2020年第一次报名ACCA考试考几科呀?

发布时间:2020-02-28

ACCA考试科目较多,如何合理搭配科目就成为了许多小伙伴们关心的问题,尤其是对于第一次参加考试的新考生来说。比如,有网友就在询问2020年第一次报名ACCA考试考几科。鉴于此,51题库考试学习网在下面为大家带来2020年ACCA考试科目搭配的相关信息,以供参考。

ACCA考试必须按照四大课程的顺序进行,因此小伙伴们主要关注的是课程内的科目搭配顺序。事实上。ACCA官方建议学员只需按照科目顺序从F1考到P7是非常合理的。同时,因为一年只能考8门,ACCA每年有四个考试季,即四次考试。所以平均下来每次报2科目就非常简单合理了。不过,由于2020年第一考试季的ACCA考试已经取消(中国地区),因此准备好的小伙伴们也可以在剩下的考试季适当增加一科。

以上就是关于ACCA考试科目搭配的相关情况。51题库考试学习网提醒:以上提供的科目搭配方案仅供参考,首次报考的小伙伴们如果觉得准备不够充足,最好适当减少报考科目。最后,51题库考试学习网预祝准备参加2020年ACCA考试的小伙伴都能顺利通过。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(c) Using information from the case, assess THREE risks to the Giant Dam Project. (9 marks)

(c) Assessment of three risks

Disruption and resistance by Stop-the-dam. Stop-the-dam seems very determined to delay and disrupt progress as much as

possible. The impact of its activity can be seen on two levels. It is likely that the tunnelling and other ‘human’ disruption will

cause a short-term delay but the more significant impact is that of exposing the lenders. In terms of probability, the case says

that it ‘would definitely be attempting to resist the Giant Dam Project when it started’ but the probability of exposing the

lenders is a much lower probability event if the syndicate membership is not disclosed.

Impact/hazard: low

Probability/likelihood: high

The risk to progress offered by First Nation can probably be considered to be low impact/hazard but high probability. The case

says that it ‘would be unlikely to disrupt the building of the dam’, meaning low impact/hazard, but that ‘it was highly likely

that they would protest’, meaning a high level of probability that the risk event would occur.

Impact: low

Probability: high

There are financing risks as banks seems to be hesitant when it comes to lending to R&M for the project. Such a risk event,

if realised, would have a high potential for disruption to progress as it may leave R&M with working capital financing

difficulties. The impact would be high because the bank may refuse to grant or extend loans if exposed (subject to existing

contractual terms). It is difficult to estimate the probability. Perhaps there will be a range of attitudes by the lending banks

with some more reticent than others (perhaps making it a ‘medium’ probability event).

Impact: medium to high (depending on the reaction of the bank)

Probability: low to medium (depending on how easy it would be to discover the lender)

(b) Briefly explain the two types of informal communication known as the grapevine and rumour. (6 marks)

(b) The grapevine and rumour are the two main types of informal communication.

The grapevine is probably the best known type of informal communication. All organisations have a grapevine and it will thrive if there is lack of information and consequently employees will make assumptions about events. In addition, insecurity,gossip about issues and fellow employees, personal animosity between employees or managers or new information that has not yet reached the formal communication system, will all drive the grapevine.

Rumours are the other main informal means of communication and are often active if there is a lack of formal communication.A rumour is inevitably a communication not based on verified facts and may therefore be true or false. Rumours travel quickly(often quicker than both the formal system and the grapevine) and can influence those who hear them and cause confusion,especially if bad news is the basis of the rumour. Managers must ensure that the formal communication system is such that rumours can be stopped, especially since they can have a serious negative effect on employees.

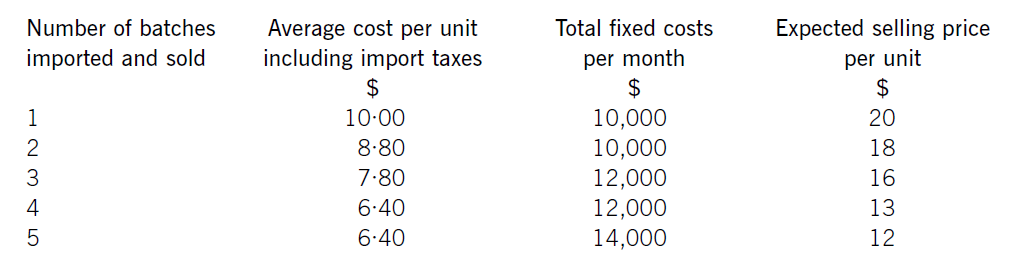

Jewel Co is setting up an online business importing and selling jewellery headphones. The cost of each set of headphones varies depending on the number purchased, although they can only be purchased in batches of 1,000 units. It also has to pay import taxes which vary according to the quantity purchased.

