关于考下ACCA证书有什么好处,速来本篇文章了解!

发布时间:2020-01-30

ACCA会员资格在国际上得到广泛认可,尤其得到欧盟立法以及许多国家公司法的承认。所以拥有ACCA会员资格,就拥有了在世界各地就业的"通行证"。接下来,大家一起看看考下ACCA证书的好处吧。

ACCA的课程就是根据现时商务社会对财会人员的实际要求进行开发、设计的,特别注意培养学员的分析能力和在复杂条件下的决策、判断能力。系统的、高质量的培训给予学员真才实学,学员学成后能适应各种环境,并逐步成为具有全面管理素质的高级财务管理专家。

ACCA会员可在工商企业财务部门、审计/会计师事务所、金融机构和财政、税务部门从事财务和财务管理工作。很多会员在世界各地大公司担任高级职位(财务经理、财务总监CFO,甚至总裁CEO)。

考ACCA证书有什么好处?

一、ACCA证书对于学生能力的培养

获得ACCA证书的同学需要通过13门全英文考试科目,这13门科目的考试难度呈阶梯状,循序渐进,所以即使是零基础的小伙伴也不必过于担忧。ACCA证书的考试,课本,考纲全都以英文形式进行,培养出来学员具有国际思维,实际解决能力的问题比较强,在就业时也会更受到国际企业的青睐。

二、ACCA证书对于学历的作用

ACCA在全球范围内得到众多大学的认可如ACCA与英国牛津布鲁克斯大学合作,在学员通过ACCA前2个阶段(F7/F8/F9不可免考)的考试后,需向院校提交相关学位申请论文及其他证明文件,就可以获得由该所大学颁发的会计学应用理学学士学位。另外英国伦敦大学国际会计硕士学位也对ACCA学员开放!符合申请条件的学员若能通过UOL考试模块与论文模块,则将获得由英国伦敦大学(UOL)颁发的会计学专业硕士学位。不出国即可实现拿到海外学历,实现学历的提升。

三、ACCA证书在就业上的作用

更重要的是ACCA为获得ACCA学员所设立的绿色就业通道,全球已经有超过7,200家认可雇主如国际四大会计师事务所,花旗银行等行业龙头的企业在招聘员工时会优先录取持有ACCA证书的人,而且在四大,持有ACCA证书的员工在基础工资的基础上会比没有证书的员工多一份Q-pay。

好的,以上就是今天51题库考试学习网为大家分享的全部内容,大家清楚了吗?想了解更多内容,敬请关注51题库考试学习网!

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

There has been significant divergence in practice over recognition of revenue mainly because International Financial Reporting Standards (IFRS) have contained limited guidance in certain areas. The International Accounting Standards Board (IASB) as a result of the joint project with the US Financial Accounting Standards Board (FASB) has issued IFRS 15 Revenue from Contracts with Customers. IFRS 15 sets out a five-step model, which applies to revenue earned from a contract with a customer with limited exceptions, regardless of the type of revenue transaction or the industry. Step one in the five-step model requires the identification of the contract with the customer and is critical for the purpose of applying the standard. The remaining four steps in the standard’s revenue recognition model are irrelevant if the contract does not fall within the scope of IFRS 15.

Required:

(a) (i) Discuss the criteria which must be met for a contract with a customer to fall within the scope of IFRS 15. (5 marks)

(ii) Discuss the four remaining steps which lead to revenue recognition after a contract has been identified as falling within the scope of IFRS 15. (8 marks)

(b) (i) Tang enters into a contract with a customer to sell an existing printing machine such that control of the printing machine vests with the customer in two years’ time. The contract has two payment options. The customer can pay $240,000 when the contract is signed or $300,000 in two years’ time when the customer gains control of the printing machine. The interest rate implicit in the contract is 11·8% in order to adjust for the risk involved in the delay in payment. However, Tang’s incremental borrowing rate is 5%. The customer paid $240,000 on 1 December 2014 when the contract was signed. (4 marks)

(ii) Tang enters into a contract on 1 December 2014 to construct a printing machine on a customer’s premises for a promised consideration of $1,500,000 with a bonus of $100,000 if the machine is completed within 24 months. At the inception of the contract, Tang correctly accounts for the promised bundle of goods and services as a single performance obligation in accordance with IFRS 15. At the inception of the contract, Tang expects the costs to be $800,000 and concludes that it is highly probable that a significant reversal in the amount of cumulative revenue recognised will occur. Completion of the printing machine is highly susceptible to factors outside of Tang’s influence, mainly issues with the supply of components.

