ACCA证书的含金量怎么样?考ACCA有用吗?

发布时间:2021-09-23

ACCA会员资格在国际上得到广泛认可,尤其得到欧盟立法以及许多国家公司法的承认。可以说拥有ACCA会员资格,等于拥有了在世界各地就业的"通行证"。ACCA证书的含金量怎么样?未来发展前景如何?今天和51题库考试学习网一起来看看吧!

ACCA的课程是根据现时商务社会对财会人员的实际要求进行开发设计的,特别注重培养学员的分析能力和在复杂条件下的决策与判断能力。并系统、高质量的培训给予学员真才实学,让学员学成后能适应各种环境,逐步成为具有全面管理素质的高级财务管理专家。

为了更好地为企业提供支持,ACCA向全球雇主推出一项免费合作项目——ACCA认可雇主计划,免费加入ACCA认可雇主计划,即可享受优质财会人才招聘和员工培训发展等一系列专享免费服务。目前在全球范围内有超过8500家企业为认可雇主,优先聘用提拔ACCA学员及会员,中国地区有超过600家国际国内大型企业为ACCA认可雇主企业。

ACCA会员可在工商企业财务部门、审计/会计师事务所、金融机构和财政、税务部门从事财务和财务管理工作。很多会员在世界各地大公司担任高级职位(财务经理、财务总监CFO,甚至总裁CEO)。ACCA学员主要就业方向为:

国际、国内金融机构、大型银行、投资银行。例如:中国工商银行、中国银行、中国国际金融公司、交通银行、汇丰银行、花旗银行、渣打银行、法国兴业银行、荷兰银行等。

跨国企业,国内大型企业。如:宝洁、联合利华、壳牌石油、微软、强生、GE、中石化、阿里巴巴集团、中国移动等大型企业。

国际大型金融咨询机构或专业会计师事务所。如埃森哲咨询等国际金融咨询机构、普华永道、毕马威、德勤、安永"四大"会计师事务所等国际会计师事务所。

考ACCA有用吗?

首先来看,ACCA的适用性。ACCA是目前全球最大的会计师组织,有10万会员和20多万学员,分布在全球160个国家。ACCA除了英国以外,主要是在英联邦国家得到承认。在中国,ACCA从九十年代初进中国以来,公众认可度也是越来越高,尤其在欧美背景的外企、外资会计事务所、在海外上市的企业受到了广泛的认可。

其次看看,ACCA的课程设置。具体内容请参考acca官方网站。十四门课程,涉及会计、审计、税法、财务管理、管理系统、企业战略、金融投资等多方面的内容。比起中国的cpa要全面很多。覆盖了一个财务总监通常应掌握的知识体系。学习起来,也不是那么枯燥,比较注重知识与实践相结合。有些考生,就算不是准备得很充分,在考试答题时还是可以用自己的经验和积累弥补准备的不足,就是由于这个道理。所以总的来讲,就算你不抱什么特别的学习目的。至少,ACCA是一套非常不错的且完善的财务培训课程。

考ACCA有用吗?当然有用,但机会总是属于有准备的人。如果你的经验够好,又有好的证书,总有机会是你的。今天分享就到这里了,更多相关资讯,敬请关注51题库考试学习网!

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(b) Prepare the balance sheet of York at 31 October 2006, using International Financial Reporting Standards,

discussing the nature of the accounting treatments selected, the adjustments made and the values placed

on the items in the balance sheet. (20 marks)

Gow’s net assets

IAS36 ‘Impairment of Assets’, sets out the events that might indicate that an asset is impaired. These circumstances include

external events such as the decline in the market value of an asset and internal events such as a reduction in the cash flows

to be generated from an asset or cash generating unit. The loss of the only customer of a cash generating unit (power station)

would be an indication of the possible impairment of the cash generating unit. Therefore, the power station will have to be

impairment tested.

The recoverable amount will have to be determined and compared to the value given to the asset on the setting up of the

joint venture. The recoverable amount is the higher of the cash generating unit’s fair value less costs to sell, and its value-inuse.

The fair value less costs to sell will be $15 million which is the offer for the purchase of the power station ($16 million)

less the costs to sell ($1 million). The value-in-use is the discounted value of the future cash flows expected to arise from the

cash generating unit. The future dismantling costs should be provided for as it has been agreed with the government that it

will be dismantled. The cost should be included in the future cash flows for the purpose of calculating value-in-use and

provided for in the financial statements and the cost added to the property, plant and equipment ($4 million ($5m/1·064)).

The value-in-use based on a discount rate of 6 per cent is $21 million (working). Therefore, the recoverable amount is

$21 million which is higher than the carrying value of the cash generating unit ($20 million) and, therefore, the value of the

cash generating unit is not impaired when compared to the present carrying value of $20 million (value before impairment

test).

