2020年ACCA报名费要多少钱?

发布时间:2020-03-05

ACCA作为国际上知名的会计师组织,其会员资格证书含金量较高,不少人都将其作为进入“四大”的敲门砖。因此,近年来网上也增加了许多关于ACCA报名信息的询问,比如报名费用。鉴于此,51题库考试学习网在下面为大家带来ACCA考试费用的相关信息,以供参考。

想要参加ACCA考试,需要先注册成为ACCA会员。因此ACCA费用主要包括:注册费,年费,报名费,教材费。此外,部分选择了培训班的学员还会有培训费。

那么,这些费用的具体金额是多少呢?

1、注册费:79英镑(只缴纳一次)

2、年费:每年105英镑。大部分ACCA学员学习ACCA一般都需要三到四年,就按照四年年费来计算。

3、ACCA考试费用:(ACCA考试报名分为提前、常规以及后期三个阶段,各阶段考试费用不同,下面的所有考试费用都以早期缴费为准。)79+99+(F1-F4费用)+103*5(F5-F9)+180(SBL)+129*3(SBR+2门选修课)=1260+(F1-F4费用,费用是每科70-80英镑),根据目前的汇率,学员一共缴纳的ACCA官方报名费用约在人民币一万四到两万左右。再加上第一次报名所缴纳的费用,总计约为一万七千元左右。如果有同一科目多次报考或者考试通过时间过长的情况,考试费用很容易超过两万元。

以上就是关于ACCA考试费用的相关情况。ACCA考试费用较高,并且考试科目较多,因此小伙伴们在完成注册后应尽快进入备考状态,争取早日脱坑。最后,51题库考试学习网预祝准备参加2020年ACCA考试的小伙伴都能顺利通过。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

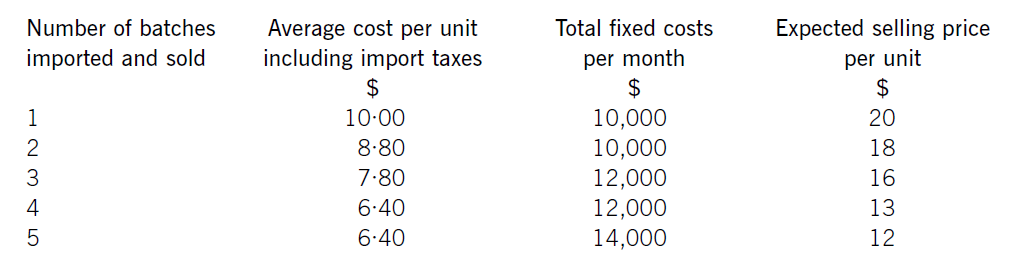

Jewel Co is setting up an online business importing and selling jewellery headphones. The cost of each set of headphones varies depending on the number purchased, although they can only be purchased in batches of 1,000 units. It also has to pay import taxes which vary according to the quantity purchased.

Jewel Co has already carried out some market research and identified that sales quantities are expected to vary depending on the price charged. Consequently, the following data has been established for the first month:

Required:

(a) Calculate how many batches Jewel Co should import and sell. (6 marks)

(b) Explain why Jewel Co could not use the algebraic method to establish the optimum price for its product.

(4 marks)

(b)Thealgebraicmodelrequiresseveralassumptionstobetrue.First,theremustbeaconsistentrelationshipbetweenprice(P)anddemand(Q),sothatademandequationcanbeestablished,usuallyintheform.P=a–bQ.Here,althoughthereisaclearrelationshipbetweenthetwo,itisnotaperfectlylinearrelationshipandsomorecomplicatedtechniquesarerequiredtocalculatethedemandequation.ItalsocannotbeassumedthatalinearrelationshipwillholdforallvaluesofPandQotherthanthefivegiven.Similarly,theremustbeaclearrelationshipbetweendemandandmarginalcost,usuallysatisfiedbyconstantvariablecostperunitandconstantfixedcosts.Thechangingvariablecostsperunitagaincomplicatetheissue,butitisthechangesinfixedcostswhichmakethealgebraicmethodlessusefulinJewel’scase.Thealgebraicmodelisonlysuitableforcompaniesoperatinginamonopolyanditisnotclearherewhetherthisisthecase,butitseemsunlikely,soany‘optimum’pricemightbecomeirrelevantifJewel’scompetitorschargesignificantlylowerprices.Othermoregeneralfactorsnotconsideredbythealgebraicmodelarepoliticalfactorswhichmightaffectimports,socialfactorswhichmayaffectcustomertastesandeconomicfactorswhichmayaffectexchangeratesorcustomerspendingpower.Thereliabilityoftheestimatesthemselves–forsalesprices,variablecostsandfixedcosts–couldalsobecalledintoquestion.

