2021年青海ACCA考试准考证打印时间:考前两周

发布时间:2021-01-03

参加任何考试最重要是的携带准考证,那2021年ACCA青海地区准考证打印相关信息想必很多考生还不知道!下面跟51题库考试学习网一起先来看看吧。

ACCA考试准考证打印时间:在考前两周,可以登陆MYACCA里打印准考证(准考证是学员考试必带的证明,请重视,打印准考证数量须和考试科数相同)。因邮寄的准考证收到时间较晚,建议提前打印好准考证,仔细核对报考科目和考试地点有无错误。

ACCA考试准考证打印步骤如下:

(1)ACCA考试学员需登录www.accaglobal.com。

(2)点击MYACCA后输入学员号和密码进入。

(3)点击左侧栏里EXAM ENTRY&RESULTS进入。

(4)点击EXAM ATTENDANCE DOCKET生成页面打印即可。

ACCA准考证打印注意事项与常见问题:

1、准考证打印需要关注问题

首先提醒考生们在打印准考证时要认真核对个人信息,是否和报名时所用的身份证信息一致,如果出现问题一定要第一时间联系协会。

大家在打印时除了要留意准考证上的姓名、考试地点和照片等信息外,也要看一下各科目的考试时间。

2、打印网址进不去

准考证打印的前几天属于高峰期,大家要尽量的错开高峰期打印,但是也不要拖到最后,避免发生网络错误打印不出准考证的情况出现。

3、准考证不幸丢失怎么办?

建议大家在打印时留好备份,避免丢失造成不必要的麻烦。

4、如果无法下载该怎么办呢?

很可能是由于学员所报考考点的地址信息细节暂时未能确认而导致准考证未开放下载。请耐心等待ACCA确认地址信息细节。如果有考生是属于此情况,ACCA将发送电子邮件告知何时可以下载准考证,请考生注意查收相关邮件!

5、如果考场地点尚未确定,页面会显示?

将看到以下提示信息: “Please note your exam docket is currently unavailable, please try again later.” (请留意,目前您的准考证还未能下载,请稍后再试。)

6、准考证上信息和报考系统不一样

准考证作为正式的考试凭证,为学员确认每个考季的最终考试信息,因此,应以准考证上的考试信息为准,包括考试日期、时间与考点地址。

以上内容就是51题库考试学习网为大家分享的ACCA考试准考证打印的相关讯息,考生在备考期间一定要合理分配学习时间,最后51题库考试学习网预祝各位考生都能顺利通过考试!

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

3 You are the manager responsible for the audit of Volcan, a long-established limited liability company. Volcan operates

a national supermarket chain of 23 stores, five of which are in the capital city, Urvina. All the stores are managed in

the same way with purchases being made through Volcan’s central buying department and product pricing, marketing,

advertising and human resources policies being decided centrally. The draft financial statements for the year ended

31 March 2005 show revenue of $303 million (2004 – $282 million), profit before taxation of $9·5 million (2004

– $7·3 million) and total assets of $178 million (2004 – $173 million).

The following issues arising during the final audit have been noted on a schedule of points for your attention:

(a) On 1 May 2005, Volcan announced its intention to downsize one of the stores in Urvina from a supermarket to

a ‘City Metro’ in response to a significant decline in the demand for supermarket-style. shopping in the capital.

The store will be closed throughout June, re-opening on 1 July 2005. Goodwill of $5·5 million was recognised

three years ago when this store, together with two others, was bought from a national competitor. It is Volcan’s

policy to write off goodwill over five years. (7 marks)

Required:

For each of the above issues:

(i) comment on the matters that you should consider; and

(ii) state the audit evidence that you should expect to find,

in undertaking your review of the audit working papers and financial statements of Volcan for the year ended

31 March 2005.

NOTE: The mark allocation is shown against each of the three issues.

3 VOLCAN

(a) Store impairment

(i) Matters

■ Materiality

? The cost of goodwill represents 3·1% of total assets and is therefore material.

? However, after three years the carrying amount of goodwill ($2·2m) represents only 1·2% of total assets –

and is therefore immaterial in the context of the balance sheet.

? The annual amortisation charge ($1·1m) represents 11·6% profit before tax (PBT) and is therefore also

material (to the income statement).

? The impact of writing off the whole of the carrying amount would be material to PBT (23%).

Tutorial note: The temporary closure of the supermarket does not constitute a discontinued operation under IFRS 5

‘Non-Current Assets Held for Sale and Discontinued Operations’.

■ Under IFRS 3 ‘Business Combinations’ Volcan should no longer be writing goodwill off over five years but

subjecting it to an annual impairment test.

■ The announcement is after the balance sheet date and is therefore a non-adjusting event (IAS 10 ‘Events After the

Balance Sheet Date’) insofar as no provision for restructuring (for example) can be made.

■ However, the event provides evidence of a possible impairment of the cash-generating unit which is this store and,

in particular, the value of goodwill assigned to it.

■ If the carrying amount of goodwill ($2·2m) can be allocated on a reasonable and consistent basis to this and the

other two stores (purchased at the same time) Volcan’s management should have applied an impairment test to

the goodwill of the downsized store (this is likely to show impairment).

