证书界,ACCA,CPA,司考到底最适合哪个行业?

发布时间:2019-01-11

秋招临近,不少准毕业生开始为面试做准备。昨天,有朋友发来微信,“准备跳槽金融行业,ACCA,司考,CPA,三张证书在简历上怎么排序比较好,哪一张应该突出?”

不得不说这是个好问题,听够了证书间的互相diss,理性分析一波各自的属性相当重要。大体来说,三张证书分别在三种应用场景中被视为顶级证书,当然,相互指尖也可以重叠。

如果想去外企,首选突出:ACCA

三张证书没有绝对的高低之分,况且司考和会计连属性都不同。但是对于用人单位来说,三张证书分别意味着求职者不同的能力。

对于立志进外企做财务的求职者们来说,请一定将ACCA加粗加黑放在简历第一行。

之所以要这样做,有三个原因:

1.ACCA曾被称为“国际注会”,在国际上知名度极高,不论是ACCA的故乡英国,还是欧洲,澳大利亚,美国,ACCA都是受到当地法律认可的会计师执业资格证书。因此将ACCA放在醒目位置可以让外企HR在一堆不熟悉的中国大学名称和证书名称之间瞬间找到一份熟悉且优秀的简历。

2.ACCA是全英文证书,全英文考试和培训,名副其实的国际证书。通常考完一遍ACCA后英文读写能力能获得全方位提升。这也是不少外企青睐ACCA的原因之一,别以为外企办公语言是中文就不用掌握英文,试想收到外国高管的新年祝福短信,用中文回复,还是用语法错误的英文回复,还是,用地道的英文回复?

3.目前ACCA在全世界有7400+“认可雇主”,包括大部分世界500强企业,通常ACCA认可雇主们会更喜欢ACCA持有者,并且在企业内部也会为员工提供ACCA考试费用报销。所以说,一定要在简历上标出ACCA,说不定即将面试的这家企业正是ACCA认可雇主呢。

如果想做审计,首选突出:CPA

审计是个很大的概念,四大会计师事务所只是其中一部分,还有本土八大,各类小所,企业内部审计部门,国家财政机关,等等。

虽然可选行业很多,但在中国万变不离其宗的是,CPA是王道。在中国,CPA是唯一拥有法律赋予的签字权的会计证书。因此不论在审计界的任何场合,CPA都代表着专业,权威,实力。CPA因为极为严苛的考试和极低的通过率,在财会类证书中有着无与伦比的稀有度。

如果做审计,请一定将CPA放在简历的最醒目位置,让HR一眼看到你。

如果想做金融,首选突出:司考

对于金融行业来说,规避法律风险是个大问题,所以法律人才供不应求。

即便是带着财会背景的CPA和ACCA人才,也请将法律从业资格证放在最前面。主要原因在于,金融行业虽然对ACCA等国际证书有较高认可度,但金融本身也有自己的对口证书,例如CFA注册金融分析师。

总结一下,三张证书在不同领域,各自都是顶尖证书,具体应该如何发挥证书的最大价值,请视自身情况而定。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(b) You are the manager responsible for the audit of Poppy Co, a manufacturing company with a year ended

31 October 2008. In the last year, several investment properties have been purchased to utilise surplus funds

and to provide rental income. The properties have been revalued at the year end in accordance with IAS 40

Investment Property, they are recognised on the statement of financial position at a fair value of $8 million, and

the total assets of Poppy Co are $160 million at 31 October 2008. An external valuer has been used to provide

the fair value for each property.

Required:

(i) Recommend the enquiries to be made in respect of the external valuer, before placing any reliance on their

work, and explain the reason for the enquiries; (7 marks)

(b) (i) Enquiries in respect of the external valuer

Enquiries would need to be made for two main reasons, firstly to determine the competence, and secondly the objectivity

of the valuer. ISA 620 Using the Work of an Expert contains guidance in this area.

Competence

Enquiries could include:

– Is the valuer a member of a recognised professional body, for example a nationally or internationally recognised

institute of registered surveyors?

– Does the valuer possess any necessary licence to carry out valuations for companies?

– How long has the valuer been a member of the recognised body, or how long has the valuer been licensed under

that body?

– How much experience does the valuer have in providing valuations of the particular type of investment properties

held by Poppy Co?

– Does the valuer have specific experience of evaluating properties for the purpose of including their fair value within

the financial statements?

– Is there any evidence of the reputation of the valuer, e.g. professional references, recommendations from other

companies for which a valuation service has been provided?

– How much experience, if any, does the valuer have with Poppy Co?

Using the above enquiries, the auditor is trying to form. an opinion as to the relevance and reliability of the valuation

provided. ISA 500 Audit Evidence requires that the auditor gathers evidence that is both sufficient and appropriate. The

auditor needs to ensure that the fair values provided by the valuer for inclusion in the financial statements have been

arrived at using appropriate knowledge and skill which should be evidenced by the valuer being a member of a

professional body, and, if necessary, holding a licence under that body.