At 30 November 2015, Tang has satisfied 65% of its performance obligation on the basis of costs incurred to date and concludes that the variable consideration is still constrained in accordance with IFRS 15. However, on 4 December 2015, the contract is modified with the result that the fixed consideration and expected costs increase by $110,000 and $60,000 respectively. The time allowable for achieving the bonus is extended by six months with the result that Tang concludes that it is highly probable that the bonus will be achieved and that the contract still remains a single performance obligation. Tang has an accounting year end of 30 November. (6 marks)

Required:

Discuss how the above two contracts should be accounted for under IFRS 15. (In the case of (b)(i), the discussion should include the accounting treatment up to 30 November 2016 and in the case of (b)(ii), the accounting treatment up to 4 December 2015.)

Note: The mark allocation is shown against each of the items above.

Professional marks will be awarded in question 4 for clarity and quality of presentation. (2 marks)

(a) (i) The definition of what constitutes a contract for the purpose of applying the standard is critical. The definition of contract is based on the definition of a contract in the USA and is similar to that in IAS 32 Financial Instruments: Presentation. A contract exists when an agreement between two or more parties creates enforceable rights and obligations between those parties. The agreement does not need to be in writing to be a contract but the decision as to whether a contractual right or obligation is enforceable is considered within the context of the relevant legal framework of a jurisdiction. Thus, whether a contract is enforceable will vary across jurisdictions. The performance obligation could include promises which result in a valid expectation that the entity will transfer goods or services to the customer even though those promises are not legally enforceable.

The first criteria set out in IFRS 15 is that the parties should have approved the contract and are committed to perform. their respective obligations. It would be questionable whether that contract is enforceable if this were not the case. In the case of oral or implied contracts, this may be difficult but all relevant facts and circumstances should be considered in assessing the parties’ commitment. The parties need not always be committed to fulfilling all of the obligations under a contract. IFRS 15 gives the example where a customer is required to purchase a minimum quantity of goods but past experience shows that the customer does not always do this and the other party does not enforce their contract rights. However, there needs to be evidence that the parties are substantially committed to the contract.

It is essential that each party’s rights and the payment terms can be identified regarding the goods or services to be transferred. This latter requirement is the key to determining the transaction price.

The contract must have commercial substance before revenue can be recognised, as without this requirement, entities might artificially inflate their revenue and it would be questionable whether the transaction has economic consequences. Further, it should be probable that the entity will collect the consideration due under the contract. An assessment of a customer’s credit risk is an important element in deciding whether a contract has validity but customer credit risk does not affect the measurement or presentation of revenue. The consideration may be different to the contract price because of discounts and bonus offerings. The entity should assess the ability of the customer to pay and the customer’s intention to pay the consideration. If a contract with a customer does not meet these criteria, the entity can continually re-assess the contract to determine whether it subsequently meets the criteria.

Two or more contracts which are entered into around the same time with the same customer may be combined and accounted for as a single contract, if they meet the specified criteria. The standard provides detailed requirements for contract modifications. A modification may be accounted for as a separate contract or a modification of the original contract, depending upon the circumstances of the case.

(ii) Step one in the five-step model requires the identification of the contract with the customer. After a contract has been determined to fall under IFRS 15, the following steps are required before revenue can be recognised.

Step two requires the identification of the separate performance obligations in the contract. This is often referred to as ’unbundling’, and is done at the beginning of a contract. The key factor in identifying a separate performance obligation is the distinctiveness of the good or service, or a bundle of goods or services. A good or service is distinct if the customer can benefit from the good or service on its own or together with other readily available resources and is separately identifiable from other elements of the contract. IFRS 15 requires a series of distinct goods or services which are substantially the same with the same pattern of transfer, to be regarded as a single performance obligation. A good or service, which has been delivered, may not be distinct if it cannot be used without another good or service which has not yet been delivered. Similarly, goods or services which are not distinct should be combined with other goods or services until the entity identifies a bundle of goods or services which is distinct. IFRS 15 provides indicators rather than criteria to determine when a good or service is distinct within the context of the contract. This allows management to apply judgement to determine the separate performance obligations which best reflect the economic substance of a transaction.

Step three requires the entity to determine the transaction price, which is the amount of consideration which an entity expects to be entitled to in exchange for the promised goods or services. This amount excludes amounts collected on behalf of a third party, for example, government taxes. An entity must determine the amount of consideration to which it expects to be entitled in order to recognise revenue.

