ACCA考试成绩查询方式以及如何申请成绩复核

发布时间:2020-09-04

各位小伙伴注意了!很多同学想知道ACCA考试成绩查询的方式,51题库考试学习网为大家带来了相关信息,让我们一起来看看吧!

成绩查询:

(一)在线查询:

1.进入ACCA官网http://www.accaglobal.com/hk/en.html

2.点击右上角My ACCA进行登录:

3.输入账号、密码登录后进入主页面,点击Exam status&Results:

4.跳转页面后选择View your status report:

进入后就可以查看自己的所有科目的考试通过情况了。

(二)通过邮件、手机信息接收成绩:

您可在MY ACCA内选择通过E-mail或SMS接收考试成绩。

如何申请成绩复核?

在评卷之前,ACCA评分团队要与考官开会,讨论试卷并确定统一详细的评分表。验卷团队会对每一份试卷进行仔细检查,确保每一道试题都没有漏评分,且每份试卷的总分是正确。在整个评卷过程中验卷团队总共要检查8次。在考试成绩发布之前,ACCA会再进行一次检查,以确保学员的ACCA考试成绩准确无误。

然而,ACCA也意识到有时候学员会对他们所获得的考试结果有所怀疑。因此,在以下情况下,您可以要求查卷。

1.您参加了考试,并提交了答卷,却说您缺席考试;

2.您缺席考试,却收到考试成绩;

3.您对自己的考试成绩有所怀疑。

您必须在考试成绩发布日后的15个工作日内提出查卷申请。如果ACCA成绩有误,您会在下次报考截止日期前收到改正了的成绩,但是ACCA的复核工作也要收取相应的费用(52英镑)。

ACCA考试成绩什么时候出?

ACCA考试可分为随机机考、分季机考与笔试三大部分,其中F阶段所有的科目都已经进入机考时代,F1-F4是随机机考,对于参加随机机考的同学来说,在考完之后,立刻就可以看到自己的成绩。F5-F9是分季机考,对于参加分季机考的同学来说,考试成绩通常会在结束考试的一个月后可以知道自己的成绩。而P阶段笔试考试成绩通常也是考试一个月后可以知道。

ACCA的有效期:

ACCA学员有七年的时间通过专业阶段的考试。如果学员不能在七年内通过所有专业阶段考试,那么超过七年的已通过专业阶段科目的成绩将作废,须重新考试。七年时限从学员通过第一门专业阶段考试之日算起。

说明:因考试政策、内容不断变化与调整,51题库考试学习网提供的考试信息仅供参考,如有异议,请考生以权威部门公布的内容为准!

以上就是今天分享的全部内容了,各位小伙伴根据自己的情况进行查阅,希望本文对各位有所帮助,预祝各位取得满意的成绩,如需了解更多相关内容,请关注51题库考试学习网!

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(b) What styles of managing change would you recommend John use to bring about the desired change?

(8 marks)

(b) Choosing the right combination of styles to manage the desired change will be an interesting challenge to John as the principal

change agent. Education and communication will be vital in getting the police officers to buy in to the need for change. It is

only by changing their perception of the nature and size of the city centre problem that any change in activity will be possible.

Communication will also be important to keep the other stakeholders informed and on board – in this case the mayor is likely

to be a key player.

Having convinced the police officers of the need for and achievability of the change John has then to motivate them to become

involved. This is achieved through collaboration and participation. John will determine the extent to which officers or task

groups are involved in various parts in the change process. Here the emphasis is on getting a shared ownership of the problem

and getting better solutions to parts of the problem. As with education and communication this may be a time-consuming

process.

Intervention by John may be needed at various points in the change process; he may delegate certain activities to others but

retain the coordination and control of the project. On occasions it may be necessary for John to take direct control over the

process in order to clarify and speed-up the whole process but such direction may cause a lack of acceptance and a poorly

conceived strategy. Finally, in times of crisis resort may have to be made to coercion/edict. This is likely to be the leastsuccessful means of managing change and should only be used when exceptional circumstances are present.

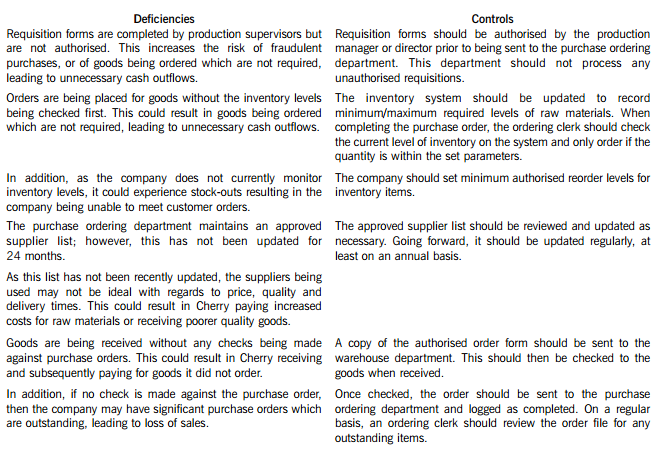

Cherry Blossom Co (Cherry) manufactures custom made furniture and its year end is 30 April. The company purchases its raw materials from a wide range of suppliers. Below is a description of Cherry’s purchasing system.

When production supervisors require raw materials, they complete a requisition form. and this is submitted to the purchase ordering department. Requisition forms do not require authorisation and no reference is made to the current inventory levels of the materials being requested. Staff in the purchase ordering department use the requisitions to raise sequentially numbered purchase orders based on the approved suppliers list, which was last updated 24 months ago. The purchasing director authorises the orders prior to these being sent to the suppliers.