Jewel Co has already carried out some market research and identified that sales quantities are expected to vary depending on the price charged. Consequently, the following data has been established for the first month:

Required:

(a) Calculate how many batches Jewel Co should import and sell. (6 marks)

(b) Explain why Jewel Co could not use the algebraic method to establish the optimum price for its product.

(4 marks)

(b)Thealgebraicmodelrequiresseveralassumptionstobetrue.First,theremustbeaconsistentrelationshipbetweenprice(P)anddemand(Q),sothatademandequationcanbeestablished,usuallyintheform.P=a–bQ.Here,althoughthereisaclearrelationshipbetweenthetwo,itisnotaperfectlylinearrelationshipandsomorecomplicatedtechniquesarerequiredtocalculatethedemandequation.ItalsocannotbeassumedthatalinearrelationshipwillholdforallvaluesofPandQotherthanthefivegiven.Similarly,theremustbeaclearrelationshipbetweendemandandmarginalcost,usuallysatisfiedbyconstantvariablecostperunitandconstantfixedcosts.Thechangingvariablecostsperunitagaincomplicatetheissue,butitisthechangesinfixedcostswhichmakethealgebraicmethodlessusefulinJewel’scase.Thealgebraicmodelisonlysuitableforcompaniesoperatinginamonopolyanditisnotclearherewhetherthisisthecase,butitseemsunlikely,soany‘optimum’pricemightbecomeirrelevantifJewel’scompetitorschargesignificantlylowerprices.Othermoregeneralfactorsnotconsideredbythealgebraicmodelarepoliticalfactorswhichmightaffectimports,socialfactorswhichmayaffectcustomertastesandeconomicfactorswhichmayaffectexchangeratesorcustomerspendingpower.Thereliabilityoftheestimatesthemselves–forsalesprices,variablecostsandfixedcosts–couldalsobecalledintoquestion.

(b) continuous auditing; (5 marks)

(b) Continuous auditing

Continuous auditing is a methodology that enables independent auditors to give written assurance on a subject matter (e.g.

inventory levels, receivables balances, financial statements) using a series of auditor’s reports issued simultaneously with (or

a short period of time after) the occurrence of events underlying the subject matter. Thus it increases the frequency of

reporting (e.g. may be issued daily, weekly).

Technological development is making increasingly sophisticated information systems available to more entities at a decreasing

cost. This has promoted a more widespread dependence on technology to produce more timely information. This has

increased the demand for timely assurance on the information provided. Auditors have had to respond with highly automated

procedures and audit tools that are integrated with the entity’s systems and controls.

Tutorial note: XBRL (eXtensible Business Reporting Language) increases the viability of continuous auditing. It provides a

widely agreed-upon set of descriptors for elements in a business report that can be read and interpreted by computer

systems. It allows an auditor to review data at any stage and determine the origin of the information and the controls that

have been incorporated.

Results of automated audit procedures must be communicated promptly, particularly if anomalies or errors identified require

that follow-up procedures be performed by audit personnel. Secure electronic communication links are therefore essential.

As entities’ reporting has moved from annual and interim reports to the monthly/daily/weekly reporting of key performance

indicators (‘KPIs’)/critical success factors (‘CSFs’), the professional accountant’s assignment has expanded from the audit of

financial statements. For example, to review reports (e.g. on interim financial statements), special purpose reports (e.g. on

the effectiveness of [outsourced] control procedures) to continuous auditing reports.

For continuous audits, auditors’ reports need to be produced automatically and safeguarded against unauthorised changes.

Reports may be ‘evergreen’ (i.e. always available to users and dated at the time of access to the information) or ‘on demand’

(i.e. available when specifically requested and dated at the time of request).

Auditors must be technically proficient to handle any engagement undertaken. For continuous audit assurance engagements

that will require a high level of expertise in various aspects of information technology as well as a sound grasp of the subject

matter being audited.

Continuous audit work requires the frequent or continuous use of audit tools integrated with the client’s systems. For example

embedded audit modules (EAMs) are subroutines that perform. control or audit procedures concurrently with the client’s

normal application processing.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-04-30

- 2020-03-26

- 2020-04-15

- 2020-01-10

- 2020-01-09

- 2020-03-14

- 2020-01-10

- 2020-01-10

- 2020-01-08

- 2020-02-29

- 2020-03-05

- 2020-03-11

- 2020-01-09

- 2020-01-09

- 2020-01-09

- 2020-01-04

- 2020-01-09

- 2020-10-09

- 2020-03-18

- 2019-07-21

- 2020-08-01

- 2021-05-07

- 2020-04-19

- 2020-03-05

- 2020-01-08

- 2020-03-18

- 2020-01-09

- 2020-01-30

- 2020-04-10

- 2020-03-22