ACCA考试 2022_04_14 每日一练

(c) Explain how the introduction of an ERPS could impact on the role of management accountants. (5 marks)

(ii) Explain how the inclusion of rental income in Coral’s UK income tax computation could affect the

income tax due on her dividend income. (2 marks)

You are not required to prepare calculations for part (b) of this question.

Note: you should assume that the tax rates and allowances for the tax year 2006/07 and for the financial year to

31 March 2007 will continue to apply for the foreseeable future.

(ii) Briefly discuss FOUR non-financial factors which might influence the above decision. (4 marks)

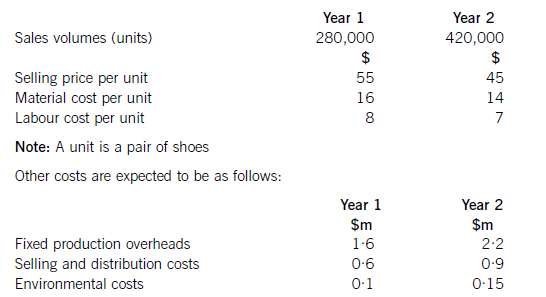

Shoe Co, a shoe manufacturer, has developed a new product called the ‘Smart Shoe’ for children, which has a built-in tracking device. The shoes are expected to have a life cycle of two years, at which point Shoe Co hopes to introduce a new type of Smart Shoe with even more advanced technology. Shoe Co plans to use life cycle costing to work out the total production cost of the Smart Shoe and the total estimated profit for the two-year period.

Shoe Co has spent $5·6m developing the Smart Shoe. The time spent on this development meant that the company missed out on the opportunity of earning an estimated $800,000 contribution from the sale of another product.

The company has applied for and been granted a ten-year patent for the technology, although it must be renewed each year at a cost of $200,000. The costs of the patent application were $500,000, which included $20,000 for the salary costs of Shoe Co’s lawyer, who is a permanent employee of the company and was responsible for preparing the application.

The following information is also available for the next two years:

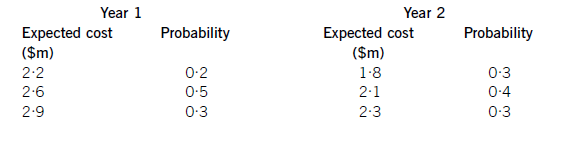

Shoe Co is still negotiating with marketing companies with regard to its advertising campaign, so is uncertain as to what the total marketing costs will be each year. However, the following information is available as regards the probabilities of the range of costs which are likely to be incurred:

Required:

Applying the principles of life cycle costing, calculate the total expected profit for Shoe Co for the two-year period.

(10 marks)

4 (a) A company may choose to finance its activities mainly by equity capital, with low borrowings (low gearing) or by

relying on high borrowings with relatively low equity capital (high gearing).

Required:

Explain why a highly geared company is generally more risky from an investor’s point of view than a company

with low gearing. (3 marks)

This scenario summarises the development of a company called Rock Bottom through three phases, from its founding in 1965 to 2008 when it ceased trading.

Phase 1 (1965–1988)

In 1965 customers usually purchased branded electrical goods, largely produced by well-established domestic companies, from general stores that stocked a wide range of household products. However, in that year, a recent university graduate, Rick Hein, established his first shop specialising solely in the sale of electrical goods. In contrast to the general stores, Rick Hein’s shop predominantly sold imported Japanese products which were smaller, more reliable and more sophisticated than the products of domestic competitors. Rick Hein quickly established a chain of shops, staffed by young people who understood the capabilities of the products they were selling. He backed this up with national advertising in the press, an innovation at the time for such a specialist shop. He branded his shops as ‘Rock Bottom’, a name which specifically referred to his cheap prices, but also alluded to the growing importance of

rock music and its influence on product sales. In 1969, 80% of sales were of music centres, turntables, amplifiers and speakers, bought by the newly affluent young. Rock Bottom began increasingly to specialise in selling audio equipment.

