证书含金量高你就随大众就去报考?听闻ACCA考试难度很大然后你就放弃考试?这样的想法可是不对的,做什么事一旦决定了就要坚持下去,坚持不懈虽然不一定成功,但一定会不留遗憾的。虽然关于ACCA考试并不适合大家全部人都去报考,但下面这几类人去51题库考试学习网十分建议去报考的

1、高中及大专学历者

在职场上,因为学历的原因吃了不少的亏的人,建议可以去报考ACCA考试,因为随着财务金融领域对这方面要求的综合素质又比较高,那么通过ACCA来提高自己的学历以及职业竞争力,是一箭双雕的选择。

2、学校不好想要逆袭

那些不是985或者211院校的普通院校毕业的同学,其实学习ACCA,不仅能提高英语成绩,提高眼界和知识面,还能提高你的自信和思维能力,在面对名校人才竞争时,你未必争不过。

3、英国留学生、会计硕士

ACCA是英国的财会考试,如果你正好在英国留学,并且就读于会计相关专业,那你的优势可就大了,因为ACCA官方总部是在英国的,完全可以利用教材、地点之便参加ACCA考试。作为本土考试,在英国大学里学习相关知识,可以让你更快掌握英式的答题思路和逻辑思维,考起试来事半功倍。

4、想让大学生活更充实的大学生

大学是很多人人生最后能够专心学习的求学阶段,也是我们踏入社会、告别读书的过渡时期,大学不会再像高中那样几乎所有的时间都被占据,而是拥有很多个人闲暇时光。因此你可以利用自己的闲暇时间来学习和复习关于ACCA的内容,毕竟多考一个证书多一个选择嘛。如果你不好好利用,大学四年也会匆匆而过。如果不甘心大学就此平庸,希望能够更加充实,学习到更多的知识,掌握更多的技能,那么,学习ACCA是个很不错的选择。你会发现,学了之后,ACCA带给你的收获远超你的想象。

5、想毕业后找到好工作的人

大学毕业后有很多不同的选择,有人考研、有人出国、有人直接工作。但对于选择直接工作的同学来说,必须想方设法提高自己的职场竞争力。考一个ACCA证书又不尝是个正确的选择呢?毕业生每年都在增长,毕业就失业并不是危言耸听。

6、外企工作者

虽然汉语是使用人数最多的语言,但英语毕竟是国际商务领域中普遍应用的语言,外企总是首先希望招聘到有较高英语写作与会话能力的人才。ACCA的考试里面独一无二的全英文考试也印证了对外企人才招募的对标程度。能成功通过ACCA考试的人英语一定不是太差,这对于应聘外企是一份巨大的优势。

以上信息希望对你报考ACCA考试有所参考,没有提及的一部分类型的人并不是证明不适合报考,只是提倡大家踊跃尝试,完善自身的同时也为这个社会提供了自己的一份力量。当然,是否报考ACCA考试最重要的的因素还是自身,适合自己的才是最好的。所以,各位ACCAer们,加油!预祝大家2020年3月份的考试成功通过~

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

21 Which of the following items must be disclosed in a company’s published financial statements?

1 Authorised share capital

2 Movements in reserves

3 Finance costs

4 Movements in non-current assets

A 1, 2 and 3 only

B 1, 2 and 4 only

C 2, 3 and 4 only

D All four items

Moonstar Co is a property development company which is planning to undertake a $200 million commercial property development. Moonstar Co has had some difficulties over the last few years, with some developments not generating the expected returns and the company has at times struggled to pay its finance costs. As a result Moonstar Co’s credit rating has been lowered, affecting the terms it can obtain for bank finance. Although Moonstar Co is listed on its local stock exchange, 75% of the share capital is held by members of the family who founded the company. The family members who are shareholders do not wish to subscribe for a rights issue and are unwilling to dilute their control over the company by authorising a new issue of equity shares. Moonstar Co’s board is therefore considering other methods of financing the development, which the directors believe will generate higher returns than other recent investments, as the country where Moonstar Co is based appears to be emerging from recession.