■ If more than 22% of goodwill is attributable to the City Metro store – then its write-off would be material to PBT

(22% × $2·2m ÷ $9·5m = 5%).

■ If the carrying amount of goodwill cannot be so allocated; the impairment test should be applied to the

cash-generating unit that is the three stores (this may not necessarily show impairment).

■ Management should have considered whether the other four stores in Urvina (and elsewhere) are similarly

impaired.

■ Going concern is unlikely to be an issue unless all the supermarkets are located in cities facing a downward trend

in demand.

Tutorial note: Marks will be awarded for stating the rules for recognition of an impairment loss for a cash-generating

unit. However, as it is expected that the majority of candidates will not deal with this matter, the rules of IAS 36 are

not reproduced here.

(ii) Audit evidence

■ Board minutes approving the store’s ‘facelift’ and documenting the need to address the fall in demand for it as a

supermarket.

■ Recomputation of the carrying amount of goodwill (2/5 × $5·5m = $2·2m).

■ A schedule identifying all the assets that relate to the store under review and the carrying amounts thereof agreed

to the underlying accounting records (e.g. non-current asset register).

■ Recalculation of value in use and/or fair value less costs to sell of the cash-generating unit (i.e. the store that is to

become the City Metro, or the three stores bought together) as at 31 March 2005.

Tutorial note: If just one of these amounts exceeds carrying amount there will be no impairment loss. Also, as

there is a plan NOT to sell the store it is most likely that value in use should be used.

■ Agreement of cash flow projections (e.g. to approved budgets/forecast revenues and costs for a maximum of five

years, unless a longer period can be justified).

■ Written management representation relating to the assumptions used in the preparation of financial budgets.

■ Agreement that the pre-tax discount rate used reflects current market assessments of the time value of money (and

the risks specific to the store) and is reasonable. For example, by comparison with Volcan’s weighted average cost

of capital.

■ Inspection of the store (if this month it should be closed for refurbishment).

■ Revenue budgets and cash flow projections for:

– the two stores purchased at the same time;

– the other stores in Urvina; and

– the stores elsewhere.

Also actual after-date sales by store compared with budget.

(b) Describe the audit work to be performed in respect of the carrying amount of the following items in the

balance sheet of GVF as at 30 September 2005:

(i) goat herd; (4 marks)

(b) Audit work on carrying amounts

Tutorial note: This part concerns audit work to be undertaken in respect of non-current tangible assets (the production

animals in the goat herd and certain equipment) and inventories (the for-sale animals and cheese). One of the ‘tests’ for

assessing whether or not a point is worthy of a mark will be whether or not the asset to which it relates is apparent. Points

which are so vague that they could apply to ANY non-current asset for ANY entity, rather than those of GVF are unlikely to

attract many marks, if any, at this level.

(i) Goat herd

■ Physical inspection of the number and condition of animals in the herd and confirming, on a test basis, that they

are tagged (or otherwise ‘branded’ as being owned by GVF).

■ Tests of controls on management’s system of identifying and distinguishing held-for-sale animals (inventory) from

the production herd (depreciable non-current assets).

■ Comparison of GVF’s depreciation policies (including useful lives, depreciation methods and residual values) with

those used by other farming entities.

■ ‘Proof in total’, or other reasonableness check, of the depreciation charge for the herd for the year.

■ Observing test counts or total counts of animals held for sale.

■ Comparing carrying amounts of the kids, according to their weight and age, as at 30 September 2005 with their

market values. (These may approximate to actual invoiced selling prices obtained by GVF.)

Tutorial note: Market value of the production herd could also be compared with its carrying amount to assess possible

impairment. However, if value in use appears to be less than market value the herd should be sold rather than used

for production.

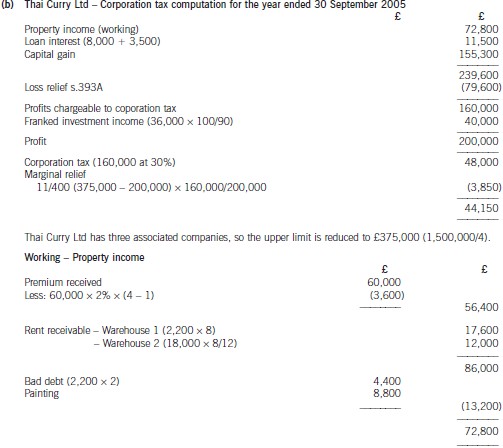

(b) Assuming that Thai Curry Ltd claims relief for its trading loss against total profits under s.393A ICTA 1988,calculate the company’s corporation tax liability for the year ended 30 September 2005. (10 marks)

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-01-10

- 2020-01-10

- 2020-01-09

- 2020-01-08

- 2021-04-17

- 2020-08-14

- 2020-08-15

- 2020-01-10

- 2021-06-27

- 2020-08-14

- 2020-08-15

- 2020-09-04

- 2020-01-08

- 2020-01-09

- 2020-12-24

- 2020-09-04

- 2020-12-24

- 2020-08-19

- 2020-01-10

- 2020-01-10

- 2020-01-08

- 2020-08-14

- 2020-01-08

- 2020-09-04

- 2021-04-17

- 2020-01-10

- 2020-01-10

- 2020-01-09

- 2020-01-10

- 2020-09-04