The transaction price might include variable or contingent consideration. Variable consideration should be estimated as either the expected value or the most likely amount. Management should use the approach which it expects will best predict the amount of consideration and should be applied consistently throughout the contract. An entity can only include variable consideration in the transaction price to the extent that it is highly probable that a subsequent change in the estimated variable consideration will not result in a significant revenue reversal. If it is not appropriate to include all of the variable consideration in the transaction price, the entity should assess whether it should include part of the variable consideration. However, this latter amount still has to pass the ’revenue reversal’ test.

Additionally, an entity should estimate the transaction price taking into account non-cash consideration, consideration payable to the customer and the time value of money if a significant financing component is present. The latter is not required if the time period between the transfer of goods or services and payment is less than one year. If an entity anticipates that it may ultimately accept an amount lower than that initially promised in the contract due to, for example, past experience of discounts given, then revenue would be estimated at the lower amount with the collectability of that lower amount being assessed. Subsequently, if revenue already recognised is not collectable, impairment losses should be taken to profit or loss.

Step four requires the allocation of the transaction price to the separate performance obligations. The allocation is based on the relative standalone selling prices of the goods or services promised and is made at inception of the contract. It is not adjusted to reflect subsequent changes in the standalone selling prices of those goods or services. The best evidence of standalone selling price is the observable price of a good or service when the entity sells that good or service separately. If that is not available, an estimate is made by using an approach which maximises the use of observable inputs. For example, expected cost plus an appropriate margin or the assessment of market prices for similar goods or services adjusted for entity-specific costs and margins or in limited circumstances a residual approach. When a contract contains more than one distinct performance obligation, an entity allocates the transaction price to each distinct performance obligation on the basis of the standalone selling price.

Where the transaction price includes a variable amount and discounts, consideration needs to be given as to whether these amounts relate to all or only some of the performance obligations in the contract. Discounts and variable consideration will typically be allocated proportionately to all of the performance obligations in the contract. However, if certain conditions are met, they can be allocated to one or more separate performance obligations.

Step five requires revenue to be recognised as each performance obligation is satisfied. An entity satisfies a performance obligation by transferring control of a promised good or service to the customer, which could occur over time or at a point in time. The definition of control includes the ability to prevent others from directing the use of and obtaining the benefits from the asset. A performance obligation is satisfied at a point in time unless it meets one of three criteria set out in IFRS 15. Revenue is recognised in line with the pattern of transfer.

If an entity does not satisfy its performance obligation over time, it satisfies it at a point in time and revenue will be recognised when control is passed at that point in time. Factors which may indicate the passing of control include the present right to payment for the asset or the customer has legal title to the asset or the entity has transferred physical possession of the asset.

(b) (i) The contract contains a significant financing component because of the length of time between when the customer pays for the asset and when Tang transfers the asset to the customer, as well as the prevailing interest rates in the market. A contract with a customer which has a significant financing component should be separated into a revenue component (for the notional cash sales price) and a loan component. Consequently, the accounting for a sale arising from a contract which has a significant financing component should be comparable to the accounting for a loan with the same features. An entity should use the discount rate which would be reflected in a separate financing transaction between the entity and its customer at contract inception. The interest rate implicit in the transaction may be different from the rate to be used to discount the cash flows, which should be the entity’s incremental borrowing rate. IFRS 15 would therefore dictate that the rate which should be used in adjusting the promised consideration is 5%, which is the entity’s incremental borrowing rate, and not 11·8%.

Tang would account for the significant financing component as follows:

Recognise a contract liability for the $240,000 payment received on 1 December 2014 at the contract inception:

Dr Cash $240,000

Cr Contract liability $240,000

During the two years from contract inception (1 December 2014) until the transfer of the printing machine, Tang adjusts the amount of consideration and accretes the contract liability by recognising interest on $240,000 at 5% for two years.

Year to 30 November 2015

Dr Interest expense $12,000

Cr Contract liability $12,000

Contract liability would stand at $252,000 at 30 November 2015.

Year to 30 November 2016

Dr Interest expense $12,600

Cr Contract liability $12,600

Recognition of contract revenue on transfer of printing machine at 30 November 2016 of $264,600 by debiting contract liability and crediting revenue with this amount.