Securitisation proposals

One of the non-executive directors of Moonstar Co has proposed that it should raise funds by means of a securitisation process, transferring the rights to the rental income from the commercial property development to a special purpose vehicle. Her proposals assume that the leases will generate an income of 11% per annum to Moonstar Co over a ten-year period. She proposes that Moonstar Co should use 90% of the value of the investment for a collateralised loan obligation which should be structured as follows:

– 60% of the collateral value to support a tranche of A-rated floating rate loan notes offering investors LIBOR plus 150 basis points

– 15% of the collateral value to support a tranche of B-rated fixed rate loan notes offering investors 12%

– 15% of the collateral value to support a tranche of C-rated fixed rate loan notes offering investors 13%

– 10% of the collateral value to support a tranche as subordinated certificates, with the return being the excess of receipts over payments from the securitisation process

The non-executive director believes that there will be sufficient demand for all tranches of the loan notes from investors. Investors will expect that the income stream from the development to be low risk, as they will expect the property market to improve with the recession coming to an end and enough potential lessees to be attracted by the new development.

The non-executive director predicts that there would be annual costs of $200,000 in administering the loan. She acknowledges that there would be interest rate risks associated with the proposal, and proposes a fixed for variable interest rate swap on the A-rated floating rate notes, exchanging LIBOR for 9·5%.

However the finance director believes that the prediction of the income from the development that the non-executive director has made is over-optimistic. He believes that it is most likely that the total value of the rental income will be 5% lower than the non-executive director has forecast. He believes that there is some risk that the returns could be so low as to jeopardise the income for the C-rated fixed rate loan note holders.

Islamic finance

Moonstar Co’s chief executive has wondered whether Sukuk finance would be a better way of funding the development than the securitisation.

Moonstar Co’s chairman has pointed out that a major bank in the country where Moonstar Co is located has begun to offer a range of Islamic financial products. The chairman has suggested that a Mudaraba contract would be the most appropriate method of providing the funds required for the investment.

Required:

(a) Calculate the amounts in $ which each of the tranches can expect to receive from the securitisation arrangement proposed by the non-executive director and discuss how the variability in rental income affects the returns from the securitisation. (11 marks)

(b) Discuss the benefits and risks for Moonstar Co associated with the securitisation arrangement that the non-executive director has proposed. (6 marks)

(c) (i) Discuss the suitability of Sukuk finance to fund the investment, including an assessment of its appeal to potential investors. (4 marks)

(ii) Discuss whether a Mudaraba contract would be an appropriate method of financing the investment and discuss why the bank may have concerns about providing finance by this method. (4 marks)

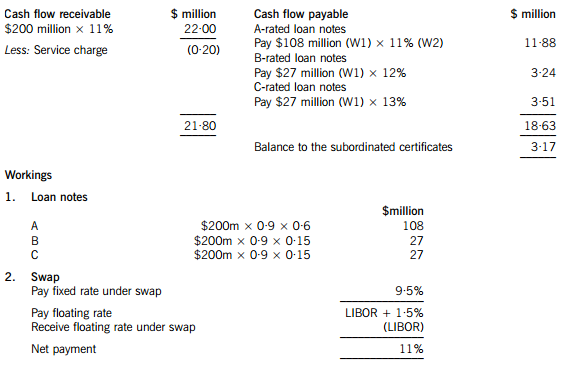

(a) An annual cash flow account compares the estimated cash flows receivable from the property against the liabilities within the securitisation process. The swap introduces leverage into the arrangement.

