你知道ACCA需要备考多久吗?

发布时间:2020-05-17

很多同学在了解ACCA之后,想考ACCA,又担心考试花费的时间太长。那么,你知道ACCA需要备考多久吗?一起来看看吧!

一、ACCA备考时间

ACCA每科学习时长,要根据自身情况而定。如果是自学可能需要时间更长一些,每门课程大概需要400小时左右,如果是参加培训,有老师指导,一般需要60小时左右。

二、ACCA可以自学

自学需要根据自己情况决定,如果个人英语基础和专业基础都比较好,部分科目可以自学。建议自学前去看一下ACCA的历年考题,衡量一下自己是否有能力自学。觉得有困难的同学,高顿小编建议参与培训,可以极大提高自己的考试通过率和考试速度。毕竟大学是今后人生中最好的学习时间,时间成本也需要考虑在内。

三、国际注册会计师考试难度

ACCA考试的难度是以英国大学学位考试的难度为标准,具体而言,第一、第二部分的难度分别相当于学士学位高年级课程的考试难度,第三部分的考试相当于硕士学位最后阶段的考试。

第一部分的每门考试只是测试本门课程所包含的知识,着重于为后两个部分中实务性的课程所要运用的理论和技能打下基础。

第二部分的考试除了本门课程的内容之外,还会考到第一部分的一些知识,着重培养学员的分析能力。

第三部分的考试要求学员综合运用学到的知识、技能和决断力。不仅会考到以前的课程内容,还会考到邻近科目的内容。

四、 国际注册会计师的通过率

ACCA全球单科通过率基本在40-60%左右,然而在国内通过培训机构的培训后,ACCA各科考试通过率平均为80%左右。

五、做题攻略

1、做第一遍题目,在看完全书后做,可能很多题不会做,理解不了题目的内涵,这是非常正常的,这不意味着看书的失败,而是缺乏全书的融会贯通,在这一阶段,多考虑应该怎么回答,再对照答案比较两者的差距,有一些题目比较难,看懂就达到目的。第二遍做题,不能急于看答案了,必须按照相应的时间要求,训练计算的准确、回答的完整和答题的速度,不要满足于算平、算对或答出要点,更要注意时间,注意表达。第三遍做题,应该要求又快又准,达到熟练的程度,同时在做完每一道题后,设想一下这类题目的变化方式。第四遍,在考前若干天,快速浏览题目,对解答方法和要点应该完全心中有数,对少数难题,在考前强记。

2、可能只有时间做三遍题,那么第一遍的尝试和上策一样,第二遍做题就要争取效果,最后一遍考前强化,应该有重点地选择题目进行练习。

3、在特殊情况下,只有时间做两遍题,那么,第一遍通览过程要求非常用心,大致记住全部答案;然后重点分析历年考题,选择本次的重点类型题目进行强化训练。

以上就是关于ACCA考试的相关信息了,希望可以帮助到你哦!想了解更多相关信息,请关注51题库考试学习网。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

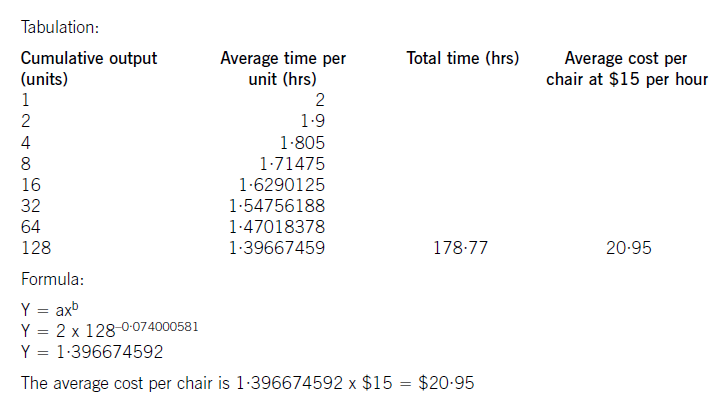

Big Cheese Chairs (BCC) manufactures and sells executive leather chairs. They are considering a new design of massaging chair to launch into the competitive market in which they operate.