It is important that the fair values have been arrived at using methods allowed under IAS 40 Investment Property. If any

other valuation method has been used then the value recognised in the statement of financial position may not be in

accordance with financial reporting standards. Thus it is important to understand whether the valuer has experience

specifically in providing valuations that comply with IAS 40, and how many times the valuer has appraised properties

similar to those owned by Poppy Co.

In gauging the reliability of the fair value, the auditor may wish to consider how Poppy Co decided to appoint this

particular valuer, e.g. on the basis of a recommendation or after receiving references from companies for which

valuations had previously been provided.

It will also be important to consider how familiar the valuer is with Poppy Co’s business and environment, as a way to

assess the reliability and appropriateness of any assumptions used in the valuation technique.

Objectivity

Enquiries could include:

– Does the valuer have any financial interest in Poppy Co, e.g. shares held directly or indirectly in the company?

– Does the valuer have any personal relationship with any director or employee of Poppy Co?

– Is the fee paid for the valuation service reasonable and a fair, market based price?

With these enquiries, the auditor is gaining assurance that the valuer will perform. the valuation from an independent

point of view. If the valuer had a financial interest in Poppy Co, there would be incentive to manipulate the valuation in

a way best suited to the financial statements of the company. Equally if the valuer had a personal relationship with a

senior member of staff at Poppy Co, the valuer may feel pressured to give a favourable opinion on the valuation of the

properties.

The level of fee paid is important. It should be commensurate with the market rate paid for this type of valuation. If the

valuer was paid in excess of what might be considered a normal fee, it could indicate that the valuer was encouraged,

or even bribed, to provide a favourable valuation.

5 International Financial Reporting Standards (IFRSs) are primarily designed for use by publicly listed companies and

in many countries the majority of companies using IFRSs are listed companies. In other countries IFRSs are used as

national Generally Accepted Accounting Practices (GAAP) for all companies including unlisted entities. It has been

argued that the same IFRSs should be used by all entities or alternatively a different body of standards should apply

to small and medium entities (SMEs).

Required:

(a) Discuss whether there is a need to develop a set of IFRSs specifically for SMEs. (7 marks)

5 (a) IFRSs were not designed specifically for listed companies. However, in many countries the main users of IFRS are listed

companies. Currently SMEs who adopt IFRS have to follow all the requirements and not all SMEs take exception to applying

IFRS because it gives their financial statements enhanced reliability, relevance and credibility, and results in fair presentation.

However, other SMEs will wish to comply with IFRS for consistency and comparability purposes within their own country and

internationally but wish to apply simplified or different standards relevant to SMEs on the grounds that some IFRS are

unnecessarily demanding and some of the information produced is not used by users of SME financial statements.

The objectives of general purpose financial statements are basically appropriate for SMEs and publicly listed companies alike.

Therefore there is an argument that there is a need for only one set of IFRS which could be used nationally and internationally.

However, some SMEs require different financial information than listed companies. For example expanded related party

disclosures may be useful as SMEs often raise capital from shareholders, directors and suppliers. Additionally directors often

offer personal assets as security for bank finance.

The cost burden of applying the full set of IFRS may not be justified on the basis of user needs. The purpose and usage of

the financial statements, and the nature of the accounting expertise available to the SME, will not be the same as for listed

companies. These circumstances themselves may provide justification for a separate set of IFRSs for SMEs. A problem which

might arise is that users become familiar with IFRS as opposed to local GAAP thus creating a two tier system which could

lead to local GAAP being seen as an inferior or even a superior set of accounting rules.

One course of action would be for GAAP for SMEs to be developed on a national basis with IFRS being focused on accounting

for listed company activities. The main issue here would be that the practices developed for SMEs may not be consistent and

may lack comparability across national boundaries. This may mean that where SMEs wish to list their shares on a capital

market, the transition to IFRSs may be difficult. It seems that national standards setters are strongly supportive of thedevelopment of IFRSs for SMEs.

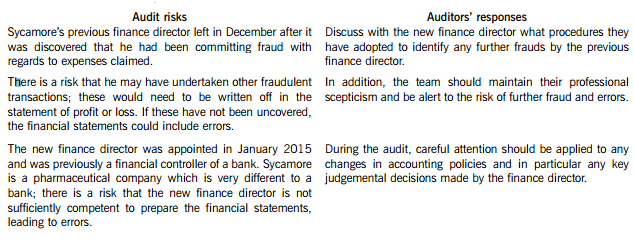

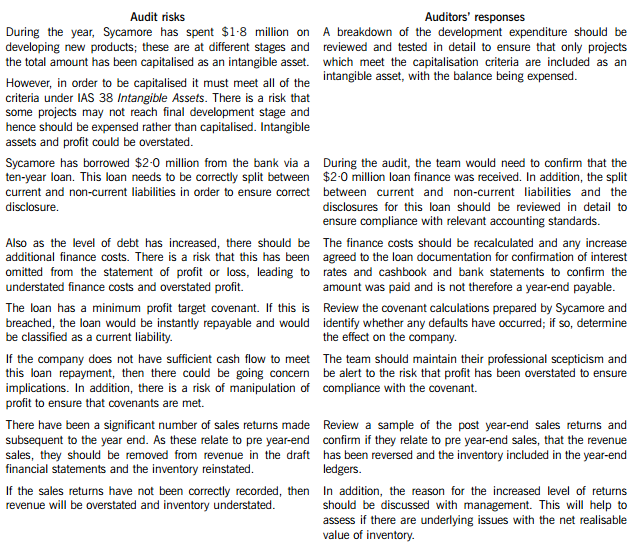

You are the audit supervisor of Maple & Co and are currently planning the audit of an existing client, Sycamore Science Co (Sycamore), whose year end was 30 April 2015. Sycamore is a pharmaceutical company, which manufactures and supplies a wide range of medical supplies. The draft financial statements show revenue of $35·6 million and profit before tax of $5·9 million.