When the goods are received, the warehouse department verifies the quantity to the suppliers despatch note and checks that the quality of the goods received are satisfactory. They complete a sequentially numbered goods received note (GRN) and send a copy of the GRN to the finance department.

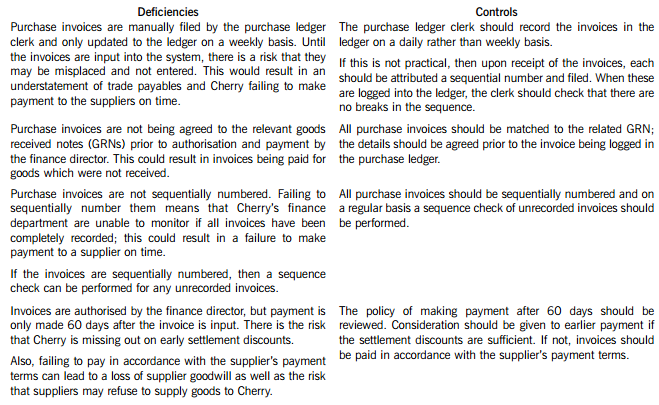

Purchase invoices are sent directly to the purchase ledger clerk, who stores them in a manual file until the end of each week. He then inputs them into the purchase ledger using batch controls and gives each invoice a unique number based on the supplier code. The invoices are reviewed and authorised for payment by the finance director, but the actual payment is only made 60 days after the invoice is input into the system.

Required:

In respect of the purchasing system of Cherry Blossom Co:

(i) Identify and explain FIVE deficiencies; and

(ii) Recommend a control to address each of these deficiencies.

Note: The total marks will be split equally between each part.

Cherry Blossom Co’s (Cherry) purchasing system deficiencies and controls

(ii) How existing standards could be modified to meet the needs of SMEs. (6 marks

(ii) The development of IFRSs for SMEs as a modification of existing IFRSs

Most SMEs have a narrower range of users than listed entities. The main groups of users are likely to be the owners,

suppliers and lenders. In deciding upon the modifications to make to IFRS, the needs of the users will need to be taken

into account as well as the costs and other burdens imposed upon SMEs by the IFRS. There will have to be a relaxation

of some of the measurement and recognition criteria in IFRS in order to achieve the reduction in the costs and the

burdens. Some disclosure requirements, such as segmental reports and earnings per share, are intended to meet the

needs of listed entities, or to assist users in making forecasts of the future. Users of financial statements of SMEs often

do not make such kinds of forecasts. Thus these disclosures may not be relevant to SMEs, and a review of all of the

disclosure requirements in IFRS will be required to assess their appropriateness for SMEs.

The difficulty is determining which information is relevant to SMEs without making the information disclosed

meaningless or too narrow/restricted. It may mean that measurement requirements of a complex nature may have to be

omitted.

There are, however, rational grounds for justifying different treatments because of the different nature of the entities and

the existence of established practices at the time of the issue of an IFRS.

(c) mandatory continuing professional development (CPD) requirements. (5 marks)

(c) Continuing Professional Development (CPD)

CPD is defined5 as ‘the continuous maintenance, development and enhancement of the professional and personal knowledge

and skills which members of ACCA require throughout their working lives’.

All professional accountants need to maintain their competence and develop new skills to be effective in their current and

future employment. CPD helps keep accountants in practice employable and maintains their reputation with employers,

clients and the public. It also helps maintain the accounting profession’s reputation for producing and supporting high calibre

individuals. Therefore, CPD is something which professional accountants should take personal responsibility for, and be doing

as part of their everyday work.

Mandatory CPD for active members of IFAC member bodies (such as ACCA) was introduced with effect from 1 January 2005

onwards. ACCA has introduced CPD as a requirement for all active members, subject to the phasing-in dates (and waivers).

Tutorial note: IFAC issued International Education Standard (IES) 7, which requires the introduction of CPD for all active

members of IFAC member bodies.

ACCA practising certificate and insolvency licence holders are still required to participate in technical CPD training. All other

members will also be asked to state on their annual CPD return that they maintain competence in professional ethics.

The scheme is being introduced in phases:

■ phase 1 (2005) – members admitted since 1 January 2001, and all practising certificate and insolvency licence

holders;

■ phase 2 (2006) – members admitted between 1 January 1995 and 31 December 2000;

■ phase 3 (2007) – all remaining members.

Tutorial note: However, ACCA encouraged all members to adopt the scheme from 1 January 2005.

Affiliates join the CPD scheme on 1 January following their date of admittance to membership.

There are two routes to participation in ACCA’s CPD scheme:

(1) the unit scheme route (40 units approximate to 40 hours required each year); and

(2) the approved CPD employer route (i.e. where employers are recognised as effectively providing ACCA members with

CPD).

Tutorial note: Alternatively, if an ACCA member is also a member of another IFAC accounting body and that CPD scheme

is compliant with IFAC’s CPD IES 7, they may choose to follow that body’ s route.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2021-01-21

- 2021-01-06

- 2019-01-05

- 2020-08-12

- 2020-10-18

- 2019-03-20

- 2020-09-05

- 2021-01-06

- 2020-08-12

- 2020-01-10

- 2019-03-20

- 2020-10-18

- 2021-01-07

- 2020-08-12

- 2020-10-19

- 2021-01-06

- 2020-04-11

- 2020-01-10

- 2020-09-05

- 2019-03-20

- 2020-09-05

- 2021-04-07

- 2020-01-10

- 2020-01-10

- 2019-01-05

- 2020-03-20

- 2020-10-18

- 2021-04-08

- 2020-08-12

- 2021-04-08