They have carried out an investigation in the market and using a target costing system have targeted a competitive selling price of $120 for the chair. BCC wants a margin on selling price of 20% (ignoring any overheads).

The frame. and massage mechanism will be bought in for $51 per chair and BCC will upholster it in leather and assemble it ready for despatch.

Leather costs $10 per metre and two metres are needed for a complete chair although 20% of all leather is wasted in the upholstery process.

The upholstery and assembly process will be subject to a learning effect as the workers get used to the new design.

BCC estimates that the first chair will take two hours to prepare but this will be subject to a learning rate (LR) of 95%.

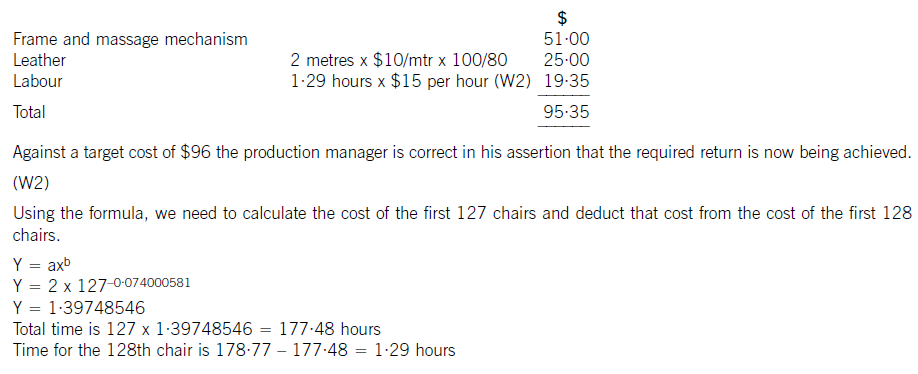

The learning improvement will stop once 128 chairs have been made and the time for the 128th chair will be the time for all subsequent chairs. The cost of labour is $15 per hour.

The learning formula is shown on the formula sheet and at the 95% learning rate the value of b is -0·074000581.

Required:

(a) Calculate the average cost for the first 128 chairs made and identify any cost gap that may be present at

that stage. (8 marks)

(b) Assuming that a cost gap for the chair exists suggest four ways in which it could be closed. (6 marks)

The production manager denies any claims that a cost gap exists and has stated that the cost of the 128th chair will be low enough to yield the required margin.

(c) Calculate the cost of the 128th chair made and state whether the target cost is being achieved on the 128th chair. (6 marks)

(W1)

The cost of the labour can be calculated using learning curve principles. The formula can be used or a tabular approach would

also give the average cost of 128 chairs. Both methods are acceptable and shown here.

(b) To reduce the cost gap various methods are possible (only four are needed for full marks)

– Re-design the chair to remove unnecessary features and hence cost

– Negotiate with the frame. supplier for a better cost. This may be easier as the volume of sales improve as suppliers often

are willing to give discounts for bulk buying. Alternatively a different frame. supplier could be found that offers a better

price. Care would be needed here to maintain the required quality

– Leather can be bought from different suppliers or at a better price also. Reducing the level of waste would save on cost.

Even a small reduction in waste rates would remove much of the cost gap that exists

– Improve the rate of learning by better training and supervision

– Employ cheaper labour by reducing the skill level expected. Care would also be needed here not to sacrifice quality or

push up waste rates.

(c) The cost of the 128th chair will be:

(c) mandatory continuing professional development (CPD) requirements. (5 marks)

(c) Continuing Professional Development (CPD)

CPD is defined5 as ‘the continuous maintenance, development and enhancement of the professional and personal knowledge

and skills which members of ACCA require throughout their working lives’.

All professional accountants need to maintain their competence and develop new skills to be effective in their current and

future employment. CPD helps keep accountants in practice employable and maintains their reputation with employers,

clients and the public. It also helps maintain the accounting profession’s reputation for producing and supporting high calibre

individuals. Therefore, CPD is something which professional accountants should take personal responsibility for, and be doing

as part of their everyday work.

Mandatory CPD for active members of IFAC member bodies (such as ACCA) was introduced with effect from 1 January 2005

onwards. ACCA has introduced CPD as a requirement for all active members, subject to the phasing-in dates (and waivers).