Sycamore’s previous finance director left the company in December 2014 after it was discovered that he had been claiming fraudulent expenses from the company for a significant period of time. A new finance director was appointed in January 2015 who was previously a financial controller of a bank, and she has expressed surprise that Maple & Co had not uncovered the fraud during last year’s audit.

During the year Sycamore has spent $1·8 million on developing several new products. These projects are at different stages of development and the draft financial statements show the full amount of $1·8 million within intangible assets. In order to fund this development, $2·0 million was borrowed from the bank and is due for repayment over a ten-year period. The bank has attached minimum profit targets as part of the loan covenants.

The new finance director has informed the audit partner that since the year end there has been an increased number of sales returns and that in the month of May over $0·5 million of goods sold in April were returned.

Maple & Co attended the year-end inventory count at Sycamore’s warehouse. The auditor present raised concerns that during the count there were movements of goods in and out the warehouse and this process did not seem well controlled.

During the year, a review of plant and equipment in the factory was undertaken and surplus plant was sold, resulting in a profit on disposal of $210,000.

Required:

(a) State Maples & Co’s responsibilities in relation to the prevention and detection of fraud and error. (4 marks)

(b) Describe SIX audit risks, and explain the auditor’s response to each risk, in planning the audit of Sycamore Science Co. (12 marks)

(c) Sycamore’s new finance director has read about review engagements and is interested in the possibility of Maple & Co undertaking these in the future. However, she is unsure how these engagements differ from an external audit and how much assurance would be gained from this type of engagement.

Required:

(i) Explain the purpose of review engagements and how these differ from external audits; and (2 marks)

(ii) Describe the level of assurance provided by external audits and review engagements. (2 marks)

(a) Fraud responsibility

Maple & Co must conduct an audit in accordance with ISA 240 The Auditor’s Responsibilities Relating to Fraud in an Audit of Financial Statements and are responsible for obtaining reasonable assurance that the financial statements taken as a whole are free from material misstatement, whether caused by fraud or error.

In order to fulfil this responsibility, Maple & Co is required to identify and assess the risks of material misstatement of the financial statements due to fraud.

They need to obtain sufficient appropriate audit evidence regarding the assessed risks of material misstatement due to fraud, through designing and implementing appropriate responses. In addition, Maple & Co must respond appropriately to fraud or suspected fraud identified during the audit.

When obtaining reasonable assurance, Maple & Co is responsible for maintaining professional scepticism throughout the audit, considering the potential for management override of controls and recognising the fact that audit procedures which are effective in detecting error may not be effective in detecting fraud.

To ensure that the whole engagement team is aware of the risks and responsibilities for fraud and error, ISAs require that a discussion is held within the team. For members not present at the meeting, Sycamore’s audit engagement partner should determine which matters are to be communicated to them.

(b) Audit risks and auditors’ responses

(c) (i) Review engagements

Review engagements are often undertaken as an alternative to an audit, and involve a practitioner reviewing financial data, such as six-monthly figures. This would involve the practitioner undertaking procedures to state whether anything has come to their attention which causes the practitioner to believe that the financial data is not in accordance with the financial reporting framework.

A review engagement differs to an external audit in that the procedures undertaken are not nearly as comprehensive as those in an audit, with procedures such as analytical review and enquiry used extensively. In addition, the practitioner does not need to comply with ISAs as these only relate to external audits.

(ii) Levels of assurance

The level of assurance provided by audit and review engagements is as follows:

External audit – A high but not absolute level of assurance is provided, this is known as reasonable assurance. This provides comfort that the financial statements present fairly in all material respects (or are true and fair) and are free of material misstatements.

Review engagements – where an opinion is being provided, the practitioner gathers sufficient evidence to be satisfied that the subject matter is plausible; in this case negative assurance is given whereby the practitioner confirms that nothing has come to their attention which indicates that the subject matter contains material misstatements.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-01-10

- 2020-02-27

- 2020-04-23

- 2020-01-30

- 2020-01-10

- 2020-01-09

- 2020-05-06

- 2020-01-09

- 2020-01-10

- 2020-05-09

- 2020-01-30

- 2020-04-19

- 2020-04-21

- 2020-01-10

- 2020-04-09

- 2020-01-09

- 2019-12-28

- 2020-01-09

- 2020-04-19

- 2020-01-10

- 2020-01-14

- 2020-01-09

- 2019-12-28

- 2020-01-10

- 2020-05-08

- 2020-01-03

- 2020-04-18

- 2020-02-20

- 2020-04-19

- 2019-01-04