The holders of the certificates are expected to receive $3·17million on $18 million, giving them a return of 17·6%. If the cash flows are 5% lower than the non-executive director has predicted, annual revenue received will fall to $20·90 million, reducing the balance available for the subordinated certificates to $2·07 million, giving a return of 11·5% on the subordinated certificates, which is below the returns offered on the B and C-rated loan notes. The point at which the holders of the certificates will receive nothing and below which the holders of the C-rated loan notes will not receive their full income will be an annual income of $18·83 million (a return of 9·4%), which is 14·4% less than the income that the non-executive director has forecast.

(b) Benefits

The finance costs of the securitisation may be lower than the finance costs of ordinary loan capital. The cash flows from the commercial property development may be regarded as lower risk than Moonstar Co’s other revenue streams. This will impact upon the rates that Moonstar Co is able to offer borrowers.

The securitisation matches the assets of the future cash flows to the liabilities to loan note holders. The non-executive director is assuming a steady stream of lease income over the next 10 years, with the development probably being close to being fully occupied over that period.

The securitisation means that Moonstar Co is no longer concerned with the risk that the level of earnings from the properties will be insufficient to pay the finance costs. Risks have effectively been transferred to the loan note holders.

Risks

Not all of the tranches may appeal to investors. The risk-return relationship on the subordinated certificates does not look very appealing, with the return quite likely to be below what is received on the C-rated loan notes. Even the C-rated loan note holders may question the relationship between the risk and return if there is continued uncertainty in the property sector.

If Moonstar Co seeks funding from other sources for other developments, transferring out a lower risk income stream means that the residual risks associated with the rest of Moonstar Co’s portfolio will be higher. This may affect the availability and terms of other borrowing.

It appears that the size of the securitisation should be large enough for the costs to be bearable. However Moonstar Co may face unforeseen costs, possibly unexpected management or legal expenses.

(c) (i) Sukuk finance could be appropriate for the securitisation of the leasing portfolio. An asset-backed Sukuk would be the same kind of arrangement as the securitisation, where assets are transferred to a special purpose vehicle and the returns and repayments are directly financed by the income from the assets. The Sukuk holders would bear the risks and returns of the relationship.

The other type of Sukuk would be more like a sale and leaseback of the development. Here the Sukuk holders would be guaranteed a rental, so it would seem less appropriate for Moonstar Co if there is significant uncertainty about the returns from the development.

The main issue with the asset-backed Sukuk finance is whether it would be as appealing as certainly the A-tranche of the securitisation arrangement which the non-executive director has proposed. The safer income that the securitisation offers A-tranche investors may be more appealing to investors than a marginally better return from the Sukuk. There will also be costs involved in establishing and gaining approval for the Sukuk, although these costs may be less than for the securitisation arrangement described above.

(ii) A Mudaraba contract would involve the bank providing capital for Moonstar Co to invest in the development. Moonstar Co would manage the investment which the capital funded. Profits from the investment would be shared with the bank, but losses would be solely borne by the bank. A Mudaraba contract is essentially an equity partnership, so Moonstar Co might not face the threat to its credit rating which it would if it obtained ordinary loan finance for the development. A Mudaraba contract would also represent a diversification of sources of finance. It would not require the commitment to pay interest that loan finance would involve.

Moonstar Co would maintain control over the running of the project. A Mudaraba contract would offer a method of obtaining equity funding without the dilution of control which an issue of shares to external shareholders would bring. This is likely to make it appealing to Moonstar Co’s directors, given their desire to maintain a dominant influence over the business.

The bank would be concerned about the uncertainties regarding the rental income from the development. Although the lack of involvement by the bank might appeal to Moonstar Co's directors, the bank might not find it so attractive. The bank might be concerned about information asymmetry – that Moonstar Co’s management might be reluctant to supply the bank with the information it needs to judge how well its investment is performing.

(b) While the refrigeration units were undergoing modernisation Lamont outsourced all its cold storage requirements

to Hogg Warehousing Services. At 31 March 2007 it was not possible to physically inspect Lamont’s inventory

held by Hogg due to health and safety requirements preventing unauthorised access to cold storage areas.