Additionally IAS39, ‘Financial Instruments: recognition and measurement’, says that an entity must assess at each balance

sheet date whether a financial asset is impaired. In this case the receivable of $7 million is likely to be impaired as Race is

going into administration. The present value of the estimated future cash flows will be calculated. Normally cash receipts from

trade receivables will not be discounted but because the amounts are not likely to be received for a year then the anticipated

cash payment is 80% of ($5 million × 1/1·06), i.e. $3·8 million. Thus a provision for the impairment of the trade receivables

of $3·2 million should be made. The intangible asset of $3 million would be valueless as the contract has been terminated.

Glass’s Net Assets

The leased property continues to be accounted for as property, plant and equipment and the carrying amount will not be

adjusted. However, the remaining useful life of the property will be revised to reflect the shorter term. Thus the property will

be depreciated at $2 million per annum over the next two years. The change to the depreciation period is applied prospectively

not retrospectively. The lease liability must be assessed under IAS39 in order to determine whether it constitutes a

de-recognition of a financial liability. As the change is a modification of the lease and not an extinguishment, the lease liability

would not be derecognised. The lease liability will be adjusted for the one off payment of $1 million and re-measured to the

present value of the revised future cash flows. That is $0·6 million/1·07 + $0·6 million/(1·07 × 1·07) i.e. $1·1 million. The

adjustment to the lease liability would normally be recognised in profit or loss but in this case it will affect the net capital

contributed by Glass.

The termination cost of the contract cannot be treated as an intangible asset. It is similar to redundancy costs paid to terminate

a contract of employment. It represents compensation for the loss of future income for the agency. Therefore it must be

removed from the balance sheet of York. The recognition criteria for an intangible asset require that there should be probable

future economic benefits flowing to York and the cost can be measured reliably. The latter criterion is met but the first criterion

is not. The cost of gaining future customers is not linked to this compensation.

IAS18 ‘Revenue’ contains a concept of a ‘multiple element’ arrangement. This is a contract which contains two or more

elements which are in substance separate and are separately identifiable. In other words, the two elements can operate

independently from each other. In this case, the contract with the overseas company has two distinct elements. There is a

contract not to supply gas to any other customer in the country and there is a contract to sell gas at fair value to the overseas

company. The contract has not been fulfilled as yet and therefore the payment of $1·5 million should not be taken to profit

or loss in its entirety at the first opportunity. The non supply of gas to customers in that country occurs over the four year

period of the contract and therefore the payment should be recognised over that period. Therefore the amount should be

shown as deferred income and not as a deduction from intangible assets. The revenue on the sale of gas will be recognised

as normal according to IAS18.

There may be an issue over the value of the net assets being contributed. The net assets contributed by Glass amount to

$21·9 million whereas those contributed by Gow only total $13·8 million after taking into account any adjustments required

by IFRS. The joint venturers have equal shareholding in York but no formal written agreements, thus problems may arise ifGlass feels that the contributions to the joint venture are unequal.

(iii) State how your answer in (ii) would differ if the sale were to be delayed until August 2006. (3 marks)

(b) Assess the likely strategic impact of the new customer delivery system on Supaserve’s activities and its ability

to differentiate itself from its competitors. (10 marks)

(b) Supaserve, through its electronic point of sale system (EPOS), is already likely to have useful information on the overall

patterns of buying behaviour in terms of products bought frequently, peak periods, etc. It is less likely to have detailed

information on individual customer purchase patterns, though it may be monitoring where its customers are living, travel

patterns, etc. The introduction of the new online system has the potential to have a major strategic impact on the company

and its relationship with its customers. Impact can be measured by assessing the significance of the change on the company’s

operations and the likelihood of its occurrence. In Michael Porter’s words, ‘the basic tool for understanding the influence of

information technology on companies is the value chain . . . and how it affects both a company’s cost and the value delivered

to buyers’.

Clearly the investment in Internet based technology will affect both the cost and revenue sides of the business. In terms of

operations the company will need to decide the way in which to integrate the new method of customer buying with its

traditional methods. Does it create a separate ‘dedicated’ warehouse operation solely involved with the online business or does

it integrate it within its existing operations? The customer will have immediate access to information on whether goods are in

stock or not, and this may have a significant impact on the procurement systems Supaserve has with its suppliers and the

inbound logistics which get the products to where they are needed for dispatch to the customers.

Online shopping will have a major impact on outbound logistics in that a totally new distribution process will have to be

created. The extent to which this new service is provided in-house by setting up a new activity within Supaserve, or

alternatively is outsourced to specialist distributors is a key decision affecting costs and efficiency. Supaserve’s delivery

performance will be both measurable and potentially available to competitors and a real source of competitive advantage or

disadvantage.

The new online system will have an immediate impact on marketing and sales. Can customers pay over the Internet?

Opportunities for direct marketing to individual customers are opened up and customisation becomes a real possibility.

Customers can link into after-sales services and provide insights into customer satisfaction. On the support side of the value

chain the impact on human resources may be profound and technology lies at the heart of the change. Above all there is a

key need to link the new strategy to the operational systems needed to deliver it.