Tutorial note: IFAC issued International Education Standard (IES) 7, which requires the introduction of CPD for all active

members of IFAC member bodies.

ACCA practising certificate and insolvency licence holders are still required to participate in technical CPD training. All other

members will also be asked to state on their annual CPD return that they maintain competence in professional ethics.

The scheme is being introduced in phases:

■ phase 1 (2005) – members admitted since 1 January 2001, and all practising certificate and insolvency licence

holders;

■ phase 2 (2006) – members admitted between 1 January 1995 and 31 December 2000;

■ phase 3 (2007) – all remaining members.

Tutorial note: However, ACCA encouraged all members to adopt the scheme from 1 January 2005.

Affiliates join the CPD scheme on 1 January following their date of admittance to membership.

There are two routes to participation in ACCA’s CPD scheme:

(1) the unit scheme route (40 units approximate to 40 hours required each year); and

(2) the approved CPD employer route (i.e. where employers are recognised as effectively providing ACCA members with

CPD).

Tutorial note: Alternatively, if an ACCA member is also a member of another IFAC accounting body and that CPD scheme

is compliant with IFAC’s CPD IES 7, they may choose to follow that body’ s route.

2 Chen Products produces four manufactured products: Products 1, 2, 3 and 4. The company’s risk committee recently

met to discuss how the company might respond to a number of problems that have arisen with Product 2. After a

number of incidents in which Product 2 had failed whilst being used by customers, Chen Products had been presented

with compensation claims from customers injured and inconvenienced by the product failure. It was decided that the

risk committee should meet to discuss the options.

When the discussion of Product 2 began, committee chairman Anne Ricardo reminded her colleagues that, apart from

the compensation claims, Product 2 was a highly profitable product.

Chen’s risk management committee comprised four non-executive directors who each had different backgrounds and

areas of expertise. None of them had direct experience of Chen’s industry or products. It was noted that it was

common for them to disagree among themselves as to how risks should be managed and that in some situations,

each member proposed a quite different strategy to manage a given risk. This was the case when they discussed

which risk management strategy to adopt with regard to Product 2.

Required:

(a) Describe the typical roles of a risk management committee. (6 marks)

(a) Typical roles of a risk management committee

The typical roles of a risk management committee are as follows:

To agree and approve the risk management strategy and policies. The design of risk policy will take into account the

environment, the strategic posture towards risk, the product type and a range of other relevant factors.

Receiving and reviewing risk reports from affected departments. Some departments will file regular reports on key risks (such

as liquidity assessments from the accounting department, legal risks from the company secretariat or product risks from the

sales manager).

Monitoring overall exposure and specific risks. If the risk policy places limits on the total risk exposure for a given risk then

this role ensures that limits are adhered to. In the case of certain strategic risks, monitoring could occur on a very frequent

basis whereas for more operational risks, monitoring will more typically occur to coincide with risk management committee

meetings.

Assessing the effectiveness of risk management systems. This involves getting feedback from departments and the internal

audit function on the workings of current management and risk mitigation systems.

Providing general and explicit guidance to the main board on emerging risks and to report on existing risks. This will involve

preparing reports on apparent risks and assessing their probability of being realised and their potential impact if they do.

To work with the audit committee on designing and monitoring internal controls for the management and mitigation of risks.

If the risk committee is part of the executive structure, it will likely have an advisory role in respect of its input into the audit

committee. If it is non-executive, its input may be more directly influential.

[Tutorial note: other roles may be suggested that, if relevant, will be rewarded]

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-01-09

- 2020-04-20

- 2020-01-09

- 2020-03-28

- 2020-02-01

- 2020-04-10

- 2020-02-20

- 2020-01-09

- 2020-01-29

- 2020-01-01

- 2020-01-09

- 2020-01-09

- 2020-05-02

- 2019-07-19

- 2020-01-09

- 2020-01-09

- 2020-03-25

- 2020-01-09

- 2020-04-17

- 2020-04-23

- 2019-07-19

- 2020-04-05

- 2020-04-07

- 2020-01-09

- 2020-04-05

- 2020-03-14

- 2020-02-01

- 2020-02-28

- 2020-04-20

- 2020-01-09