Hein also developed a high public profile. He dressed unconventionally and performed a number of outrageous stunts that publicised his company. He also encouraged the managers of his stores to be equally outrageous. He rewarded their individuality with high salaries, generous bonus schemes and autonomy. Many of the shops were extremely successful, making their managers (and some of their staff) relatively wealthy people.

However, by 1980 the profitability of the Rock Bottom shops began to decline significantly. Direct competitors using a similar approach had emerged, including specialist sections in the large general stores that had initially failed to react to the challenge of Rock Bottom. The buying public now expected its electrical products to be cheap and reliable.

Hein himself became less flamboyant and toned down his appearance and actions to satisfy the banks who were becoming an increasingly important source of the finance required to expand and support his chain of shops.

Phase 2 (1989–2002)

In 1988 Hein considered changing the Rock Bottom shops into a franchise, inviting managers to buy their own shops (which at this time were still profitable) and pursuing expansion though opening new shops with franchisees from outside the company. However, instead, he floated the company on the country’s stock exchange. He used some of the capital raised to expand the business. However, he also sold shares to help him throw the ‘party of a lifetime’ and to purchase expensive goods and gifts for his family. Hein became Chairman and Chief Executive Officer (CEO) of the newly quoted company, but over the next thirteen years his relationship with his board and shareholders became increasingly difficult. Gradually new financial controls and reporting systems were put in place. Most of the established managers left as controls became more centralised and formal. The company’s performance was solid but unspectacular. Hein complained that ‘business was not fun any more’. The company was legally required to publish directors’ salaries in its annual report and the generous salary package enjoyed by the Chairman and CEO increasingly became an issue and it dominated the 2002 Annual General Meeting (AGM). Hein was embarrassed by its publication and the discussion it led to in the national media. He felt that it was an infringement of his privacy and

civil liberties.

Phase 3 (2003–2008)

In 2003 Hein found the substantial private equity investment necessary to take Rock Bottom private again. He also used all of his personal fortune to help re-acquire the company from the shareholders. He celebrated ‘freeing Rock Bottom from its shackles’ by throwing a large celebration party. Celebrities were flown in from all over the world to attend. However, most of the new generation of store managers found Hein’s style. to be too loose and unfocused. He became rude and angry about their lack of entrepreneurial spirit. Furthermore, changes in products and how they were purchased meant that fewer people bought conventional audio products from specialist shops. The reliability of these products now meant that they were replaced relatively infrequently. Hein, belatedly, started to consider selling via an Internet site. Turnover and profitability plummeted. In 2007 Hein again considered franchising the company,but he realised that this was unlikely to be successful. In early 2008 the company ceased trading and Hein himself,now increasingly vilified and attacked by the press, filed for personal bankruptcy.

Required:

(a) Analyse the reasons for Rock Bottom’s success or failure in each of the three phases identified in the

scenario. Evaluate how Rick Hein’s leadership style. contributed to the success or failure of each phase.

(18 marks)

(b) Rick Hein considered franchising the Rock Bottom brand at two points in its history – 1988 and 2007.

Explain the key factors that would have made franchising Rock Bottom feasible in 1988, but would have

made it ‘unlikely to be successful’ in 2007. (7 marks)

18 Which of the following statements about accounting ratios and their interpretation are correct?

1 A low-geared company is more able to survive a downturn in profit than a highly-geared company.

2 If a company has a high price earnings ratio, this will often indicate that the market expects its profits to rise.

3 All companies should try to achieve a current ratio (current assets/current liabilities) of 2:1.

A 2 and 3 only

B 1 and 3 only

C 1 and 2 only

D All three statements are correct

(c) Acting as an external consultant to Semer, discuss the validity of the proposed strategy to increase gearing, and explain whether or not the estimates produced in (b) above are likely to be accurate. (10 marks)