Clearly, the introduction of the online shopping system offers an opportunity for Supaserve to differentiate itself from its

aggressive competitors. The online service, as suggested above, is likely to appeal to a limited but growing segment of its

customers. In strategic terms it is a focus differentiation strategy enabling Supaserve to provide an improved level of service

to its customers. For this customers are willing to pay a small premium. Perhaps the more significant impact on its profit

margins will be derived from improved levels of customer retention and the attraction of customers who formerly shopped

with its competitors. The ability to sustain its competitive advantage will be measured by the impact on its competitors and

their ability to introduce a similar service.

There are a number of useful models for assessing the impact of an IT related change. These could include the five forces

model and the frameworks developed by Michael Earl assessing the strategic impact of IT. Michael Earl argues persuasively

for the correct alignment between business strategy and IT strategy. Indeed he sees a need for a ‘binary approach’ with the

alignment of IT investment activities in existing ways of doing business as having to be accommodated with the IT investments

associated with more radical change to the ways business is conducted.

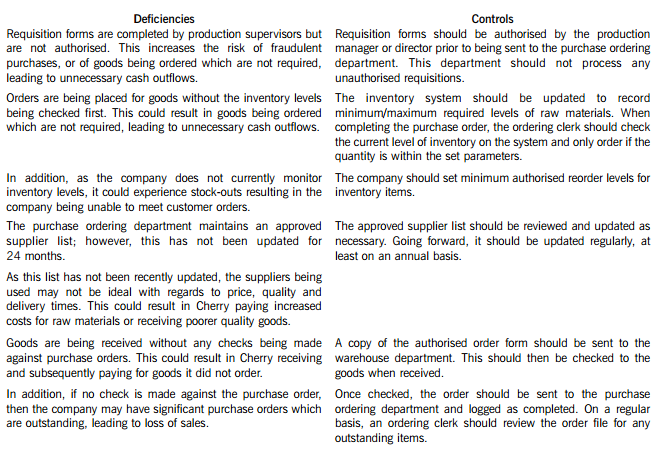

Cherry Blossom Co (Cherry) manufactures custom made furniture and its year end is 30 April. The company purchases its raw materials from a wide range of suppliers. Below is a description of Cherry’s purchasing system.

When production supervisors require raw materials, they complete a requisition form. and this is submitted to the purchase ordering department. Requisition forms do not require authorisation and no reference is made to the current inventory levels of the materials being requested. Staff in the purchase ordering department use the requisitions to raise sequentially numbered purchase orders based on the approved suppliers list, which was last updated 24 months ago. The purchasing director authorises the orders prior to these being sent to the suppliers.

When the goods are received, the warehouse department verifies the quantity to the suppliers despatch note and checks that the quality of the goods received are satisfactory. They complete a sequentially numbered goods received note (GRN) and send a copy of the GRN to the finance department.

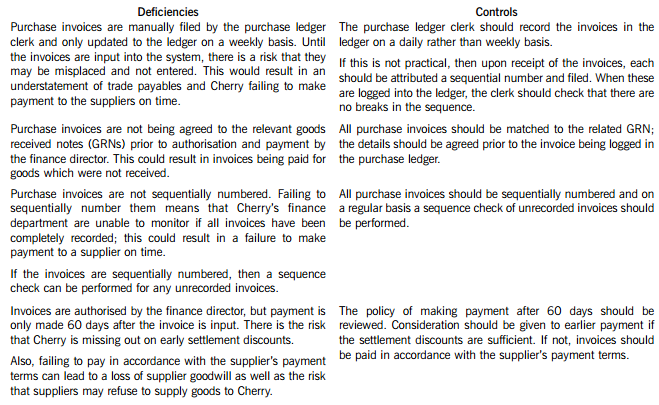

Purchase invoices are sent directly to the purchase ledger clerk, who stores them in a manual file until the end of each week. He then inputs them into the purchase ledger using batch controls and gives each invoice a unique number based on the supplier code. The invoices are reviewed and authorised for payment by the finance director, but the actual payment is only made 60 days after the invoice is input into the system.

Required:

In respect of the purchasing system of Cherry Blossom Co:

(i) Identify and explain FIVE deficiencies; and

(ii) Recommend a control to address each of these deficiencies.

Note: The total marks will be split equally between each part.

Cherry Blossom Co’s (Cherry) purchasing system deficiencies and controls

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-01-09

- 2020-01-10

- 2020-01-09

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-01-11

- 2020-01-10

- 2020-04-23

- 2020-01-10

- 2020-05-16

- 2020-08-16

- 2019-01-05

- 2020-03-07

- 2020-04-09

- 2020-01-10

- 2020-01-31

- 2020-01-10

- 2020-01-10

- 2020-04-15

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2021-06-25

- 2020-01-09

- 2019-05-01

- 2020-03-08

- 2020-01-10

- 2020-01-09

- 2020-01-10