Lamont’s management has provided written representation that inventory held at 31 March 2007 was

$10·1 million (2006 – $6·7 million). This amount has been agreed to a costing of Hogg’s monthly return of

quantities held at 31 March 2007. (7 marks)

Required:

For each of the above issues:

(i) comment on the matters that you should consider; and

(ii) state the audit evidence that you should expect to find,

in undertaking your review of the audit working papers and financial statements of Lamont Co for the year ended

31 March 2007.

NOTE: The mark allocation is shown against each of the three issues.

(b) Outsourced cold storage

(i) Matters

■ Inventory at 31 March 2007 represents 21% of total assets (10·1/48·0) and is therefore a very material item in the

balance sheet.

■ The value of inventory has increased by 50% though revenue has increased by only 7·5%. Inventory may be

overvalued if no allowance has been made for slow-moving/perished items in accordance with IAS 2 Inventories.

■ Inventory turnover has fallen to 6·6 times per annum (2006 – 9·3 times). This may indicate a build up of

unsaleable items.

Tutorial note: In the absence of cost of sales information, this is calculated on revenue. It may also be expressed

as the number of days sales in inventory, having increased from 39 to 55 days.

■ Inability to inspect inventory may amount to a limitation in scope if the auditor cannot obtain sufficient audit

evidence regarding quantity and its condition. This would result in an ‘except for’ opinion.

■ Although Hogg’s monthly return provides third party documentary evidence concerning the quantity of inventory it

does not provide sufficient evidence with regard to its valuation. Inventory will need to be written down if, for

example, it was contaminated by the leakage (before being moved to Hogg’s cold storage) or defrosted during

transfer.

■ Lamont’s written representation does not provide sufficient evidence regarding the valuation of inventory as

presumably Lamont’s management did not have access to physically inspect it either. If this is the case this may

call into question the value of any other representations made by management.

■ Whether, since the balance sheet date, inventory has been moved back from Hogg’s cold storage to Lamont’s

refrigeration units. If so, a physical inspection and roll-back of the most significant fish lines should have been

undertaken.

Tutorial note: Credit will be awarded for other relevant accounting issues. For example a candidate may question

whether, for example, cold storage costs have been capitalised into the cost of inventory. Or whether inventory moves

on a FIFO basis in deep storage (rather than LIFO).

(ii) Audit evidence

■ A copy of the health and safety regulation preventing the auditor from gaining access to Hogg’s cold storage to

inspect Lamont’s inventory.

■ Analysis of Hogg’s monthly returns and agreement of significant movements to purchase/sales invoices.

■ Analytical procedures such as month-on-month comparison of gross profit percentage and inventory turnover to

identify any trend that may account for the increase in inventory valuation (e.g. if Lamont has purchased

replacement inventory but spoiled items have not been written off).

■ Physical inspection of any inventory in Lamont’s refrigeration units after the balance sheet date to confirm its

condition.

■ An aged-inventory analysis and recalculation of any allowance for slow-moving items.

■ A review of after-date sales invoices for large quantities of fish to confirm that fair value (less costs to sell) exceed

carrying amount.

■ A review of after-date credit notes for any returns of contaminated/perished or otherwise substandard fish.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-01-09

- 2020-02-26

- 2020-09-05

- 2020-02-26

- 2020-02-28

- 2020-01-10

- 2020-02-26

- 2019-01-06

- 2020-01-10

- 2020-01-09

- 2020-01-09

- 2020-01-03

- 2020-01-10

- 2020-01-09

- 2020-02-26

- 2020-01-10

- 2020-02-23

- 2020-01-10

- 2020-01-09

- 2019-01-06

- 2020-02-05

- 2020-02-22

- 2020-01-09

- 2020-01-09

- 2020-02-26

- 2019-01-17

- 2019-01-17

- 2020-01-01

- 2020-02-23

- 2020-01-10