(ii) Tang accounts for the promised bundle of goods and services as a single performance obligation satisfied over time in accordance with IFRS 15. At the inception of the contract, Tang expects the following:

Transaction price $1,500,000

Expected costs $800,000

Expected profit (46·7%) $700,000

At contract inception, Tang excludes the $100,000 bonus from the transaction price because it cannot conclude that it is highly probable that a significant reversal in the amount of cumulative revenue recognised will not occur. Completion of the printing machine is highly susceptible to factors outside the entity’s influence. By the end of the first year, the entity has satisfied 65% of its performance obligation on the basis of costs incurred to date. Costs incurred to date are therefore $520,000 and Tang reassesses the variable consideration and concludes that the amount is still constrained. Therefore at 30 November 2015, the following would be recognised:

Revenue $975,000

Costs $520,000

Gross profit $455,000

However, on 4 December 2015, the contract is modified. As a result, the fixed consideration and expected costs increase by $110,000 and $60,000, respectively. The total potential consideration after the modification is $1,710,000 which is $1,610,000 fixed consideration + $100,000 completion bonus. In addition, the allowable time for achieving the bonus is extended by six months with the result that Tang concludes that it is highly probable that including the bonus in the transaction price will not result in a significant reversal in the amount of cumulative revenue recognised in accordance with IFRS 15. Therefore the bonus of $100,000 can be included in the transaction price. Tang also concludes that the contract remains a single performance obligation. Thus,Tang accounts for the contract modification as if it were part of the original contract. Therefore, Tang updates its estimates of costs and revenue as follows:

Tang has satisfied 60·5% of its performance obligation ($520,000 actual costs incurred compared to $860,000 total expected costs). The entity recognises additional revenue of $59,550 [(60·5% of $1,710,000) – $975,000 revenue recognised to date] at the date of the modification as a cumulative catch-up adjustment. As the contract amendment took place after the year end, the additional revenue would not be treated as an adjusting event.

(ii) the recent financial performance of Merton plc from a shareholder perspective. Clearly identify any

issues that you consider should be brought to the attention of the ordinary shareholders. (15 marks)

(ii) Discussion of financial performance

It is clear that 2006 has been a difficult year for Merton plc. There are very few areas of interest to shareholders where

anything positive can be found to say.

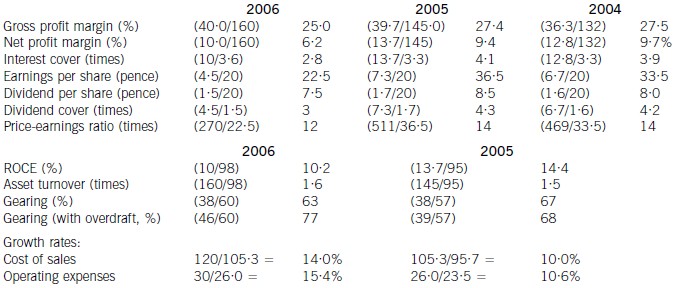

Profitability

Return on capital employed has declined from 14·4% in 2005, which compared favourably with the sector average of

12%, to 10·2% in 2006. Since asset turnover has improved from 1·5 to 1·6 in the same period, the cause of the decline

is falling profitability. Gross profit margin has fallen each year from 27·5% in 2004 to 25% in 2006, equal to the sector

average, despite an overall increase in turnover during the period of 10% per year. Merton plc has been unable to keep

cost of sales increases (14% in 2006 and 10% in 2005) below the increases in turnover. Net profit margin has declined

over the same period from 9·7% to 6·2%, compared to the sector average of 8%, because of substantial increases in

operating expenses (15·4% in 2006 and 10·6% in 2005). There is a pressing need here for Merton plc to bring cost

of sales and operating costs under control in order to improve profitability.

Gearing and financial risk

Gearing as measured by debt/equity has fallen from 67% (2005) to 63% (2006) because of an increase in

shareholders’ funds through retained profits. Over the same period the overdraft has increased from £1m to £8m and

cash balances have fallen from £16m to £1m. This is a net movement of £22m. If the overdraft is included, gearing

has increased to 77% rather than falling to 63%.

None of these gearing levels compare favourably with the average gearing for the sector of 50%. If we consider the large

increase in the overdraft, financial risk has clearly increased during the period. This is also evidenced by the decline in

interest cover from 4·1 (2005) to 2·8 (2006) as operating profit has fallen and interest paid has increased. In each year

interest cover has been below the sector average of eight and the current level of 2·8 is dangerously low.

Share price

As the return required by equity investors increases with increasing financial risk, continued increases in the overdraft

will exert downward pressure on the company’s share price and further reductions may be expected.