3 At a recent international meeting of business leaders, Seamus O’Brien said that multi-jurisdictional attempts to

regulate corporate governance were futile because of differences in national culture. He drew particular attention to

the Organisation for Economic Co-operation and Development (OECD) and International Corporate Governance

Network (ICGN) codes, saying that they were, ‘silly attempts to harmonise practice’. He said that in some countries,

for example, there were ‘family reasons’ for making the chairman and chief executive the same person. In other

countries, he said, the separation of these roles seemed to work. Another delegate, Alliya Yongvanich, said that the

roles of chief executive and chairman should always be separated because of what she called ‘accountability to

shareholders’.

One delegate, Vincent Viola, said that the right approach was to allow each country to set up its own corporate

governance provisions. He said that it was suitable for some countries to produce and abide by their own ‘very

structured’ corporate governance provisions, but in some other parts of the world, the local culture was to allow what

he called, ‘local interpretation of the rules’. He said that some cultures valued highly structured governance systems

while others do not care as much.

Required:

(a) Explain the roles of the chairman in corporate governance. (5 marks)

(a) Roles of the chairman in corporate governance

The chairman is the leader of the board of directors in a private or public company although other organisations are often run

on similar governance lines. In this role, he or she is responsible for ensuring the board’s effectiveness as a unit, in the service

of the shareholders. This means agreeing and, if necessary, setting the board’s agenda and ensuring that board meetings

take place on a regular basis.

The chairman represents the company to investors and other outside stakeholders/constituents. He or she is often the

‘public face’ of the organisation, especially if the organisation must account for itself in a public manner. Linked to this,

the chairman’s roles include communication with shareholders. This occurs in a statutory sense in the annual report

(where, in many jurisdictions, the chairman must write to shareholders each year in the form. of a chairman’s statement)

and at annual and extraordinary general meetings.

Internally, the chairman ensures that directors receive relevant information in advance of board meetings so that all

discussions and decisions are made by directors fully apprised of the situation under discussion. Finally, his or her role

extends to co-ordinating the contributions of non-executive directors (NEDs) and facilitating good relationships between

executive and non-executive directors.

(ii) List the additional information required in order to calculate the employment income benefit in respect

of the provision of the furnished flat for 2007/08 and advise Benny of the potential income tax

implications of requesting a more centrally located flat in accordance with the company’s offer.

(4 marks)

(ii) The flat

The following additional information is required in order to calculate the employment income benefit in respect of the

flat.

– The flat’s annual value.

– The cost of any improvements made to the flat prior to 6 April 2007.

– The cost of power, water, repairs and maintenance etc borne by Summer Glow plc.

– The cost of the furniture provided by Summer Glow plc.

– Any use of the flat by Benny wholly, exclusively and necessarily for the purposes of his employment.

Tutorial note

The market value of the flat is not required as Summer Glow plc has owned it for less than six years.

One element of the employment income benefit in respect of the flat is calculated by reference to its original cost plus

the cost of any capital improvements prior to 6 April 2007. If Benny requests a flat in a different location, this element

of the benefit will be computed instead by reference to the cost of the new flat, which in turn equals the proceeds of

sale of the old flat.

Accordingly, if, as is likely, the value of the flat has increased since it was purchased, Benny’s employment income

benefit will also increase. The increase in the employment income benefit will be the flat’s sales proceeds less its original

cost less the cost of any capital improvements prior to 6 April 2007 multiplied by 5%.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-03-29

- 2021-04-23

- 2020-01-09

- 2020-01-10

- 2019-07-21

- 2020-01-10

- 2019-07-21

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-03-11

- 2020-01-10

- 2020-01-09

- 2020-03-07

- 2020-04-21

- 2020-08-01

- 2020-02-28

- 2020-04-08

- 2020-01-08

- 2020-03-08

- 2020-01-10

- 2020-02-29

- 2020-03-20

- 2020-02-21

- 2020-01-08

- 2020-05-08

- 2020-01-10

- 2020-02-10

- 2020-03-04

- 2020-01-10