Investor ratios

Earnings per share, dividend per share and dividend cover have all declined from 2005 to 2006. The cut in the dividend

per share from 8·5 pence per share to 7·5 pence per share is especially worrying. Although in its announcement the

company claimed that dividend growth and share price growth was expected, it could have chosen to maintain the

dividend, if it felt that the current poor performance was only temporary. By cutting the dividend it could be signalling

that it expects the poor performance to continue. Shareholders have no guarantee as to the level of future dividends.

This view could be shared by the market, which might explain why the price-earnings ratio has fallen from 14 times to

12 times.

Financing strategy

Merton plc has experienced an increase in fixed assets over the last period of £10m and an increase in stocks and

debtors of £21m. These increases have been financed by a decline in cash (£15m), an increase in the overdraft (£7m)

and an increase in trade credit (£6m). The company is following an aggressive strategy of financing long-term

investment from short-term sources. This is very risky, since if the overdraft needed to be repaid, the company would

have great difficulty in raising the funds required.

A further financing issue relates to redemption of the existing debentures. The 10% debentures are due to be redeemed

in two years’ time and Merton plc will need to find £13m in order to do this. It does not appear that this sum can be

raised internally. While it is possible that refinancing with debt paying a lower rate of interest may be possible, the low

level of interest cover may cause concern to potential providers of debt finance, resulting in a higher rate of interest. The

Finance Director of Merton plc needs to consider the redemption problem now, as thought is currently being given to

raising a substantial amount of new equity finance. This financing choice may not be available again in the near future,

forcing the company to look to debt finance as a way of effecting redemption.

Overtrading

The evidence produced by the financial analysis above is that Merton plc is showing some symptoms of overtrading

(undercapitalisation). The board are suggesting a rights issue as a way of financing an expansion of business, but it is

possible that a rights issue will be needed to deal with the overtrading problem. This is a further financing issue requiring

consideration in addition to the redemption of debentures mentioned earlier.

Conclusion

Ordinary shareholders need to be aware of the following issues.

1. Profitability has fallen over the last year due to poor cost control

2. A substantial increase in the overdraft over the last year has caused gearing to increase

3. It is possible that the share price will continue to fall

4. The dividend cut may warn of continuing poor performance in the future

5. A total of £13m of debentures need redeeming in two year’s time

6. A large amount of new finance is needed for working capital and debenture redemption

Appendix: Analysis of key ratios and financial information

(c) Explain how the introduction of an ERPS could impact on the role of management accountants. (5 marks)

(c) The introduction of ERPS has the potential to have a significant impact on the work of management accountants. The use of

ERPS causes a substantial reduction in the gathering and processing of routine information by management accountants.

Instead of relying on management accountants to provide them with information, managers are able to access the system to

obtain the information they require directly via a suitable electronic access medium.

ERPS integrate separate business functions in one system for the entire organisation and therefore co-ordination is usually

undertaken centrally by information management specialists who have a dual responsibility for the implementation and

operation of the system.

ERPS perform. routine tasks that not so long ago were seen as an essential part of the daily routines of management

accountants, for example perpetual inventory valuation. Therefore if the value of the role of management accountants is not

to be diminished then it is of necessity that management accountants should seek to expand their roles within their

organisations.

The management accountant will also control and audit the ERPS data input and analysis. Hence the implementation of ERPS

provides the management accountant with an opportunity to change the emphasis of their role from information gathering

and processing to that of the role of advisers and internal consultants to their organisations. This new role will require

management accountants to be involved in interpreting the information generated from the ERPS and to provide business

support for all levels of management within an organisation.

(c) Increasing the revaluation reserve to $300,000 by revaluing goodwill from $800,000 to $1,000,000.

(1 mark)

(c) IFRS 3 Business combinations does not allow goodwill to be revalued upwards.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2019-03-27

- 2019-03-30

- 2019-01-04

- 2020-01-10

- 2020-05-09

- 2020-02-04

- 2020-02-21

- 2020-04-17

- 2020-03-11

- 2020-05-07

- 2020-01-10

- 2020-02-18

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2019-11-27

- 2019-07-20

- 2020-01-10

- 2020-04-21

- 2020-04-06

- 2020-04-19

- 2019-07-20

- 2020-05-01

- 2020-04-18

- 2020-01-10

- 2021-06-25

- 2020-04-23

- 2021-08-21

- 2020-01-10

- 2020-01-09